Heparin Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1833634

리서치사:Global Market Insights Inc.

발행일:2025년 09월

페이지 정보:영문 138 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

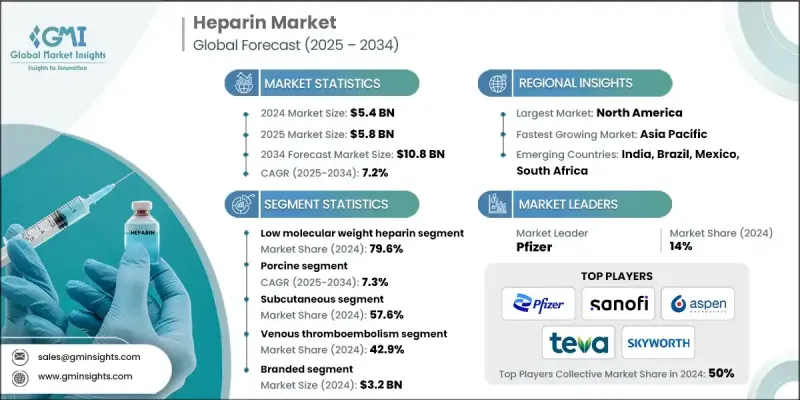

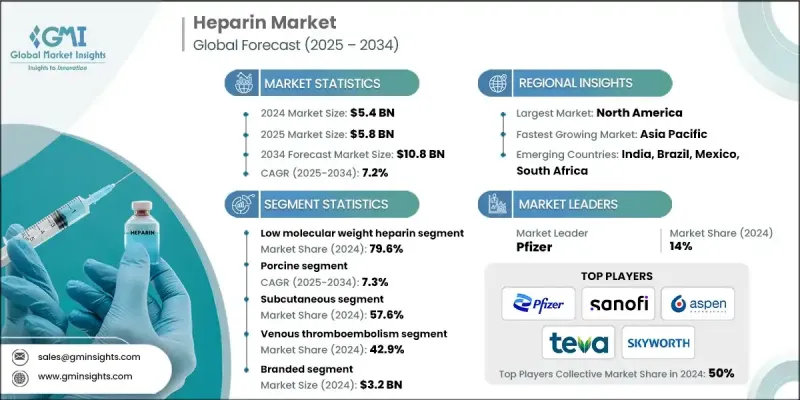

세계의 헤파린 시장은 2024년에는 54억 달러로 평가되었고, CAGR 7.2%로 성장할 전망이며, 2034년에는 108억 달러에 이를 것으로 추정됩니다.

수요 증가는 심혈관 질환 및 혈전성 질환의 급증에 더해, 세계적인 수술 증가에 의한 점이 큽니다. 헤파린은 또한 투석, 암 치료, 다양한 의료기기 용도 분야와 같은 분야에서 널리 채택되었습니다. 이러한 치료법의 확대는 특히 라틴아메리카와 아시아태평양의 신흥 경제권 지역에서 헬스케어 인프라를 개선함으로써 더욱 가속화되고 있습니다. 기술 혁신 및 부작용이 적은 보다 효과적인 항응고요법의 개발에 지속적으로 주력하는 것이 시장 역학을 전진시키고 있습니다. 연구 이니셔티브가 제품의 진보에 박차를 가하고 헤파린 기반 치료 옵션이 병원, 클리닉, 재택 치료 시설에서보다 이용하기 쉬워지고 있습니다. 심혈관 질환은 세계적으로 헬스케어 시스템에 큰 부담을 주고 있기 때문에 항응고 기술의 지속적인 진화는 시장의 보급을 가속할 것으로 예측됩니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시장 규모

54억 달러

예측 금액

108억 달러

CAGR

7.2%

저분자량 헤파린(LMWH) 부문은 2024년에 79.6%의 점유율을 차지했으며, 유리한 약동학, 낮은 출혈 위험, 투여 용이성, 외래 설정에 대한 적합성 등 몇 가지 임상적 이점이 그 원동력이 되고 있습니다. LMWH는 예측 가능한 치료 결과를 제공하고 모니터링 빈도가 적기 때문에 의료 제공업체와 환자가 선호합니다.

포신 유래의 헤파린 분절은 안정한 공급, 임상적 신뢰성, 헤파린 유발성 혈소판 감소증(HIT)과 같은 합병증 발생률의 저하로 2024년 CAGR은 7.3%였습니다. 이 제품 유형의 헤파린은 가장 널리 사용되는 LMWH의 제조에 필수적이며 현재도 대량 생산의 핵심입니다.

미국의 헤파린 시장은 2024년에 28억 달러를 창출했습니다. 이 나라에서는 심혈관 질환 및 만성 질환의 이환율이 높기 때문에 항응고 요법에 대한 수요가 높습니다. FDA에 의한 규제 지원과 유리한 상환의 틀은 브랜드 제제와 제네릭 제제를 모두 널리 받아들입니다. 프리필드 주사기 및 자동 주사기의 병원 및 재택치료에서의 사용 확대도 이러한 약제의 안전하고 편리한 사용에 기여하고 있습니다.

세계의 헤파린 업계를 선도하는 주요 기업으로는 Leo Pharma, Pfizer, Suanfarma, Shenzhen Hepalink Pharmaceuticals, Bioiberica, Amphastar, Sanofi, Dr. Reddy's Laboratories, Changzhou Qianhong Biopharma, Teva Pharmaceutical Industries, Fresenius Kabi, Aspen Pharmacare, Nanjing King-Friend Biochemical Pharmaceutical, Laboratorios Farmaceuticos ROVI, Yantai Dongcheng Biochemicals 등이 있습니다. 헤파린 시장의 선도 기업들은 전략적 제휴, 수직 통합 및 능력 확장을 결합하여 활용하여 시장에서의 입지를 강화하고 있습니다. 일부 기업은 더 나은 효과 및 부작용이 적은 차세대 항응고제를 개발하기 위해 연구 개발에 투자하고 있습니다. 또한 판매 채널 확대 및 원료 공급 확보를 목적으로 제휴 및 라이선싱 계약을 맺고 있는 기업도 있습니다. 성장률이 높은 신흥 시장으로의 지리적 확대도 중요한 중점 분야가 되고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

업계에 미치는 영향요인

성장 촉진요인

세계의 심혈관 질환의 유병률의 상승

고령화 및 외과 수술

병원 인프라 및 재택 케어의 확대

정부 및 기관에 의한 건강에 관한 대처

업계의 잠재적 위험 및 과제

브랜드 LMWH 및 바이오시밀러의 고비용

공급망의 혼란 및 원재료에 대한 의존

시장 기회

합성 및 재조합 기술 개발 헤파린

헬스케어 투자가 증가하는 신흥 시장

성장 가능성 분석

규제 상황

북미

미국

캐나다

유럽

아시아태평양

장래 시장 동향

기술의 상황

현재의 기술

신흥 기술

특허 상황

가격 분석

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

세계

북미

유럽

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병 및 인수

파트너십 및 협업

신제품 발매

확장 계획

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

주요 동향

저분자량 헤파린

미분할 헤파린

초저분자량 헤파린 및 합성 헤파린

제6장 시장 추계 및 예측 : 소스별(2021-2034년)

주요 동향

돼지

소

제7장 시장 추계 및 예측 : 투여 경로별(2021-2034년)

주요 동향

정맥내

피하

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

정맥 혈전 색전증

심방세동 및 조동

관상동맥 질환

기타 용도

제9장 시장 추계 및 예측 : 유형별(2021-2034년)

주요 동향

브랜드

제네릭 의약품

제10장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

주요 동향

병원

클리닉

외래수술센터(ASC)

기타 용도

제11장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

네덜란드

아시아태평양

중국

일본

인도

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제12장 기업 프로파일

Amphastar

Aspen Pharmacare

Bioiberica

Changzhou Qianhong Biopharma

Dr. Reddy’s Laboratories

Fresenius Kabi

Laboratorios Farmaceuticos ROVI

Leo Pharma

Nanjing King-Friend Biochemical Pharmaceutical

Pfizer

Sanofi

Shenzhen Hepalink Pharmaceuticals

Suanfarma

Teva Pharmaceutical Industries

AJY

영문 목차

영문목차

The Global Heparin Market was valued at USD 5.4 billion in 2024 and is estimated to grow at a CAGR of 7.2% to reach USD 10.8 billion by 2034.

The increasing demand is largely attributed to a surge in cardiovascular and thrombotic conditions, coupled with a growing number of surgical interventions worldwide. Heparin is also seeing broader adoption in fields like dialysis, cancer treatment, and various medical device applications. These therapeutic expansions are further amplified by improvements in healthcare infrastructure, particularly in emerging economies across Latin America and the Asia-Pacific region. The continued focus on innovation and the development of more effective anticoagulant therapies with fewer adverse effects is pushing market dynamics forward. Research initiatives are fueling product advancements, making heparin-based treatment options more accessible across hospitals, clinics, and home care facilities. As cardiovascular disease continues to place a substantial burden on healthcare systems globally, the ongoing evolution of anticoagulation technology is expected to accelerate market adoption.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$5.4 Billion

Forecast Value

$10.8 Billion

CAGR

7.2%

The low molecular weight heparin (LMWH) segment held 79.6% share in 2024, driven by several clinical advantages, including its favorable pharmacokinetics, lower risk of bleeding, ease of administration, and suitability for outpatient settings. LMWH offers predictable therapeutic outcomes and requires less frequent monitoring, making it a preferred choice among healthcare providers and patients alike.

The porcine-derived heparin segment held a CAGR of 7.3% in 2024 due to its consistent supply, clinical reliability, and reduced incidence of complications like heparin-induced thrombocytopenia (HIT). This variety of heparin is integral in the manufacturing of the most widely used LMWH types and remains the cornerstone of large-scale production.

United States Heparin Market generated USD 2.8 billion in 2024. The country's high incidence of cardiovascular diseases and chronic health conditions has led to strong demand for anticoagulant therapies. Regulatory support from the FDA, along with favorable reimbursement frameworks, continues to facilitate the widespread acceptance of both branded and generic heparin formulations. The growing use of prefilled syringes and autoinjectors in hospitals and home care environments is also contributing to the safe and convenient use of these medications.

Key companies leading the global heparin industry include Leo Pharma, Pfizer, Suanfarma, Shenzhen Hepalink Pharmaceuticals, Bioiberica, Amphastar, Sanofi, Dr. Reddy's Laboratories, Changzhou Qianhong Biopharma, Teva Pharmaceutical Industries, Fresenius Kabi, Aspen Pharmacare, Nanjing King-Friend Biochemical Pharmaceutical, Laboratorios Farmaceuticos ROVI, and Yantai Dongcheng Biochemicals. Leading players in the heparin market are leveraging a combination of strategic collaborations, vertical integration, and capacity expansion to strengthen their market position. Several companies are investing in R&D to develop next-generation anticoagulants with better efficacy and fewer side effects. Others are entering into partnerships and licensing agreements to broaden distribution channels and secure raw material supplies. Geographic expansion into high-growth emerging markets has also become a critical focus area.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definitions

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumption and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Product

2.2.3 Source

2.2.4 Route of administration

2.2.5 Application

2.2.6 Type

2.2.7 End Use

2.3 CXO perspectives: Strategic imperatives

2.3.1 Key decision points for industry executives

2.3.2 Critical success factors for market players

2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Value addition at each stage

3.1.3 Factor affecting the value chain

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising global cardiovascular disease prevalence

3.2.1.2 Aging population and surgical procedures

3.2.1.3 Expansion of hospital infrastructure and homecare

3.2.1.4 Government and institutional health initiatives

3.2.2 Industry pitfalls and challenges

3.2.2.1 High cost of branded LMWH and biosimilars

3.2.2.2 Supply chain disruptions and raw material dependency

3.2.3 Market opportunities

3.2.3.1 Development of synthetic and recombinant heparin

3.2.3.2 Emerging markets with rising healthcare investment

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 U.S.

3.4.1.2 Canada

3.4.2 Europe

3.4.3 Asia Pacific

3.5 Future market trends

3.6 Technology landscape

3.6.1 Current technology

3.6.2 Emerging technologies

3.7 Patent landscape

3.8 Pricing analysis

3.9 Porter's analysis

3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 Global

4.2.2 North America

4.2.3 Europe

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Merger and acquisition

4.6.2 Partnership and collaboration

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)