기계식 인공호흡기 시장 : 시장 기회 및 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Mechanical Ventilators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1844327

리서치사:Global Market Insights Inc.

발행일:2025년 09월

페이지 정보:영문 160 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

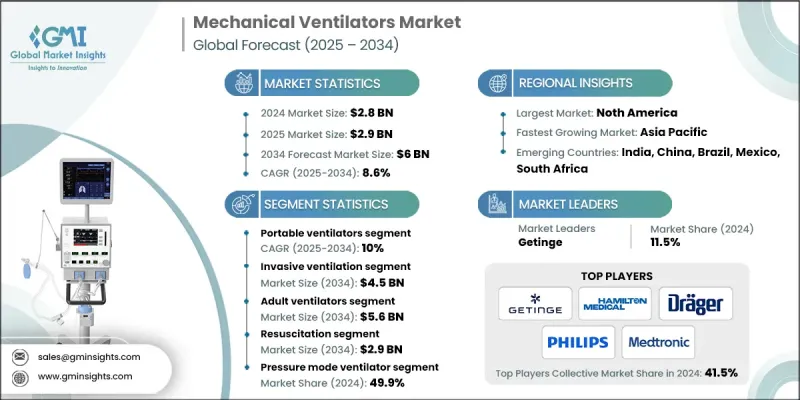

세계의 기계식 인공호흡기 시장 규모는 2024년에 28억 달러로 평가되었고, CAGR 8.6%로 성장할 전망이며, 2034년에는 60억 달러에 이를 것으로 예측되고 있습니다.

성장의 원동력이 되고 있는 것은 ICU 입실 증가, 호흡기 질환의 부담 증가, 의료의 급속한 진보, 세계적인 집중 치료 서비스 수요 증가입니다. 의료 제공자와 생명과학 기업은 중요한 호흡 지원을 제공할 뿐만 아니라 규제 준수, 업무 효율성 및 전반적인 환자 결과 개선에도 도움이 되는 기계식 환기 시스템에 주목하고 있습니다. 이 시스템에는 휴대용 및 심각한 환자 유닛에서 침습적 및 비침습적 모델에 이르기까지 다양한 솔루션이 있으며, 치료 제공 및 환자의 안전성을 높이기 위한 디지털 호흡 모니터링이 장착되어 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시장 규모

28억 달러

예측 금액

60억 달러

CAGR

8.6%

수면 무호흡 증후군, 천식, 만성 폐색성 폐 질환과 같은 장기 호흡기 질환의 이환율 증가는 인공 호흡기 수요에 크게 기여합니다. 또한 스마트 모니터링, 통합 AI, 사용자 친화적인 인공호흡기 인터페이스 등의 첨단 기술로 케어 수준이 향상되고 있는 것도 시장 성장에 박차를 가하고 있습니다. 병원과 재택치료 환경이 보다 비용 효율적인 환자 중심 케어 모델을 채택하는 동안 휴대용 및 원격 사용형 인공호흡기로의 이동은 계속 가속화되고 있습니다. 특히 신흥경제국에서는 의료 인프라에 대한 투자가 증가하고 있어 접근성이 향상되고 병원 및 외과 치료의 두 분야에서 시장 침투가 진행되고 있습니다.

2024년 휴대용 인공호흡기 부문의 매출은 4억 7,240만 달러로 평가되었고, 2034년까지 10%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다. 가정이나 긴급 상황에서 지속적인 호흡 관리가 필요한 환자가 증가함에 따라 수요가 크게 증가하고 있습니다. 만성 호흡기 질환은 환자와 간병인 모두에게 이동성과 사용 편의성을 향상시키면서 장기적인 지원을 제공하는 모바일 솔루션의 사용을 촉진하여 시장에서 컴팩트하고 휴대 가능한 장치의 관련성을 강화합니다.

침습적 인공호흡기 부문은 2024년에 77.5%의 점유율을 차지하였고, 2034년에는 45억 달러에 이를 것으로 추정됩니다. 이러한 시스템은 특히 집중 치료 환경에서 심한 호흡기 질환과 생명을 위협하는 합병증을 관리하는 데 필수적입니다. 이 분야의 성장 배경에는 세계적인 ICU 시설의 급증과 급성 호흡기 질환 증가가 있습니다. 침습적 인공호흡기는 높은 수준의 호흡 지원을 제공할 수 있기 때문에 병원과 외상 치료실의 지속적인 투자를 지원합니다.

북미의 기계식 인공호흡기 2024년 시장 점유율은 36.7%로 평가되었고, 성숙한 헬스케어 시스템, 의료기술에 많은 지출, 중증 환자 케어를 위한 강력한 인프라가 이를 지원하고 있습니다. 인구 고령화 및 호흡기 시스템의 건강 부담 증가로 병원 기반과 가정 기반 모두 인공호흡 시스템에 대한 수요가 증가하고 있습니다. 연구 투자, 첨단 헬스케어 접근, 진단률 향상으로 이 지역 전반에 걸쳐 급속한 기술 도입이 진행되고 있습니다.

기계식 인공호흡기 시장의 주요 기업으로는 ZOLL Medical, Medtronic, ResMed, Philips, Mindray, Noccarc Robotics, Bio-Med Devices, Baxter, Fisher & Paykel, Hamilton Medical, Getinge, Drager, ICU Medical, GE HealthCare, Nihon Kohden, ACOMA Medical, Carl Reiner, Aeonmed, Breas Medical, Air Liquide Medical Systems, Allied Medical, Foremost Meditech, and Skanray Technologies 등이 있습니다. 기계식 인공호흡기 시장의 지위를 강화하기 위해 제조업체는 기술 혁신, 제품 다양화 및 전략적 파트너십에 주력하고 있습니다. 각 회사는 실시간 환자 모니터링과 데이터 중심의 인사이트를 제공하기 위해 AI 통합형 및 IoT 대응 인공호흡기를 개발하고 있습니다. 또한 의료 환경 전반에 걸친 수요 증가에 대응하기 위해 병원 등급과 휴대용 기기 모두로 제품을 확대하고 있습니다. 제조 및 애프터서비스 센터의 현지화는 리드타임 단축과 시장 대응력 향상에 도움이 됩니다. 또한 의료 서비스 제공업체와의 합병, 인수 및 제휴로 유통망이 강화되고 연구개발 능력이 육성되고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

업계에 미치는 영향요인

성장 촉진요인

만성 호흡기 질환 유병률 증가

헬스케어비 증가

집중치료실의 병상수 증가

기술적 진보

업계의 잠재적 위험 및 과제

인공호흡기 사용에 따른 위험

기계식 인공호흡기의 고비용

시장 기회

재택 케어 및 비침습적 환기 증가

AI 및 원격 모니터링의 통합

성장 가능성 분석

규제 상황

기술의 상황

현재의 기술 동향

휴대용 및 홈 기반 기계식 인공 호흡기의 성장

원격 모니터링을 가능하게 하는 디지털 헬스 플랫폼

고급 환자-인공 호흡기 인터페이스

신흥 기술

AI 탑재 인공호흡기 및 예측 분석

웨어러블 및 커넥티드 인공호흡기 시스템

IoT 및 클라우드 기능을 통합한 스마트 인공호흡기

갭 분석

Porter's Five Forces 분석

PESTEL 분석

장래 시장 동향

재택 케어 및 휴대용 인공호흡기의 확대

원격 모니터링 및 원격 의료 도입

소형화 및 웨어러블 인공호흡기

제4장 경쟁 구도

서문

기업 매트릭스 분석

기업의 시장 점유율 분석

세계

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

경쟁 포지셔닝 매트릭스

주요 시장 기업의 경쟁 분석

주요 발전

합병 및 인수

파트너십 및 협업

새로운 서비스 유형의 개시

확장 계획

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

주요 동향

집중치료용 인공호흡기

하이엔드

미드엔드

베이직 엔드

휴대용 인공호흡기

제6장 시장 추계 및 예측 : 인터페이스별(2021-2034년)

주요 동향

침습적 환기

CPAP

바이팝

어팍

기타 비침습적 환기

비침습적 환기

제7장 시장 추계 및 예측 : 인공호흡기 유형별(2021-2034년)

주요 동향

성인용 인공호흡기

신생아용 인공호흡기

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

소생

긴급 및 운송

마취과

임상 용도

홈케어 용도

수면 무호흡 증후군 치료

기타 용도

제9장 시장 추계 및 예측 : 모드별(2021-2034년)

주요 동향

압력모드 인공호흡기

제어모드 인공호흡기

복합모드 인공호흡기

제10장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

주요 동향

병원

외래수술센터(ASC)

홈케어

기타 용도

제11장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

네덜란드

아시아태평양

중국

일본

인도

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제12장 기업 프로파일

ACOMA Medical

Aeonmed

Air Liquide Medical Systems

Allied Medical

Baxter

Bio-Med Devices

Breas Medical

Carl Reiner

Drager

Foremost Meditech

Fisher & Paykel

GE Healthcare

Getinge

Hamilton Medical

ICU Medical

Medtronic

Mindray

Nihon Kohden

Noccarc Robotics

Philips

ResMed

Skanray Technologies

ZOLL Medical

AJY

영문 목차

영문목차

The Global Mechanical Ventilators Market was valued at USD 2.8 billion in 2024 and is estimated to grow at a CAGR of 8.6% to reach USD 6 billion by 2034.

Growth is driven by increasing ICU admissions, a rising burden of respiratory disorders, rapid medical advancements, and a higher demand for intensive care services worldwide. Healthcare providers and life sciences firms are turning to mechanical ventilation systems that offer not only critical respiratory support but also help improve regulatory compliance, operational efficiency, and overall patient outcomes. These systems include a wide variety of solutions, ranging from portable and critical care units to invasive and non-invasive models, equipped with digital respiratory monitoring for enhanced treatment delivery and patient safety.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$2.8 Billion

Forecast Value

$6 Billion

CAGR

8.6%

The growing incidence of long-term respiratory conditions such as sleep apnea, asthma, and chronic obstructive pulmonary disease is contributing heavily to the demand for ventilators. Market growth is also being fueled by advanced technologies like smart monitoring, integrated AI, and user-friendly ventilator interfaces that are elevating care standards. As hospitals and home care environments adopt more cost-effective and patient-centered care models, the shift toward portable and remote-use ventilators continues to accelerate. Rising healthcare infrastructure investments especially in developing economies are increasing accessibility and broadening market penetration across both hospital and surgical care segments.

In 2024, the portable ventilators segment generated USD 472.4 million and is expected to grow at a 10% CAGR through 2034. Demand is rising significantly as more patients require ongoing respiratory care in home-based or emergency scenarios. Chronic respiratory illnesses are prompting the use of mobile solutions that offer long-term support with increased mobility and ease of use for both patients and caregivers, reinforcing the relevance of compact, transportable units in the market.

The invasive ventilators segment held a 77.5% share in 2024 and is estimated to reach USD 4.5 billion by 2034. These systems are essential for managing severe respiratory conditions and life-threatening complications, particularly in intensive care settings. Growth in this segment is backed by a surge in ICU facilities worldwide and the rise in acute respiratory conditions. The ability of invasive ventilators to offer high levels of respiratory support is driving continued investment from hospitals and trauma care units.

North America Mechanical Ventilators Market held 36.7% share in 2024, supported by a mature healthcare system, significant spending on medical technologies, and a strong infrastructure for critical care. The aging population and growing respiratory health burden have elevated demand for both hospital-based and home-based ventilatory systems. Investments in research, access to advanced healthcare, and higher diagnosis rates have enabled rapid technology adoption across the region.

Leading companies in the Mechanical Ventilators Market include ZOLL Medical, Medtronic, ResMed, Philips, Mindray, Noccarc Robotics, Bio-Med Devices, Baxter, Fisher & Paykel, Hamilton Medical, Getinge, Drager, ICU Medical, GE Healthcare, Nihon Kohden, ACOMA Medical, Carl Reiner, Aeonmed, Breas Medical, Air Liquide Medical Systems, Allied Medical, Foremost Meditech, and Skanray Technologies. To strengthen their position in the Mechanical Ventilators Market, manufacturers are focusing on technological innovation, product diversification, and strategic partnerships. Companies are developing AI-integrated and IoT-enabled ventilators to deliver real-time patient monitoring and data-driven insights. They are also expanding their offerings to include both hospital-grade and portable devices to meet growing demand across care settings. Localization of manufacturing and after-sales service centers is helping reduce lead times and improve market responsiveness. Additionally, mergers, acquisitions, and collaborations with healthcare providers are enhancing distribution networks and fostering R&D capabilities.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definitions

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional trends

2.2.2 Product trends

2.2.3 Interface trends

2.2.4 Ventilator type trends

2.2.5 Application trends

2.2.6 Mode trends

2.2.7 End use trends

2.3 CXO perspectives: Strategic imperatives

2.3.1 Key decision points for industry executives

2.3.2 Critical success factors for market players

2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Increasing prevalence of chronic respiratory diseases

3.2.1.2 Rise in healthcare expenditure

3.2.1.3 Increase in number of ICU beds/critical care beds

3.2.1.4 Technological advancements

3.2.2 Industry pitfalls and challenges

3.2.2.1 Risks associated with the use of ventilators

3.2.2.2 High cost of mechanical ventilators

3.2.3 Market opportunities

3.2.3.1 Growth of homecare and non-invasive ventilation

3.2.3.2 Integration of AI and remote monitoring

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 MEA

3.5 Technology landscape

3.5.1 Current technological trends

3.5.1.1 Growth of portable and home-based mechanical ventilators

3.5.1.2 Digital health platforms enabling remote monitoring

3.5.1.3 Advanced patient-ventilator interfaces

3.5.2 Emerging technologies

3.5.2.1 AI-powered ventilators and predictive analytics

3.5.2.2 Wearable and connected ventilator systems

3.5.2.3 Smart ventilators with integrated IoT and cloud capabilities

3.6 Gap analysis

3.7 Porter's analysis

3.8 PESTEL analysis

3.9 Future market trends

3.9.1 Expansion of homecare and portable ventilators

3.9.2 Remote monitoring and telehealth adoption

3.9.3 Miniaturization and wearable ventilators

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company matrix analysis

4.3 Company market share analysis

4.3.1 Global

4.3.2 North America

4.3.3 Europe

4.3.4 Asia Pacific

4.3.5 Latin America

4.3.6 MEA

4.4 Competitive positioning matrix

4.5 Competitive analysis of major market players

4.6 Key developments

4.6.1 Mergers and acquisitions

4.6.2 Partnerships and collaborations

4.6.3 New service type launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn, Units)

5.1 Key trends

5.2 Intensive care ventilators

5.2.1 High-end

5.2.2 Mid-end

5.2.3 Basic-end

5.3 Portable ventilators

Chapter 6 Market Estimates and Forecast, By Interface, 2021 - 2034 ($ Mn, Units)

6.1 Key trends

6.2 Invasive ventilation

6.2.1 CPAP

6.2.2 BiPAP

6.2.3 APAP

6.2.4 Other non-invasive ventilation

6.3 Non-invasive ventilation

Chapter 7 Market Estimates and Forecast, By Ventilator Type, 2021 - 2034 ($ Mn, Units)

7.1 Key trends

7.2 Adult ventilators

7.3 Neonatal ventilators

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn, Units)

8.1 Key trends

8.2 Resuscitation

8.3 Emergency/Transport

8.4 Anesthesiology

8.5 Clinical applications

8.6 Homecare applications

8.7 Sleep apnea therapy

8.8 Other applications

Chapter 9 Market Estimates and Forecast, By Mode, 2021 - 2034 ($ Mn, Units)

9.1 Key trends

9.2 Pressure mode ventilator

9.3 Control mode ventilator

9.4 Combined mode ventilator

Chapter 10 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn, Units)

10.1 Key trends

10.2 Hospitals

10.3 Ambulatory surgical centers

10.4 Homecare

10.5 Other end use

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn, Units)