E-Bike 구동장치 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)

E-Bike Drive Unit Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1844328

리서치사:Global Market Insights Inc.

발행일:2025년 09월

페이지 정보:영문 230 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

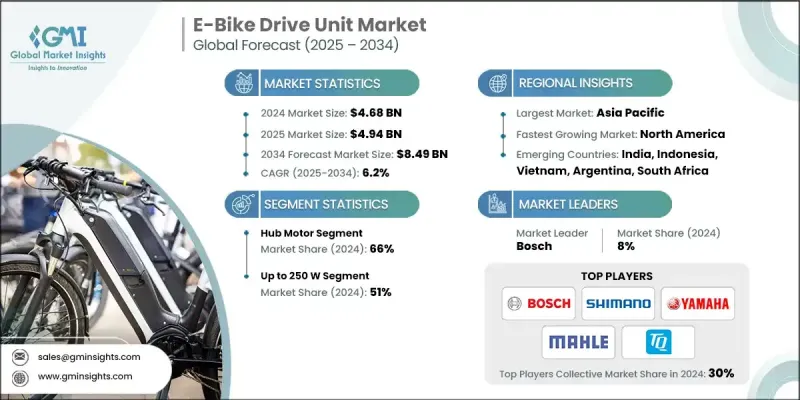

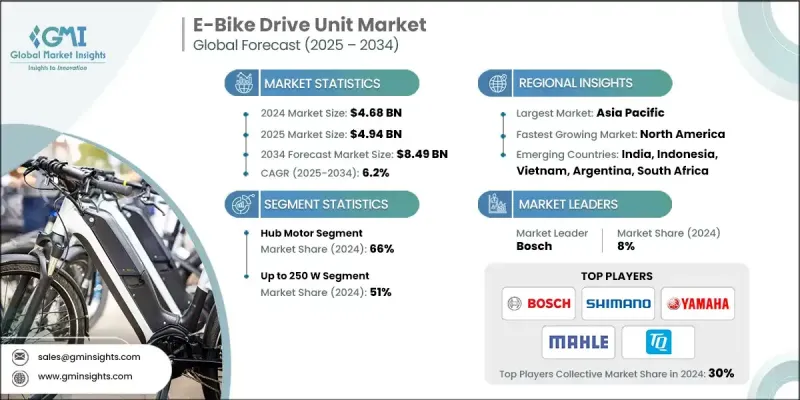

E-Bike 구동장치 세계 시장 규모는 2024년에 46억 8,000만 달러로 평가되었고, CAGR 6.2%로 성장하여 2034년에는 84억 9,000만 달러에 이를 것으로 예측됩니다.

전기 모빌리티가 주류가 되면서 효율적이고 지능적인 구동 시스템에 대한 수요는 계속 증가하고 있습니다. 이러한 구동 장치는 모터, 제어 시스템, 센서를 결합하여 e-bike의 보조 및 완전한 동력원이 되어 사용자 경험을 향상시킵니다. 수년에 걸쳐 기술은 기본적인 허브 모터에서 전자 장치와 소프트웨어를 통합한 정교한 시스템으로 발전해 왔습니다. 구동장치에는 토크 센서, 회생 브레이크, 지능형 연결 기능이 탑재되는 경우가 많으며, 다양한 지형과 도시 지역에서 사용할 수 있는 고효율 및 스마트한 기능을 갖추고 있습니다. 미드 구동장치은 균형 잡힌 무게 배분, 우수한 토크, 기존 드라이브 트레인과의 완벽한 통합으로 트레킹, 산악 자전거, 화물 자전거에서 인기를 얻고 있습니다. 모듈식 배터리 설계와 향상된 연결 기능은 이러한 시스템의 가치를 높이고 있습니다. OEM은 공급망을 지배하고 자전거 제조업체에 완벽한 솔루션을 제공하며 제품 개발 과정에서 중요한 파트너십을 형성하고 있습니다. 개조 키트 및 교체용 모터 애프터마켓도 존재하지만, 전체 매출에서 차지하는 비중은 미미하며, 매출의 대부분은 OEM 중심의 제조 채널에 뿌리를 두고 있습니다.

시장 범위

개시 연도

2024년

예측 연도

2025-2034년

시장 규모

46억 8,000만 달러

예측 금액

84억 9,000만 달러

CAGR

6.2%

2024년 허브 모터 분야는 66%의 점유율을 차지했으며, 2034년까지 연평균 복합 성장률(CAGR)은 5.5%로 예측됩니다. 앞바퀴 또는 뒷바퀴에 장착되는 허브 모터는 부품 수가 적고 심플한 설계로 제조 비용과 유지보수 비용을 모두 절감할 수 있습니다. 자전거의 구동계와 독립적으로 작동하기 때문에 도시 통근자나 초보 라이더에게 이상적입니다. 이러한 분리는 체인과 카세트의 마모를 줄이고 유지보수 주기를 더욱 개선하는 데 도움이 됩니다. 저렴한 가격과 심플한 디자인으로 도심에서의 사용에도 적합합니다.

최대 250W의 전기 자전거용 구동장치은 2024년 51%의 점유율을 차지했으며, 2025-2034년 연평균 5.2%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 이 유닛은 전 세계 전기자전거용 모터의 대부분을 차지하고 있으며, 주요 지역의 규제 기준을 충족하고 있습니다. 대부분 시장, 특히 북미, 일본, 유럽에서는 전기자전거용 구동장치의 연속 정격 전력이 250W로 제한되어 있습니다. 이러한 규제 정합성은 많은 라이더의 전력 수요를 충족시키면서 규정 준수를 보장하고 대량 채택을 촉진할 수 있습니다.

아시아태평양 전기자전거용 구동장치 시장 점유율은 38%이며, 2024년에는 17억 8,000만 달러에 달했습니다. 이 지역 전체의 정부 정책과 전략적 도시 계획이 e-모빌리티로의 전환을 가속화하고 있습니다. 일부 국가에서는 전기 자전거를 기존 자전거와 유사하게 취급하여 규제 마찰을 줄이고 사용자 채택을 늘리고 있습니다. e-bike 구매를 보조하는 것을 목표로 하는 대규모 공공 프로그램도 특히 광범위한 소매 네트워크를 통해 지원되는 경우 구동 장치에 대한 수요를 증가시키는 데 큰 역할을 하고 있습니다.

전기자전거용 구동장치 시장에서 활동하는 주요 기업으로는 시마노, 야마하, Bafang, Tongsheng Motor, Bosch, Brose, Dapu Motors, TQ-Group, Valeo, Mahle 등이 있습니다. 이들 기업은 시장에서의 입지를 강화하기 위해 여러 전략을 채택하고 있습니다. 각 회사는 토크 응답, 배터리 효율, 지능형 통합을 개선하기 위해 연구개발에 집중하고 있습니다. 또한, 프리미엄 e-bike나 고성능 e-bike에 자체 제작 유닛이 채택될 수 있도록 OEM과의 제휴를 확대하는 기업도 많습니다. 출퇴근, 트레킹, 화물 등 다양한 이용 사례에 맞는 맞춤형 드라이브 시스템은 브랜드가 소비자층을 확대하는 데 도움이 되고 있습니다. 앱 연결 및 무선 업데이트와 같은 스마트 기능의 통합은 경쟁 구도에서 중요한 차별화 요소가 되고 있습니다.

목차

제1장 조사 방법

시장 범위와 정의

조사 디자인

조사 접근

데이터 수집 방법

데이터 마이닝 소스

세계

지역/국가

기본 추정과 계산

기준 연도 계산

시장 예측 주요 동향

1차 조사와 검증

1차 정보

예보

조사 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 미치는 요인

파괴적 변화

업계에 대한 영향요인

성장 촉진요인

업계의 잠재적 리스크&과제

시장 기회

성장 가능성 분석

특허 분석

Porter의 Five Forces 분석

PESTEL 분석

성장 가능성 분석

규제 상황

Porter의 Five Forces 분석

PESTEL 분석

기술 및 혁신 상황

현재 기술 동향

AI를 활용한 적응 제어 시스템

머신러닝 통합 기능

예지보전과 고장 예방

에너지 최적화와 항속거리 연장

무선 충전 통합과 인프라

고체 배터리 통합 영향

차량과 그리드 통합과 에너지 서비스

자율형 및 자기 밸런스 시스템

신기술

가격 동향

지역별

제품별

투자 및 자금조달 동향 분석

보안 실장 전략

하드웨어 보안 모듈 통합

암호화된 통신 프로토콜

시큐어 부트 및 펌웨어 보호

침입 감지 및 대응 시스템

규제 상황

데이터 보호 규제 준수

사이버 보안 프레임워크 요건

업계 고유 보안 표준

인증 및 감사 요건

진단 툴과 기기 요건

제조업체 고유 진단 시스템

서비스 기기 표준화

지속가능성과 ESG의 영향 분석

지속가능성과 ESG의 영향 분석

사회적 영향과 지역사회와의 관계

거버넌스와 기업 책임

보증 서비스와 비용 분석

보증 범위 비교

보증 청구 분석

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

시장 개척 전략

고객 만족도 벤치마킹

주요 발전

인수합병(M&A)

파트너십 및 협업

신제품 발매

확장 계획과 자금조달

제5장 시장 추산·예측 : 모터 마운트별, 2021년-2034년

주요 동향

허브 모터

Rear

Front

Mid-drive motor

제6장 시장 추산·예측 : 용량별, 2021년-2034년

주요 동향

최대 250W

250W-550W

550W 이상

제7장 시장 추산·예측 : 용도별, 2021년-2034년

주요 동향

카고 바이크

최대 250W

250W-550W

550W 이상

트렉킹 바이크

최대 250W

250W-550W

550W 이상

시티 바이크

최대 250W

250W-550W

550W 이상

제8장 시장 추산·예측 : 유통별, 2021년-2034년

주요 동향

OEM

애프터마켓

제9장 시장 추산·예측 : 지역별, 2021년-2034년

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

북유럽 국가

러시아

아시아태평양

중국

인도

일본

호주

인도네시아

필리핀

태국

한국

싱가포르

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

사우디아라비아

남아프리카공화국

아랍에미리트(UAE)

제10장 기업 개요

세계 기업

Bosch

Shimano

Brose(Acquired by Yamaha)

Yamaha

Valeo

Mahle

Dapu Motors

지역 기업

Fazua

TQ-Group

Pinion

Zehus

SHINWIN

Ananda Drive Technology

Bafang

Tongsheng Motor

신규 기업/파괴적 혁신

To7 Motor

Tamobyke

Karmina E-bike

GOBAO

Suzhou Shengyi Motor

SEG Automotive

LSH

영문 목차

영문목차

The Global E-Bike Drive Unit Market was valued at USD 4.68 billion in 2024 and is estimated to grow at a CAGR of 6.2% to reach USD 8.49 billion by 2034.

As electric mobility becomes more mainstream, the demand for efficient and intelligent drive systems continues to rise. These drive units combine motors, control systems, and sensors that assist or fully power the e-bike, improving user experience. Over the years, technology has evolved from basic hub motors to sophisticated systems with integrated electronics and software. Drive units often feature torque sensors, regenerative braking, and intelligent connectivity, making them highly efficient and smarter for varied terrains and urban use. Mid-drive units are increasingly popular in trekking, mountain, and cargo bikes due to their balanced weight distribution, better torque, and seamless integration with existing drivetrains. Improvements in modular battery design and connectivity features are driving up the overall value of these systems. OEMs dominate the supply chain, offering complete solutions to bicycle manufacturers and forming critical partnerships during product development. Although the aftermarket for conversion kits and replacement motors exists, it contributes only a small portion to total revenue, with most sales rooted in OEM-led manufacturing channels.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$4.68 Billion

Forecast Value

$8.49 Billion

CAGR

6.2%

In 2024, the hub motor segment held a 66% share and is projected to grow at a CAGR of 5.5% through 2034. Built into either the front or rear wheel, hub motors offer a simplified design that requires fewer components, lowering both production and maintenance costs. Their independent operation from the bike's drivetrain makes them ideal for urban commuters and entry-level riders. This separation helps reduce wear on chains and cassettes, further improving maintenance cycles. Their affordability and simplicity keep them highly relevant for city-focused applications.

The e-bike drive units up to 250 W segment held a 51% share in 2024 and is expected to grow at a CAGR of 5.2% from 2025 to 2034. These units represent the bulk of e-bike motors globally and align with regulatory standards in key regions. Most markets, especially in North America, Japan, and Europe limit e-bike drive units to a continuous power rating of 250 W. This regulatory alignment encourages mass adoption, ensuring compliance while meeting the power needs of most riders.

Asia Pacific E-Bike Drive Unit Market held 38% share and generated USD 1.78 billion in 2024. Government policies and strategic urban planning across the region are accelerating the shift to e-mobility. In several countries, e-bikes are treated similarly to traditional bicycles, reducing regulatory friction and increasing user adoption. Large-scale public programs aimed at subsidizing e-bike purchases have also played a major role in boosting demand for drive units, especially when supported through wide-reaching retail networks.

Key companies active in the E-Bike Drive Unit Market include Shimano, Yamaha, Bafang, Tongsheng Motor, Bosch, Brose, Dapu Motors, TQ-Group, Valeo, and Mahle. These players are adopting multiple strategies to strengthen their market position. Companies are focusing on R&D to improve torque response, battery efficiency, and intelligent integration. Many have expanded OEM partnerships to ensure their units are adopted in premium and performance e-bikes. Customizable drive systems for different use cases, commuting, trekking, and cargo, are helping brands widen their consumer base. Integration of smart features such as app connectivity and over-the-air updates is becoming a key differentiator in a competitive landscape.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Regional

2.2.2 Motor mounting

2.2.3 Capacity

2.2.4 Application

2.2.5 Distribution

2.3 TAM analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future-outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factors affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Urban congestion and commuting challenges

3.2.1.2 Government incentives and subsidies

3.2.1.3 Growth in fitness and eco-conscious lifestyles

3.2.1.4 Technological advancements in drive systems

3.2.1.5 Expansion of e-bike sharing and rental services

3.2.1.6 Rising fuel prices and vehicle ownership costs

3.2.2 Industry pitfalls and challenges

3.2.2.1 High cost of advanced drive units

3.2.2.2 Limited charging infrastructure

3.2.3 Market opportunities

3.2.3.1 Development of lightweight, compact drive units

3.2.3.2 Integration of smart and connected technologies