Womens Health Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1833436

리서치사:Global Market Insights Inc.

발행일:2025년 09월

페이지 정보:영문 140 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

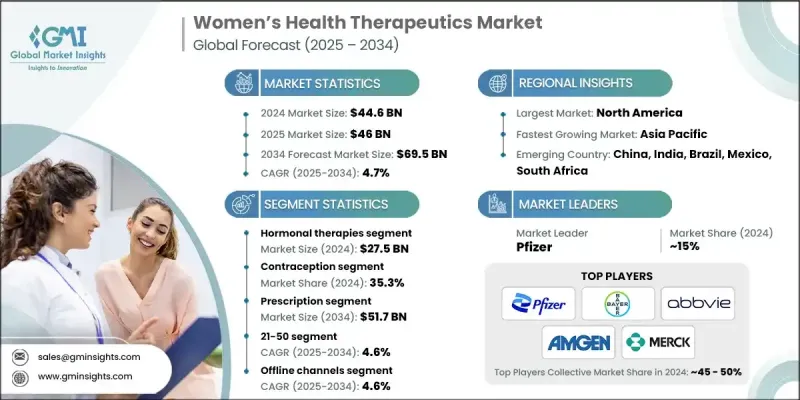

세계의 여성 건강 치료제 시장은 2024년에는 446억 달러로 평가되었고, CAGR 4.7%로 성장하여 2034년에는 695억 달러에 이를 것으로 추정되고 있습니다.

자궁내막증, 폐경, 다낭성난소증후군(PCOS), 골다공증 등의 질환이 점점 더 흔해지고 있습니다. 이러한 질병 부담 증가는 보다 효과적이고 표적화된 치료제에 대한 수요를 증가시키고 있습니다.

시장 범위

개시 연도

2024년

예측 연도

2025-2034년

시장 규모

446억 달러

예측 금액

695억 달러

CAGR

4.7%

호르몬 요법 도입 증가

호르몬 치료 분야는 갱년기 장애, 자궁내막증, 호르몬 균형 장애 등의 증상에 대한 치료 수요 증가로 인해 2024년 큰 점유율을 차지할 것으로 예측됩니다. 호르몬 대체 요법(HRT)과 치료되지 않은 호르몬 문제가 건강에 미치는 장기적인 영향에 대한 인식이 높아짐에 따라, 점점 더 많은 여성들이 의료적 개입을 요구하고 있습니다. 이 시장에서는 패치, 젤, 서방형 임플란트 등 환자 순응도를 높일 수 있는 전달 메커니즘의 혁신이 계속되고 있습니다.

피임 보급률 증가

피임 분야는 장기 지속형 가역적 피임약(LARC)과 비호르몬 피임약에 대한 수요 증가로 인해 2024년 큰 점유율을 차지할 것으로 예측됩니다. 현대인의 라이프스타일, 가족계획의 지연, 생식 자율성에 대한 공중보건적 지원 증가는 다양한 계층에 대한 보급에 박차를 가하고 있습니다. 시장은 기존의 경구피임약에 그치지 않고 질링, 자궁내피임기구(IUD), 피임주사제 등 혁신적인 제품들로 진화하고 있습니다.

처방약에 의한 견인

골다공증, 불임, 부인과 암 등의 치료에는 임상적 특성이 있기 때문에 2024년에는 처방약 부문이 큰 비중을 차지할 것으로 예측됩니다. 의사는 여전히 중요한 의사결정권자이며, 처방된 의약품에 대한 환자의 신뢰는 브랜드 충성도를 지속적으로 견인하고 있습니다. 규제 당국의 승인 경로, 포뮬러의 포지셔닝, 보험 적용은 이 부문의 매출 실적에 큰 영향을 미칩니다.

북미는 추진력 있는 지역으로

북미 여성 건강 치료제 시장은 2025년부터 2034년까지 적절한 CAGR로 성장할 것으로 예측됩니다. 이 지역은 선진적인 의료 인프라, 강력한 규제 감독, 환자와 의료 제공업체 모두의 높은 의식 수준 등의 이점을 누리고 있습니다. 시장 참여자들은 유리한 상환 정책과 사춘기부터 폐경 후까지 여성의 생애주기별 단계별 표적 치료에 대한 수요 증가를 활용하고 있습니다.

여성 건강 치료제 시장의 주요 기업은 Theramex, Cipla, Kissei Pharmaceuticals, Evofem, Pfizer, Shionogi, Ferring, Organon, Amgen, Besins, Allergan(AbbVie), Sanofi, Gedeon Richter, Lupin Atossa Therapeutics,Novartis,Johnson &Johnson,Bayer입니다.

여성 건강 치료 분야 시장 기반을 강화하기 위해 각 업체들은 다각적인 접근에 주력하고 있습니다. 주요 전략으로는 특히 자궁근종, 여성 성기능 장애 등 치료제가 부족한 질환에 대한 자체 연구개발 및 라이선스 계약을 통한 제품 파이프라인 확대가 있습니다. M&&A 또한 시장에서의 존재감을 높이고 혁신적인 기술에 대한 접근성을 확보하기 위해 활용되고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

각 단계에서의 부가가치

밸류체인에 영향을 미치는 요인

업계에 대한 영향요인

성장 촉진요인

만성질환 및 생활습관병 이환율 상승

교육과 공중위생 캠페인 강화

맞춤형 의료 진보

월경 건강과 위생에 관한 치료제 수요 증가

업계의 잠재적 리스크&과제

월경, 불임, 갱년기에 관한 사회적 편견

치료비가 높은

규제상 과제

시장 기회

신흥 시장에의 확대

여성 예방 헬스케어에 대한 주목이 높아진다

성장 가능성 분석

규제 상황

파이프라인 분석

여성 건강 분야 투자 및 자금조달 상황

기술적 상황

향후 시장 동향

Porter의 Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

서론

기업 매트릭스 분석

기업의 시장 점유율 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

인수합병(M&A)

파트너십 및 협업

신제품 발매

확장 계획

제5장 시장 추산·예측 : 약제 유형별, 2021-2034

주요 동향

호르몬 요법

통증과 증상 관리약

GnRH 모듈레이터

뼈 건강 촉진제

대사약

불임 치료제

기타 약물 유형

제6장 시장 추산·예측 : 용도별, 2021-2034

주요 동향

피임

갱년기와 폐경 후 관리

호르몬 장애

자궁내막증과 자궁근종

생식 보건과 불임 치료

뼈 건강과 골다공증

기타 용도

제7장 시장 추산·예측 : 약 유형별, 2021-2034

주요 동향

시판약(OTC)

처방전

제8장 시장 추산·예측 : 연령별, 2021-2034

주요 동향

20세 미만

21-50

51세 이상

제9장 시장 추산·예측 : 유통 채널별, 2021-2034

주요 동향

오프라인 채널

병원 약국

소매 약국

기타 오프라인 스토어

온라인 채널

제10장 시장 추산·예측 : 지역별, 2021-2034

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

네덜란드

아시아태평양

중국

일본

인도

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카공화국

사우디아라비아

아랍에미리트

제11장 기업 개요

Allergan(AbbVie)

Amgen

Atossa Therapeutics

Bayer

Besins

Cipla

Evofem

Ferring

Gedeon Richter

Johnson &Johnson

Kissei Pharmaceutical

Lupin

Novartis

Organon

Pfizer

Sanofi

Shionogi

Theramex

LSH

영문 목차

영문목차

The Global Womens Health Therapeutics Market was valued at USD 44.6 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 69.5 billion by 2034.

Conditions like endometriosis, menopause-related issues, polycystic ovary syndrome (PCOS), and osteoporosis is increasingly common. This growing disease burden is pushing demand for more effective and targeted therapeutics.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$44.6 Billion

Forecast Value

$69.5 Billion

CAGR

4.7%

Increasing Adoption of Hormonal Therapies

The hormonal therapies segment held a significant share in 2024, driven by the rising demand for treatments that address conditions such as menopause symptoms, endometriosis, and hormonal imbalances. As awareness grows around hormone replacement therapy (HRT) and the long-term health impacts of untreated hormonal issues, more women are seeking medical intervention. The market has seen continuous innovation in delivery mechanisms, including patches, gels, and sustained-release implants, which enhance patient compliance.

Rising Prevalence of Contraception

The contraception segment generated a sizeable share in 2024, driven by rising demand for both long-acting reversible contraceptives (LARCs) and non-hormonal options. Modern lifestyles, delayed family planning, and growing public health support for reproductive autonomy have fueled adoption across a broad demographic. The market is evolving beyond traditional oral contraceptives, with innovations in vaginal rings, intrauterine devices (IUDs), and injectable formats.

Prescription to Gain Traction

The prescription segment held a substantial share in 2024, owing to the clinical nature of most treatments for conditions like osteoporosis, fertility issues, and gynecological cancers. Physicians remain key decision-makers, and patient trust in prescribed medications continues to drive brand loyalty. Regulatory approval pathways, formulary positioning, and insurance coverage significantly impact sales performance in this segment.

North America to Emerge as a Propelling Region

North America womens health therapeutics market is poised to grow at a decent CAGR during 2025-2034. The region benefits from advanced healthcare infrastructure, strong regulatory oversight, and high awareness levels among both patients and providers. Market players are capitalizing on favorable reimbursement policies and rising demand for targeted treatments across various stages of a woman's life cycle, from adolescence to post-menopause.

Major players in the women's health therapeutics market are Theramex, Cipla, Kissei Pharmaceutical, Evofem, Pfizer, Shionogi, Ferring, Organon, Amgen, Besins, Allergan (AbbVie), Sanofi, Gedeon Richter, Lupin, Atossa Therapeutics, Novartis, Johnson & Johnson, and Bayer.

To strengthen their market foothold in the women's health therapeutics space, companies are focusing on a multi-pronged approach. Key strategies include expanding product pipelines through in-house R&D and licensing deals, particularly for underserved conditions such as uterine fibroids and female sexual dysfunction. Mergers and acquisitions are also being used to consolidate market presence and gain access to innovative technologies.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Drug type

2.2.3 Application

2.2.4 Medication type

2.2.5 Age group

2.2.6 Distribution channel

2.3 CXO perspectives: Strategic imperatives

2.3.1 Key decision points for industry executives

2.3.2 Critical success factors for market players

2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Value addition at each stage

3.1.3 Factors affecting the value chain

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising prevalence of chronic and lifestyle diseases

3.2.1.2 Enhanced education and public health campaigns

3.2.1.3 Growing advancement in personalized medicine

3.2.1.4 Increasing demand for menstrual health and hygiene therapeutics

3.2.2 Industry pitfalls and challenges

3.2.2.1 Social stigma around menstruation, infertility, and menopause

3.2.2.2 High treatment cost

3.2.2.3 Regulatory challenges

3.2.3 Market opportunities

3.2.3.1 Expansion in emerging markets

3.2.3.2 Growing focus on preventive women's healthcare

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East and Africa

3.5 Pipeline analysis

3.6 Investment and funding landscape in the women's health sector

3.7 Technological landscape

3.8 Future market trends

3.9 Porter’s analysis

3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company matrix analysis

4.3 Company market share analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Merger and acquisition

4.6.2 Partnership and collaboration

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Type, 2021 - 2034 ($ Mn)

5.1 Key trends

5.2 Hormonal therapies

5.3 Pain and symptom management drugs

5.4 GnRH modulators

5.5 Bone health agents

5.6 Metabolic drugs

5.7 Fertility drugs

5.8 Other drug types

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

6.1 Key trends

6.2 Contraception

6.3 Menopause and post-menopausal management

6.4 Hormonal disorders

6.5 Endometriosis and uterine fibroids

6.6 Reproductive health and fertility care

6.7 Bone health and osteoporosis

6.8 Other applications

Chapter 7 Market Estimates and Forecast, By Medication Type, 2021 - 2034 ($ Mn)

7.1 Key trends

7.2 Over the counter (OTC)

7.3 Prescription

Chapter 8 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

8.1 Key trends

8.2 Below 20

8.3 21-50

8.4 51 and above

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

9.1 Key trends

9.2 Offline channels

9.2.1 Hospital pharmacies

9.2.2 Retail pharmacies

9.2.3 Other offline stores

9.3 Online channels

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)