의료용 장갑 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)

Medical Gloves Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1822658

리서치사:Global Market Insights Inc.

발행일:2025년 08월

페이지 정보:영문 170 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

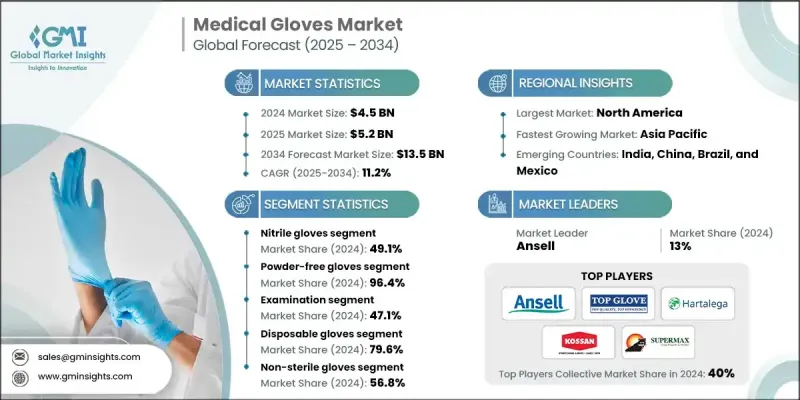

Global Market Insights Inc.가 발행한 최신 보고서에 따르면 세계의 의료용 장갑 시장은 2024년에 45억 달러로 평가되었고, CAGR은 11.2%를 나타낼 것으로 예측되며 2025년 52억 달러에서 2034년에 135억 달러로 성장할 전망입니다.

병원, 클리닉 및 진단 센터는 감염 관리 프로토콜을 최우선으로 하여 환자 간 및 의료진 간 교차 오염 위험을 감축하기 위한 일회용 의료용 장갑에 대한 꾸준한 수요를 촉진하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시장 규모

45억 달러

예측 금액

135억 달러

CAGR

11.2%

니트릴 장갑 부문 수요 증가

니트릴 장갑 부문은 우수한 내화학성, 내구성 및 저알레르기성 특성으로 인해 2024년에 강력한 성장세를 촉진되었습니다. 라텍스 장갑과 달리 니트릴 장갑은 라텍스 알레르기가 있는 환자와 의료진 모두에게 더 안전한 대안을 제공합니다. 이러한 장갑은 강도와 찔림 저항성이 중요한 수술 환경, 응급실 및 진단 실험실에서 점점 더 선호되고 있습니다. 합성 소재로의 수요 전환과 직업 안전 기준에 대한 인식 제고에 힘입어 해당 부문은 지속적으로 확대되고 있습니다.

파우더 프리 장갑의 성장 가속화

규제 제한과 장갑 파우더로 인한 알레르기 반응 우려로 인해 파우더 프리 장갑 부문은 2024년 상당한 매출을 기록했습니다. 이 장갑은 피부 안전성을 향상시키고 환자 치료 및 수술 절차 중 오염 위험을 감축합니다. 또한 분말 없이도 착용이 용이하도록 제조 기술이 개선되어 채택이 촉진되고 있습니다. FDA와 같은 규제 기관이 분말 처리된 의료용 장갑을 금지함에 따라 분말 없는 장갑 부문은 상당한 시장 변화를 가지고 있습니다. 제조업체들은 이 부문 내에서 편안함, 그립감, 촉각 감도를 향상시키는 혁신을 지속하며, 분말 없는 장갑을 최근 의료 프로토콜의 핵심 요소로 만들고 있습니다.

지역별 인사이트

북미가 유리한 지역으로 상승

북미의 의료용 장갑 시장은 2024년 강력한 의료 인프라, 엄격한 안전 규정, 감염 관리에 대한 높은 인식에 의해 촉진되어 상당한 점유율을 기록했습니다. 미국은 병원, 외래 진료 시설, 진단 센터 전반에 걸친 광범위한 사용으로 이 지역을 주도하고 있습니다. 유리한 보험 적용 정책과 병원 내 감염(HAI) 예방에 대한 강력한 강조는 이 지역의 지속적인 수요에 더욱 기여하고 있습니다.

의료용 장갑 시장의 주요 기업은 INTCO Medical, Medline Industries, Rubberex, Supermax, Globus, Hartalega, Semperit, Kossan, 3M Company, Top Glove, Cardinal Health, Ansell입니다.

의료용 장갑 업계의 선도 업체들은 시장 입지를 강화하기 위해 생산 능력 확대, 제품 혁신, 지역 다각화에 적극적으로 투자하고 있습니다. 여러 제조업체들은 인력 의존도를 감축하고 운영 효율성을 높이기 위해 자동화 생산 라인을 구축하고 있습니다. 전략적 파트너십, 합병 및 인수도 신규 시장 진출과 유통망 향상을 위해 활용되고 있습니다. 환경 문제에 대응하여 기업들은 생분해성 장갑 옵션을 개발하고 지속 가능한 조달 관행을 촉진하고 있습니다. 또한 많은 기업들은 경쟁이 심화되는 미래에서 수요 안정성을 확보하고 브랜드 충성도를 구축하기 위해 의료 기관과의 장기 공급 계약을 추진하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

업계에 미치는 영향요인

성장 촉진요인

안전과 위생에 관한 의식의 고조

전 세계적으로 수술 건수의 급속한 증가

개발도상국 내 의료 시설 수 증가

전염병 증가

업계의 잠재적 위험 및 과제

라텍스 장갑에 의한 감염의 가능성

경쟁 가격 압력

시장 기회

생분해성 의료용 장갑 개발

재택 케어와 원격 의료의 성장 통합

성장 가능성 분석

규제 상황

기술적 진보

현재 기술 동향

신흥 기술

나노기술의 통합

3D 프린팅 및 맞춤화 가능성

고급 장벽 보호 기술

디지털 헬스 통합 및 스마트 장갑

밸류체인 분석

환급 시나리오

소비자 행동의 경향

고무 수술용 장갑의 국가별 수출입(비율 및 금액)

국가별 수입 데이터(%, 2021-2023년)

국가별 수입 데이터(값, 2021-2023년)

국가별 수출 데이터(%, 2021-2023년)

국가별 수출 데이터(값, 2021-2023년)

가격 분석(2024년)

제품별

지역별

톱 기업의 판매 모델

브랜드 분석

공급망 최적화 전략

리스크 분산과 탄력성 구축

공급자 관계 관리

재고 관리 및 수요 예측

물류와 배송 최적화

투자 및 자금조달 동향

재료 기술의 진화

차세대 니트릴 제제

바이오 기반 및 지속 가능한 소재 개발

가속제 없는 기술적 발전

항균 및 항바이러스 코팅 기술

Porter's Five Forces 분석

PESTEL 분석

장래 시장 동향

갭 분석

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

세계

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병과 인수

파트너십 및 협업

신제품 발매

확장 계획

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

주요 동향

라텍스 장갑

니트릴 장갑

비닐 장갑

네오프렌 장갑

기타 제품 유형

제6장 시장 추계 및 예측 : 형태별(2021-2034년)

주요 동향

파우더 프리 장갑

파우더 처리 장갑

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

검사

수술

치과

식품 가공

클린룸

기타 용도

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

일회용 장갑

재사용 가능한 장갑

제9장 시장 추계 및 예측 : 불임증별(2021-2034년)

주요 동향

멸균 장갑

비멸균 장갑

제10장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

주요 동향

점포

전자상거래

제11장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

주요 동향

병원

클리닉

외래수술센터(ASC)

진단센터

기타 최종 사용자

제12장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

아시아태평양

일본

중국

인도

호주

한국

말레이시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제13장 기업 프로파일

세계 기업

3M Company

Ansell

Cardinal Health

Globus

Hartalega

INTCO Medical

Kossan

Medline Industries

Rubberex

Semperit

Supermax

Top Glove

지역 기업

Akzenta

Eco Medi Glove

Swear HealthCare

신흥 기업

Adventa Healthcare

Berner International

ERENLER MEDIKAL

Leboo Healthcare

NuLife

Vernacare

SHIELD Scientific

HBR

영문 목차

영문목차

The global medical gloves market was estimated at USD 4.5 billion in 2024 and is expected to grow from USD 5.2 billion in 2025 to USD 13.5 billion by 2034, at a CAGR of 11.2%, according to the latest report published by Global Market Insights Inc.

Hospitals, clinics, and diagnostic centers are prioritizing infection control protocols, driving consistent demand for disposable medical gloves to reduce the risk of cross-contamination between patients and healthcare workers.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$4.5 Billion

Forecast Value

$13.5 Billion

CAGR

11.2%

Rising Demand for the Nitrile Gloves Segment

The nitrile gloves segment has gained strong traction in 2024, driven by its superior chemical resistance, durability, and hypoallergenic properties. Unlike latex gloves, nitrile variants offer a safer alternative for both patients and healthcare workers with latex sensitivities. These gloves are increasingly preferred in surgical environments, emergency rooms, and diagnostic labs where strength and puncture resistance are critical. The segment continues to expand, supported by a shift in demand toward synthetic materials and rising awareness of occupational safety standards.

Powder-Free Gloves to Gain Traction

The powder-free gloves segment generated notable revenues in 2024 owing to regulatory restrictions and concerns over allergic reactions caused by glove powders. These gloves offer enhanced skin safety and reduce the risk of contamination during patient care and surgical procedures. Their increasing adoption is also driven by improved manufacturing techniques that ensure ease of donning without the need for powder. With regulatory agencies like the FDA banning powdered medical gloves, the powder-free segment has witnessed a substantial market shift. Manufacturers continue to innovate within this category by enhancing comfort, grip, and tactile sensitivity, making powder-free gloves a critical part of modern medical protocols.

Regional Insights

North America to Emerge as a Lucrative Region

North America medical gloves market held a notable share in 2024, driven by strong healthcare infrastructure, stringent safety regulations, and high awareness of infection control. The United States leads the region due to widespread use across hospitals, outpatient facilities, and diagnostic centers. Favorable reimbursement policies and a strong emphasis on hospital-acquired infection (HAI) prevention further contribute to sustained demand in this region.

Major players in the medical gloves market are INTCO Medical, Medline Industries, Rubberex, Supermax, Globus, Hartalega, Semperit, Kossan, 3M Company, Top Glove, Cardinal Health, and Ansell.

To strengthen their market foothold, leading players in the medical gloves industry are actively investing in capacity expansion, product innovation, and regional diversification. Several manufacturers are establishing automated production lines to reduce dependency on manual labor and improve operational efficiency. Strategic partnerships, mergers, and acquisitions are also being leveraged to access new markets and enhance distribution networks. In response to environmental concerns, companies are developing biodegradable glove options and promoting sustainable sourcing practices. Additionally, many firms are pursuing long-term supply contracts with healthcare institutions to secure demand consistency and build brand loyalty in an increasingly competitive landscape.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional trends

2.2.2 Product trends

2.2.3 Form trends

2.2.4 Application trends

2.2.5 Usage trends

2.2.6 Sterility trends

2.2.7 Distribution channel trends

2.2.8 End use trends

2.3 CXO perspectives: Strategic imperatives

2.3.1 Key decision points for industry executives

2.3.2 Critical success factors for market players

2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Growing awareness regarding safety and hygiene

3.2.1.2 Rapid growth in the number of surgeries across the globe

3.2.1.3 Increasing number of healthcare facilities in developing countries

3.2.1.4 Growing number of contagious diseases

3.2.2 Industry pitfalls and challenges

3.2.2.1 Possible infections due to latex gloves

3.2.2.2 Competitive pricing pressures

3.2.3 Market opportunities

3.2.3.1 Development of biodegradable medical gloves

3.2.3.2 Home healthcare and telemedicine growth integration

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East and Africa

3.5 Technological advancements

3.5.1 Current technological trends

3.5.2 Emerging technologies

3.5.2.1 Nanotechnology integration

3.5.2.2 3D printing and customization potential

3.5.2.3 Advanced barrier protection technologies

3.5.2.4 Digital health integration and smart gloves

3.6 Value chain analysis

3.7 Reimbursement scenario

3.8 Consumer behaviour trend

3.9 Import and export of rubber surgical gloves, by country (% and value)

3.9.1 Import data by country (%), 2021-2023

3.9.2 Import data by country (value), 2021-2023

3.9.3 Export data by country (%), 2021-2023

3.9.4 Export data by country (value), 2021-2023

3.10 Pricing analysis, 2024

3.10.1 By product

3.10.2 By region

3.11 Sales model of top companies

3.12 Brand analysis

3.13 Supply chain optimization strategies

3.13.1 Risk diversification and resilience building

3.13.2 Supplier relationship management

3.13.3 Inventory management and demand forecasting

3.13.4 Logistics and distribution optimization

3.14 Investment and funding trends

3.15 Material technology evolution

3.15.1 Next-generation nitrile formulations

3.15.2 Bio-based and sustainable material development

3.15.3 Accelerator-free technology advancement

3.15.4 Antimicrobial and antiviral coating technologies

3.16 Porter's analysis

3.17 PESTEL analysis

3.18 Future market trends

3.19 Gap analysis

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 Global

4.2.2 North America

4.2.3 Europe

4.2.4 Asia Pacific

4.2.5 Latin America

4.2.6 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers and acquisitions

4.6.2 Partnerships and collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn and Units)

5.1 Key trends

5.2 Latex gloves

5.3 Nitrile gloves

5.4 Vinyl gloves

5.5 Neoprene gloves

5.6 Other product types

Chapter 6 Market Estimates and Forecast, By Form, 2021 - 2034 ($ Mn and Units)

6.1 Key trends

6.2 Powder-free gloves

6.3 Powdered gloves

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn and Units)

7.1 Key trends

7.2 Examination

7.3 Surgical

7.4 Dental

7.5 Food processing

7.6 Cleanroom

7.7 Other applications

Chapter 8 Market Estimates and Forecast, By Usage, 2021 - 2034 ($ Mn and Units)

8.1 Key trends

8.2 Disposable gloves

8.3 Reusable gloves

Chapter 9 Market Estimates and Forecast, By Sterility, 2021 - 2034 ($ Mn and Units)

9.1 Key trends

9.2 Sterile gloves

9.3 Non-sterile gloves

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn and Units)

10.1 Key trends

10.2 Brick and mortar

10.3 E-commerce

Chapter 11 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn and Units)

11.1 Key trends

11.2 Hospitals

11.3 Clinics

11.4 Ambulatory surgical centers

11.5 Diagnostic centers

11.6 Other end users

Chapter 12 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn and Units)