Audiology Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1822613

리서치사:Global Market Insights Inc.

발행일:2025년 08월

페이지 정보:영문 165 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

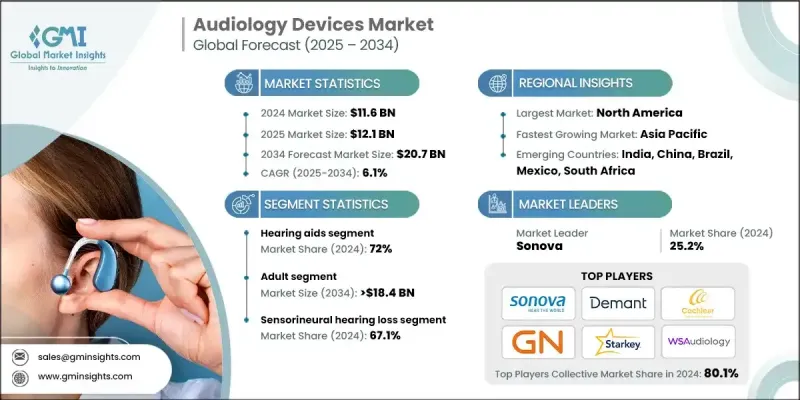

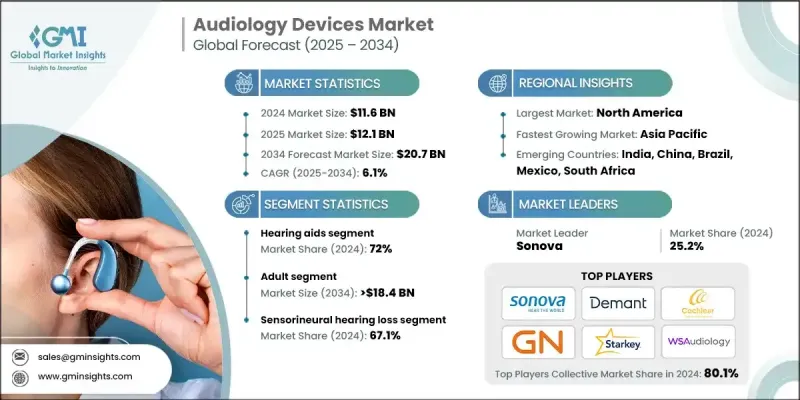

Global Market Insights Inc.가 발행한 최신 보고서에 따르면 청력 검사 기기 세계 시장은 2024년에 116억 달러로 평가되었고, CAGR 6.1%로 2025년 121억 달러, 2034년에는 207억 달러로 성장할 것으로 예측되고 있습니다.

세계적인 난청 이환율 증가는 청력 검사 기기 시장의 주요 촉진요인입니다. 평균 수명이 연장되고 세계 인구의 고령화가 진행됨에 따라 노안이라고도 불리는 노화로 인한 청각 장애가 점점 보편화되고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시장 규모

116억 달러

예측 금액

207억 달러

CAGR

6.1%

보청기 수요 증가

보청기 분야는 지속적인 기술 혁신과 눈에 띄지 않고 사용하기 쉬운 제품에 대한 수요가 증가함에 따라 2024년에 주목해야 할 점유율을 차지했습니다. 최근 보청기는 블루투스 연결, AI를 통한 음질 향상, 노이즈 제거, 충전식 배터리 등의 고급 기능을 갖추고 있습니다. 이러한 기능은 디지털 라이프 스타일과의 원활한 통합을 요구하는 기술에 익숙한 소비자에게 호소합니다.

성인층의 수요 증가

성인분야는 2024년 노화에 따른 청력 상실의 유병률이 높기 때문에 큰 수익을 올렸습니다. 더 많은 성인들이 능동적인 라이프스타일을 지원하는 솔루션을 찾는 가운데 자연스러운 음질과 긴 배터리 수명을 제공하는 고성능, 유지보수가 적은 장비에 대한 수요가 증가하고 있습니다. 또한 성인은 정기적인 청력 검사를 받는 경향이 높아 진단률과 치료율의 향상으로 이어집니다. 제조업체는 이 층을 타겟으로, 자립, 커뮤니케이션, 생활의 질을 강조한 마케팅을 실시했습니다.

감음성 난청의 유병률 증가

감음성 난청 분야는 2024년 지속 가능한 수익을 올렸습니다. 감음성 난청은 일반적으로 내이와 청신경 손상으로 인해 발생하며, 종종 회복 불가능하며 장기적인 장비 지원이 필요합니다. 보청기와 인공 내이가 주요 해결책이며 장비의 성능은 중증도에 따라 조정됩니다. 각 회사는 보다 자연스러운 소리를 모방하고 복잡한 소리 환경에 적응하는 기기를 개발하기 위해 연구 개발에 많은 투자를 하고 있습니다. 음성 인식 및 실시간 음성 처리의 혁신은 시끄러운 환경에서도 선명함과 편안함을 향상시키는 데 도움이 됩니다.

지역별 인사이트

북미가 추진력이 있는 지역으로 상승

북미 청력 검사 기기 시장은 고급 건강 관리 인프라, 유리한 상환 정책, 조기 난청 진단의 견고한 문화에 견인되어 2024 년에 큰 점유율을 차지했습니다. 미국은 고령화와 소비자 의식 증가에 힘입어 매년 30억 달러를 넘는 금액으로 꾸준히 성장하고 있으며 이 지역 시장을 독점하고 있습니다. 기업은 청각 클리닉 네트워크의 확장, 온라인 소매 플랫폼 강화, 청각 케어 여행에 대한 원격 의료 솔루션의 통합을 통해 북미의 입지를 강화하고 있습니다.

청력 검사 기기 시장의 주요 기업은 EARGO, Demant, NUROTRON, ENVOY MEDICAL, WS Audiology, Medtronic, GN Store Nord, MAICO, RION, EARTECHNIC, MED-EL Medical, Starkey, Cochlear, American Diagnostic Corporation, Sonova입니다.

청력 검사 기기 시장의 주요 기업은 그 존재감을 확고하게하기 위해 다방면에서 접근을 채택하고 있습니다. 혁신은 여전히 중심적이며 진화하는 사용자의 기대에 부응하기 위해 소형화, AI 기반 음성 처리 및 무선 연결에 대한 투자를 계속하고 있습니다. 많은 기업들은 원격 의료 제공업체와 소매 약국 체인과 전략적 제휴를 맺어 판매망을 넓히고 있습니다. 또한 맞춤형 피팅 기술, 기기 제어를 위한 모바일 앱, 평생 서비스 플랜을 통해 고객 경험이 우선합니다.

The global audiology devices market was estimated at USD 11.6 billion in 2024 and is expected to grow from USD 12.1 billion in 2025 to USD 20.7 billion by 2034, at a CAGR of 6.1%, according to the latest report published by Global Market Insights Inc.

The growing incidence of hearing loss worldwide is a primary driver of the audiology devices market. Age-related hearing impairment, also known as presbycusis, is becoming increasingly common as life expectancy rises and the global population continues to age.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$11.6 Billion

Forecast Value

$20.7 Billion

CAGR

6.1%

Rising Demand for Hearing Aids

The hearing aids segment held a notable share in 2024, driven by continuous technological innovation and rising demand for discreet, user-friendly products. Modern hearing aids now feature advanced functionalities such as Bluetooth connectivity, AI-based sound enhancement, noise cancellation, and rechargeable batteries. These features appeal to tech-savvy consumers looking for seamless integration with digital lifestyles.

Adults to Gain Traction

The adult segment generated significant revenues in 2024, owing to the high prevalence of age-related hearing loss. As more adults seek solutions that support active lifestyles, there is a growing demand for high-performance, low-maintenance devices that offer natural sound quality and long battery life. Adults are also more likely to engage in regular hearing assessments, leading to higher diagnosis and treatment rates. Manufacturers are targeting this demographic with marketing that emphasizes independence, communication, and quality of life.

Increasing Prevalence of Sensorineural Hearing Loss

The sensorineural hearing loss segment generated sustainable revenues in 2024. This condition, typically caused by damage to the inner ear or auditory nerve, is often irreversible and requires long-term device support. Hearing aids and cochlear implants are the primary solutions, with device performance tailored to different degrees of severity. Companies are investing heavily in research and development to produce devices that better mimic natural hearing and adapt to complex sound environments. Innovations in speech recognition and real-time sound processing are helping users experience improved clarity and comfort in noisy settings.

Regional Insights

North America to Emerge as a Propelling Region

North America audiology devices market held a sizeable share in 2024, driven by advanced healthcare infrastructure, favorable reimbursement policies, and a strong culture of early hearing loss diagnosis. The United States dominates the regional market, with a value exceeding USD 3 billion and steady annual growth fueled by the aging population and rising consumer awareness. Companies are strengthening their position in North America by expanding audiology clinic networks, enhancing online retail platforms, and integrating telehealth solutions into the hearing care journey.

Major players in the audiology devices market are EARGO, Demant, NUROTRON, ENVOY MEDICAL, WS Audiology, Medtronic, GN Store Nord, MAICO, RION, EARTECHNIC, MED-EL Medical, Starkey, Cochlear, American Diagnostic Corporation, and Sonova.

To solidify their presence, leading companies in the audiology devices market are adopting a multi-pronged approach. Innovation remains central, with ongoing investments in miniaturization, AI-based audio processing, and wireless connectivity to meet evolving user expectations. Many companies are entering strategic alliances with telehealth providers and retail pharmacy chains to broaden their distribution footprint. Additionally, customer experience is prioritized through personalized fitting technology, mobile apps for device control, and lifetime service plans.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definitions

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional trends

2.2.2 Product trends

2.2.3 Patient trends

2.2.4 Hearing loss trends

2.3 CXO perspectives: Strategic imperatives

2.3.1 Key decision points for industry executives

2.3.2 Critical success factors for market players

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Increasing prevalence of hearing loss globally

3.2.1.2 Growing preference for e-commerce channels

3.2.1.3 Technological advancements in audiology devices

3.2.1.4 Favorable reimbursement policies in developed countries

3.2.2 Industry pitfalls and challenges

3.2.2.1 High cost of advanced audiology devices

3.2.2.2 Lack of awareness in low-income countries

3.2.3 Market opportunities

3.2.3.1 Integration of AI and machine learning in hearing devices

3.2.3.2 Growing demand for tele-audiology and remote hearing services

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 U.S.

3.4.2 Europe

3.5 Technology landscape

3.6 Reimbursement scenario

3.7 Pricing analysis, by region

3.8 Consumer pathway

3.8.1 Conventional pathway

3.8.2 Need for new pathway

3.8.3 Hybrid pathway

3.9 Consumer insights

3.10 Policy landscape

3.11 Gap analysis

3.12 Risk management analysis

3.12.1 Research and development

3.12.2 Operations

3.12.3 Marketing and sales

3.12.4 Quality

3.12.5 Intellectual property rights

3.12.6 Regulatory

3.12.7 Information technology

3.12.8 Climate

3.12.9 Financial

3.13 Porter's analysis

3.14 PESTEL analysis

3.15 Future market trends

3.16 Value chain analysis

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company matrix analysis

4.3 Company market share analysis

4.3.1 By region

4.3.1.1 North America

4.3.1.2 Europe

4.3.1.3 Asia Pacific

4.3.1.4 Latin America

4.3.1.5 MEA

4.4 Competitive positioning matrix

4.5 Key developments

4.5.1 Mergers and acquisitions

4.5.2 Partnerships and collaborations

4.5.3 New product launches

4.5.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn, Units)

5.1 Key trends

5.2 Hearing aids

5.2.1 By Type

5.2.1.1 Behind-the-ear (BTE)

5.2.1.2 Receiver in the ear/receiver in canal (RITE/RIC)