탄도 미사일 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Ballistic Missiles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1844280

리서치사:Global Market Insights Inc.

발행일:2025년 09월

페이지 정보:영문 160 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

세계의 탄도 미사일 시장은 2024년에는 91억 달러로 평가되었고, CAGR 5.1%로 성장할 전망이며, 2034년에는 149억 달러에 이를 것으로 추정됩니다.

이 성장에 기여하는 주요 요인으로는 세계적인 국방비 증가, 시대 지연 미사일 무기의 근대화, 추진 시스템 및 조준 시스템의 기술 진보, 지역 분쟁 및 국제 분쟁의 격화 등이 있습니다. 세계 각국은 전략적 억지력과 신속한 대응 체제의 강화를 목표로 미사일 능력에 대한 투자를 대폭 늘리고 있습니다. 레거시 플랫폼 업그레이드는 보다 정교한 추진 시스템, 향상된 재진입 기술 및 고정밀 조준에 중점을 둡니다. 진화하는 위협은 기존의 미사일 클래스에서 극초음속, 기동 재돌입 차량(MaRVs), 정밀 유도 시스템 등의 보다 고급 유형으로의 전환을 촉진하고 있습니다. 이 개발은 국가 안보 우선 순위 및 현대 전쟁의 복잡성을 모두 반영합니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시장 규모

91억 달러

예측 금액

149억 달러

CAGR

5.1%

단거리 탄도 미사일(SRBM) 분야는 지역 분쟁 시나리오에서 전술적 이점, 신속한 배치 능력 및 비용 효율성으로 2024년 32.9%의 점유율을 차지했습니다. 예산이 제한되고 위협이 많은 환경에서 국가들은 신속한 대응 요구를 충족시키고 억제 태세를 강화하기 위해 이러한 시스템을 채택하고 있습니다. 시장 관계자는 새로운 지역 요건과 근대화 의무를 따르기 때문에 소형 추진력, 확장 가능한 탄두 구성, 조준 강화에 있어서의 기술 혁신을 우선시켜야 합니다.

2024년에는 지상발사형 미사일 부문의 점유율은 51.6%였습니다. 그 매력은 광범위한 페이로드 옵션, 공격 범위 확대, 해상 또는 항공 기반 시스템에 비해 저렴한 비용입니다. 또한 전술 방위 및 장거리 방위 전략을 모두 지원합니다. 경쟁력을 유지하기 위해 제조업체는 차세대 극 초음속 시스템과 고체 추진 시스템을 개발하고 고급 정밀 기술을 통합하고 신흥국 시장에서 확장되는 방위 프로그램과의 연계를 강화할 것을 권장합니다.

미국의 탄도 미사일 시장은 2024년에 31억 달러에 이르렀으며, 전략 미사일과 전술 미사일의 양성능에 대한 지속적인 투자가 그 원동력이 되고 있습니다. 방위 기업은 미사일의 정확성, 신뢰성, 성능 향상에 주력하는 반면, 연방기관과 긴밀하게 연계하여 현재의 군사 현대화 전략에 맞추어야 합니다. 비용 효율적이고 확장 가능한 시스템을 제공하는 것은 장기적인 방위 계약을 확보하는 데 있어서 매우 중요합니다.

이 업계를 형성하고 있는 주요 참가 기업으로는 Roketsan, Northrop Grumman Corporation, BAE Systems plc, RAFAEL Advanced Defense Systems Ltd., MBDA, Lockheed Martin Corporation, Bharat Dynamics Limited, BrahMos Aerospace, Israel Aerospace Industries Ltd. (IAI), and NPO Mashinostroyeniya입니다. 시장에서의 지위를 확보하기 위해, 주요 기업은 최첨단 추진 기술, 고도 유도 시스템, 성능을 높이는 경량 복합재료에 투자하고 있습니다. 또한 장기적인 군사 근대화 목표 및 제품 개발을 일치시키기 위해 국방기관과 적극적으로 제휴하고 있습니다. 억지력과 공격력이 모두 가능한 멀티 레인지 미사일 시스템의 포트폴리오를 확대하는데 중점을 두고 있습니다.

목차

제1장 조사 방법

시장의 범위 및 정의

조사 디자인

조사 접근

데이터 수집 방법

데이터 마이닝 소스

세계

지역 및 국가

기본 추정 및 계산

기준 연도 계산

시장 예측의 주요 동향

1차 조사 및 검증

1차 정보

예측 모델

조사의 전제 및 한계

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

세계의 방위 예산 확대

지정학적 긴장 및 지역 분쟁 증가

노후화한 미사일 시스템의 현대화 및 교환

미사일 유도 및 추진 기술의 진보

전략적 억제력 및 핵능력에 중점 강화

업계의 잠재적 위험 및 과제

탄도 미사일의 높은 연구 개발비 및 생산 비용

엄격한 군비 관리 조약 및 수출 규제

시장 기회

극초음속 및 기동성이 있는 재돌입체(HGV/MaRV)의 개발

공동 방위 프로그램 및 공동 개발 이니셔티브

신흥 방위 시장의 성장(아시아태평양, 중동)

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현재의 기술 동향

신흥 기술

새로운 비즈니스 모델

컴플라이언스 요건

국방 예산 분석

세계의 방위비 동향

지역 방위 예산 배분

북미

유럽

아시아태평양

중동 및 아프리카

라틴아메리카

주요 방위 근대화 프로그램

예산 예측(2025-2034년)

업계의 성장에 미치는 영향

국가별 방위 예산

공급망의 탄력

지정학적 분석

인재 분석

디지털 변혁

합병, 인수 및 전략적 파트너십의 상황

위험 평가 및 관리

주요 계약 체결(2021-2024년)

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 기업의 경쟁 벤치마킹

재무 실적 비교

수익

이익률

연구개발

제품 포트폴리오 비교

제품 라인업의 넓이

기술

혁신

지리적 존재의 비교

세계 실적 분석

서비스 네트워크의 범위

지역별 시장 침투율

경쟁 포지셔닝 매트릭스

리더들

과제자들

팔로워

틈새 기업

전략적 전망 매트릭스

주요 발전(2021-2024년)

합병 및 인수

파트너십 및 협업

기술적 진보

확대 및 투자 전략

디지털 변혁의 대처

신흥기업 및 스타트업 기업 경쟁 구도

제5장 시장 추계 및 예측 : 범위별(2021-2034년)

주요 동향

단거리(1,000 km 미만)

중거리(1,000-3,000 km)

중거리(3,000-5,500 km)

대륙간 거리(5,500 km 초과)

제6장 시장 추계 및 예측 : 발사 플랫폼별(2021-2034년)

주요 동향

지상 베이스

공수

해군

우주 대응

제7장 시장 추계 및 예측 : 추진력별(2021-2034년)

주요 동향

액체 연료

고체 연료

하이브리드

제8장 시장 추계 및 예측 : 가이던스 시스템별(2021-2034년)

주요 동향

관성 항법 시스템(INS)

위성 지원

상급 탐구자

TERCOM/DSMAC

제9장 시장 추계 및 예측 : 스피드별(2021-2034년)

주요 동향

초음속

극초음속

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

네덜란드

아시아태평양

중국

인도

일본

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제11장 기업 프로파일

세계 주요 기업

BAE Systems plc

MBDA

Israel Aerospace Industries Ltd.(IAI)

지역별 주요 기업

북미

Lockheed Martin Corporation

Northrop Grumman Corporation

유럽

Avibras

Elbit Systems

아시아태평양

Bharat Dynamics Limited

BrahMos Aerospace

China Aerospace Science and Technology Corporation(CASC)

Hanwha Aerospace

Roketsan

틈새 기업 및 교란 기업

Makeyev Rocket Design Bureau(GRTs Makeyeva)

NPO Mashinostroyeniya

RAFAEL Advanced Defense Systems Ltd.

AJY

영문 목차

영문목차

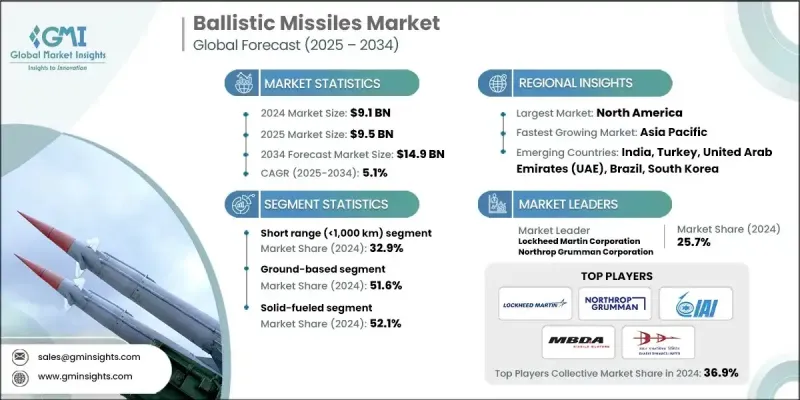

The Global Ballistic Missiles Market was valued at USD 9.1 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 14.9 billion by 2034.

Key drivers contributing to this growth include rising global defense expenditures, the modernization of outdated missile arsenals, technological advancements in propulsion and targeting systems, and intensifying regional and international conflicts. Countries across the world are significantly increasing their investment in missile capabilities, aiming to strengthen both their strategic deterrence and rapid response frameworks. Upgrades to legacy platforms are shifting the focus toward more sophisticated propulsion systems, enhanced re-entry technologies, and precision targeting. The evolving threat is pushing the transition from conventional missile classes to more advanced types such as hypersonic, maneuverable reentry vehicles (MaRVs), and precision-guided systems. This development reflects both national security priorities and the growing complexity of modern warfare.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$9.1 billion

Forecast Value

$14.9 billion

CAGR

5.1%

The short-range ballistic missile (SRBM) segment held a 32.9% share in 2024 owing to its tactical advantages in regional conflict scenarios, rapid deployment capabilities, and cost-efficiency. Nations with limited budgets and high-threat environments are adopting these systems to meet fast-response needs and strengthen deterrent postures. Market players should prioritize innovation in compact propulsion, scalable warhead configurations, and enhanced targeting to align with emerging regional requirements and modernization mandates.

In 2024, the ground-based missile segment held a 51.6% share. Its appeal lies in broader payload options, extended strike range, and lower cost relative to sea or air-based systems. It also supports both tactical and long-range defense strategies. To remain competitive, manufacturers are encouraged to develop next-generation hypersonic and solid-propelled systems, integrate advanced precision technologies, and increase collaboration with expanding defense programs in newer markets.

U.S. Ballistic Missile Market reached USD 3.1 billion in 2024, driven by sustained investment in both strategic and tactical missile capabilities. Defense firms should focus on boosting the accuracy, reliability, and performance of missiles while working closely with federal agencies to align with current military modernization strategies. Providing cost-effective, scalable systems remains crucial in securing long-term defense contracts.

Major participants shaping the industry include Roketsan, Northrop Grumman Corporation, BAE Systems plc, RAFAEL Advanced Defense Systems Ltd., MBDA, Lockheed Martin Corporation, Bharat Dynamics Limited, BrahMos Aerospace, Israel Aerospace Industries Ltd. (IAI), and NPO Mashinostroyeniya. To secure their market position, leading companies are investing in cutting-edge propulsion technologies, advanced guidance systems, and lightweight composite materials that enhance performance. They're also actively partnering with national defense organizations to align product development with long-term military modernization goals. Emphasis is being placed on expanding portfolios with multi-range missile systems capable of both deterrence and offensive capability.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Range trends

2.2.2 Launch platform trends

2.2.3 Propulsion trends

2.2.4 Guidance system trends

2.2.5 Speed trends

2.2.6 Regional trends

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Expansion of defense budgets globally

3.2.1.2 Rising geopolitical tensions and regional conflicts

3.2.1.3 Modernization and replacement of aging missile systems

3.2.1.4 Advancements in missile guidance and propulsion technology

3.2.1.5 Increased focus on strategic deterrence and nuclear capabilities

3.2.2 Industry pitfalls and challenges

3.2.2.1 High R&D and production costs of ballistic missiles

3.2.2.2 Stringent arms control treaties and export regulations

3.2.3 Market opportunities

3.2.3.1 Development of hypersonic and maneuverable re-entry vehicles (HGV/MaRV)

3.2.3.2 Collaborative defense programs and joint development initiatives

3.2.3.3 Growth in emerging defense markets (Asia-Pacific, Middle East)

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter’s analysis

3.6 PESTEL analysis

3.7 Technology and Innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Emerging business models

3.9 Compliance requirements

3.10 Defense budget analysis

3.11 Global defense spending trends

3.12 Regional defense budget allocation

3.12.1 North America

3.12.2 Europe

3.12.3 Asia Pacific

3.12.4 Middle East and Africa

3.12.5 Latin America

3.13 Key defense modernization programs

3.14 Budget forecast (2025-2034)

3.14.1 Impact on industry growth

3.14.2 Defense budgets by country

3.15 Supply chain resilience

3.16 Geopolitical analysis

3.17 Workforce analysis

3.18 Digital transformation

3.19 Mergers, acquisitions, and strategic partnerships landscape

3.20 Risk assessment and management

3.21 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 Latin America

4.2.1.5 Middle East & Africa

4.3 Competitive benchmarking of key players

4.3.1 Financial performance comparison

4.3.1.1 Revenue

4.3.1.2 Profit margin

4.3.1.3 R&D

4.3.2 Product portfolio comparison

4.3.2.1 Product range breadth

4.3.2.2 Technology

4.3.2.3 Innovation

4.3.3 Geographic presence comparison

4.3.3.1 Global footprint analysis

4.3.3.2 Service network coverage

4.3.3.3 Market penetration by region

4.3.4 Competitive positioning matrix

4.3.4.1 Leaders

4.3.4.2 Challengers

4.3.4.3 Followers

4.3.4.4 Niche players

4.3.5 Strategic outlook matrix

4.4 Key developments, 2021-2024

4.4.1 Mergers and acquisitions

4.4.2 Partnerships and collaborations

4.4.3 Technological advancements

4.4.4 Expansion and investment strategies

4.4.5 Digital transformation initiatives

4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Range, 2021 - 2034 (USD Million)

5.1 Key trends

5.2 Short range (<1,000 km)

5.3 Medium range (1,000-3,000 km)

5.4 Intermediate range (3,000-5,500 km)

5.5 Intercontinental range (>5,500 km)

Chapter 6 Market Estimates and Forecast, By Launch Platform, 2021 - 2034 (USD Million)

6.1 Key trends

6.2 Ground-based

6.3 Airborne

6.4 Naval

6.5 Space-enabled

Chapter 7 Market Estimates and Forecast, By Propulsion, 2021 - 2034 (USD Million)

7.1 Key trends

7.2 Liquid-fueled

7.3 Solid-fueled

7.4 Hybrid

Chapter 8 Market Estimates and Forecast, By Guidance System, 2021 - 2034 (USD Million)

8.1 Key trends

8.2 Inertial navigation systems (INS)

8.3 Satellite-aided

8.4 Advanced seekers

8.5 TERCOM / DSMAC

Chapter 9 Market Estimates and Forecast, By Speed, 2021 - 2034 (USD Million)