Marine Sensors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1822590

리서치사:Global Market Insights Inc.

발행일:2025년 08월

페이지 정보:영문 185 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

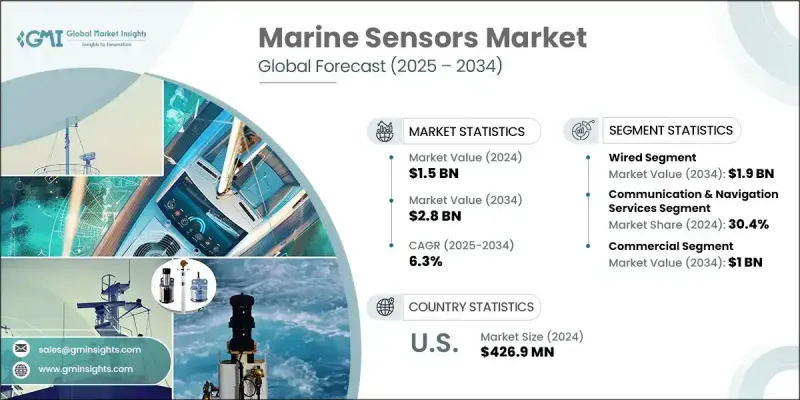

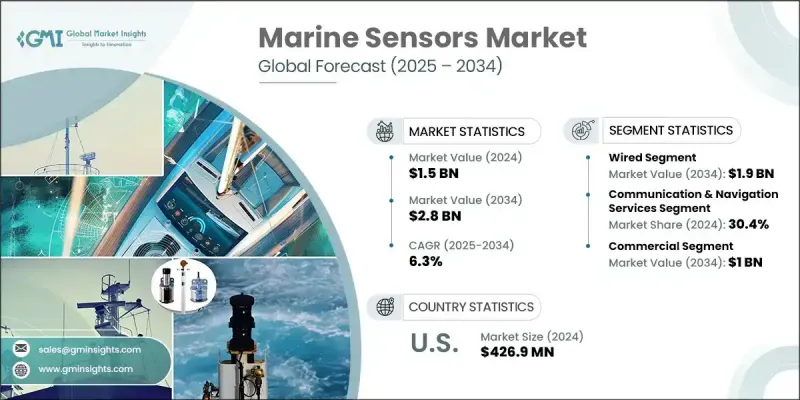

해양 센서 세계 시장 규모는 2024년에는 15억 달러에 달했고, CAGR 6.3%로 성장했으며 2034년에는 28억 달러에 이를 것으로 예측됩니다.

이 성장을 뒷받침하는 주요 요인은 해저 모니터링 인프라 설치, 항만 시설의 현대화, 세계 해상 무역 증가 등입니다. 해상 루트가 세계적인 물류를 지배하고 있기 때문에 고급 감지 시스템에 대한 수요가 가속화되고 있습니다. 이러한 기술은 항만 항해, 하역, 선박 교통 관리 등의 업무 성능을 향상시키고 있습니다. 이에 대응하기 위해, 제조업체 각 사는 다기능으로 컴팩트한 센서를 설계해, 특히 자율형 시스템이나 소형 선박에의 유연한 배치를 가능하게 하고 있습니다. 광섬유 기반의 센싱과 같은 기술 혁신은 정확성과 과제인 수중 환경에서의 내구성으로 지지를 받고 있습니다. 또한 재활용 가능한 구성요소, 최소한의 에너지 사용, 환경에 배려한 배치 방법 등 지속 가능한 설계를 중시하는 움직임도 눈에 띄고 있으며, 상업·방위 양 분야에서의 가치 제안이 더욱 강화되고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시장 규모

15억 달러

예측 금액

28억 달러

CAGR

6.3%

유선 해양 센서는 2034년까지 19억 달러를 창출할 것으로 예상되며, 일관된 데이터 전달과 가혹한 해양 환경에서의 견고성으로 인해 관련성을 유지하고 있습니다. 그 신뢰성은 항만과 해양 에너지 시설과 같은 고정된 장소에 장기 배치에 이상적입니다. 현장에서의 성능 수명과 비용 효율을 높이기 위해 내부식성 강화를 위한 지속적인 조사가 이루어지고 있습니다. 이러한 유선 시스템의 내구성과 정확성은 여전히 비교할 수 없으며 전 세계 해양 인프라의 핵심에 필수적입니다.

통신 및 내비게이션 분야는 2024년에 30.4%의 점유율을 차지했습니다. 이 분야에서는 해상 상황 인식과 안전 프로토콜을 최적화하는 기술의 통합이 진행되고 있습니다. 최신 시스템은 다양한 센서의 출력을 통합 운영 이미지에 통합하고 네비게이션, 항로 최적화 및 충돌 방지를 위한 실시간 의사결정을 강화하도록 설계되었습니다. 세계적으로 해상 교통량이 증가하고 있기 때문에 이러한 시스템의 수용과 도입이 진행되고 있으며, 민간 선박과 방위 항행 노력 모두에 중요한 데이터를 제공합니다.

북미 해양 센서 시장은 2024년에 31.6%의 점유율을 차지하며 2034년까지 연평균 복합 성장률(CAGR)은 5.8%를 보일 것으로 예측됩니다. 이 지역 전체 시장 확대는 해상 안전 인프라, 해양 재생에너지 및 고도 환경 모니터링 시스템에 대한 투자 확대로 지원됩니다. 스마트 센서 기술의 채택은 이 지역의 항만 자동화, 선박 추적, 상업 및 방어 용도에 걸친 컴플라이언스 관리 능력을 강화하고 있습니다. 북미 기업은 이러한 진화 상황에서 경쟁력을 유지하기 위해 차세대 센서 기술을 채택하고 있으며, 혁신은 여전히 중요한 주제입니다.

해양 센서 시장을 형성하는 주요 기업으로는 Honeywell, Kongsberg Maritime, Garmin, Eaton, Curtiss-Wright, Nortek, Furuno, NKE Marine Electronics 등이 있습니다. 이러한 주요 기업들은 이 분야의 개발과 혁신을 주도하고 현대적인 해양 생태계의 복잡한 요구에 부응하는 최첨단 센서 기술을 제공합니다. 시장에서의 지위를 굳히기 위해, 주요 해양 센서 기업은 센서의 정밀도, 내구성, 통합 능력을 높이는 연구 개발에 다액의 투자를 실시했습니다. 각 회사는 자율 선박과 소형 플랫폼에 원활하게 배치 할 수 있도록 소형화 및 다기능 시스템에 주력하고 있습니다. 또 다른 주요 전략은 재활용 가능한 재료와 에너지 효율적인 부품을 사용하고 지속 가능한 운영을 지원하는 센서를 개발하는 것입니다. 방위기관과 상업선박사와의 파트너십은 용도의 범위를 확대하고 광섬유 기술의 지속적인 업그레이드는 가혹한 조건에서 성능을 유지하는 데 도움이 됩니다.

목차

제1장 조사 방법

시장의 범위와 정의

조사 디자인

조사 접근

데이터 수집 방법

데이터 마이닝 소스

세계

지역/국가

기본 추정과 계산

기준연도 계산

시장 예측의 주요 동향

1차 조사와 검증

1차 정보

예측 모델

조사의 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

세계 해상무역 확대와 항만 근대화

해군의 수중 감시 시스템의 배치 증가

엄격한 해상 안전 및 환경 규제

자율형 및 무인 선박의 도입 증가

실시간 내비게이션 및 모니터링 시스템에 대한 수요 증가

업계의 잠재적 위험 및 과제

첨단 센서 시스템의 설치 및 유지 보수 비용이 증가

수중에서의 운용 범위의 제한과 환경의 제약

시장 기회

예측적인 해양 분석을 위한 AI와 머신러닝의 통합

풍력 발전소를 포함한 해상 재생에너지 프로젝트 확대

해상 운영에서 디지털 트윈 기술의 채택 증가

해양 보전 프로젝트에 있어서의 관민 제휴의 강화

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현재의 기술 동향

신규기술

새로운 비즈니스 모델

컴플라이언스 요건

국방예산 분석

세계의 방위비의 동향

지역 방위 예산 배분

북미

유럽

아시아태평양

중동 및 아프리카

라틴아메리카

주요 방위 근대화 프로그램

예산 예측(2025-2034)

업계의 성장에 미치는 영향

국가별 방위 예산

공급 체인의 탄력

지정학적 분석

인재 분석

디지털 변혁

합병, 인수, 전략적 파트너십의 상황

위험 평가 및 관리

주요 계약 체결(2021-2024)

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 기업의 경쟁 벤치마킹

재무실적의 비교

수익

이익률

연구개발

제품 포트폴리오 비교

제품 범위 폭

기술

혁신

지리적 존재의 비교

세계 실적 분석

서비스 네트워크의 범위

지역별 시장 침투율

경쟁 포지셔닝 매트릭스

리더들

도전자

팔로워

틈새 기업

전략적 전망 매트릭스

주요 발전, 2021-2024

합병과 인수

파트너십 및 협업

기술적 진보

확대 및 투자 전략

디지털 변혁의 대처

신규기업/스타트업기업경쟁 구도

제5장 시장 추정 및 예측 : 센서 유형별, 2021-2034

주요 동향

압력 센서

온도 센서

힘 센서

토크 센서

속도 센서

위치·변위 센서

레벨 센서

근접 센서

플로우 센서

광학 센서

모션 센서

레이더 센서

연기 감지 센서

GPS 센서

음향 센서

전류 센서

기타

제6장 시장 추정 및 예측 : 접속성별, 2021-2034

주요 동향

유선

무선

제7장 시장 추정 및 예측 : 용도별, 2021-2034

주요 동향

정보 수집, 감시, 정찰

통신 및 내비게이션 서비스

환경 모니터링

HVAC 시스템

연료 및 추진 시스템

기타

제8장 시장 추정 및 예측 : 최종 용도별, 2021-2034

주요 동향

상업용

크루즈선

여객 페리

요트

유조선

벌크선

화물선

기타

군 및 방위

항공모함

양륙함

프리게이트함

구축함

잠수함

기타

무인 수중 차량

자율형 수중 차량

원격조작형 수중차량

기타

제9장 시장 추정 및 예측 : 지역별, 2021-2034

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

네덜란드

아시아태평양

중국

인도

일본

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제10장 기업 프로파일

세계 주요 기업

Kongsberg Maritime

Teledyne Marine

Thales

Garmin

Furuno

지역별 주요 기업

북미

Honeywell

Northrop Grumman

Curtiss-Wright

Rockwell Collins

유럽

Eaton

Sonardyne

SBG Systems

Trensor

아시아태평양

NKE Marine Electronics

Nortek

Senmatic

틈새 기업/디스 랩터

Sea-Bird Scientific

Siren Marine

TE Connectivity

Xylem

SHW

영문 목차

영문목차

The Global Marine Sensors Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 6.3% to reach USD 2.8 billion by 2034.

Key drivers fueling this growth include the installation of submarine surveillance infrastructure, the modernization of port facilities, and rising global maritime trade. As sea routes continue to dominate global logistics, the demand for advanced sensing systems has accelerated. These technologies are improving operational performance across port navigation, cargo handling, and vessel traffic management. In response, manufacturers are engineering multi-functional, compact sensors that allow for flexible deployment, particularly on autonomous systems and compact marine vessels. Technological innovations, such as fiber-optic-based sensing, are gaining traction due to their accuracy and durability in challenging underwater environments. There is also a notable pivot toward sustainable design, emphasizing recyclable components, minimal energy usage, and eco-conscious deployment methods-further enhancing their value proposition in both commercial and defense sectors.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$1.5 Billion

Forecast Value

$2.8 Billion

CAGR

6.3%

The wired marine sensors are projected to generate USD 1.9 billion by 2034, maintaining their relevance due to consistent data delivery and robustness in harsh marine environments. Their reliability makes them ideal for long-term deployments in fixed locations such as harbors and offshore energy installations. Continued research is being channeled into enhancing their anti-corrosive properties to boost performance longevity and cost-efficiency in the field. The durability and precision of these wired systems remain unmatched, making them essential to the backbone of marine infrastructure across the globe.

The communication and navigation segment held a 30.4% share in 2024. This segment has witnessed increased integration of technologies that optimize maritime situational awareness and safety protocols. Modern systems are designed to merge various sensor outputs into a unified operational picture, enhancing real-time decision-making for navigation, route optimization, and collision prevention. The growing volume of maritime traffic globally is driving the acceptance and deployment of such systems, which provide critical data for both commercial shipping and defense navigation efforts.

North America Marine Sensors Market held a 31.6% share in 2024 and is projected to grow at a CAGR of 5.8% through 2034. Market expansion across the region is being supported by growing investments in maritime safety infrastructure, offshore renewable energy, and advanced environmental monitoring systems. Adoption of smart sensor technologies is enhancing the region's capabilities in port automation, vessel tracking, and compliance management across commercial and defense applications. Innovation remains a key theme as North American companies continue to adopt next-gen sensor technologies to remain competitive in this evolving landscape.

Key players shaping the Marine Sensors Market include Honeywell, Kongsberg Maritime, Garmin, Eaton, Curtiss-Wright, Nortek, Furuno, and NKE Marine Electronics. These companies are leading developments and innovation in the field, delivering cutting-edge sensor technologies that meet the complex needs of the modern maritime ecosystem. To solidify their market position, leading marine sensor companies are investing heavily in R&D to enhance sensor precision, durability, and integration capabilities. Firms are focusing on miniaturization and multifunctional systems to enable seamless deployment on autonomous vessels and compact platforms. Another key strategy involves developing sensors that support sustainable operations, using recyclable materials and energy-efficient components. Partnerships with defense organizations and commercial shipping entities are expanding application reach, while continuous upgrades to fiber-optic technology help maintain performance in extreme conditions.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Sensor type trends

2.2.2 Connectivity trends

2.2.3 Application trends

2.2.4 End use trends

2.2.5 Regional trends

2.3 TAM analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Expansion of global maritime trade and port modernization

3.2.1.2 Increasing deployment of naval underwater surveillance systems

3.2.1.3 Stringent maritime safety and environmental regulations

3.2.1.4 Rising adoption of autonomous and unmanned marine vessels

3.2.1.5 Increasing demand for real-time navigation and monitoring systems

3.2.2 Industry pitfalls and challenges

3.2.2.1 High installation and maintenance costs of advanced sensor systems

3.2.2.2 Limited operational range and environmental constraints underwater

3.2.3 Market opportunities

3.2.3.1 Integration of AI and machine learning for predictive marine analytics

3.2.3.2 Expansion of offshore renewable energy projects, including wind farms

3.2.3.3 Growing adoption of digital twin technology in maritime operations

3.2.3.4 Increasing public-private partnerships for marine conservation projects

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Technology and Innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Emerging business models

3.9 Compliance requirements

3.10 Defense budget analysis

3.11 Global defense spending trends

3.12 Regional defense budget allocation

3.12.1 North America

3.12.2 Europe

3.12.3 Asia Pacific

3.12.4 Middle East and Africa

3.12.5 Latin America

3.13 Key defense modernization programs

3.14 Budget forecast (2025-2034)

3.14.1 Impact on industry growth

3.14.2 Defense budgets by country

3.15 Supply chain resilience

3.16 Geopolitical analysis

3.17 Workforce analysis

3.18 Digital transformation

3.19 Mergers, acquisitions, and strategic partnerships landscape

3.20 Risk assessment and management

3.21 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 Latin America

4.2.1.5 Middle East & Africa

4.3 Competitive benchmarking of key players

4.3.1 Financial performance comparison

4.3.1.1 Revenue

4.3.1.2 Profit margin

4.3.1.3 R&D

4.3.2 Product portfolio comparison

4.3.2.1 Product range breadth

4.3.2.2 Technology

4.3.2.3 Innovation

4.3.3 Geographic presence comparison

4.3.3.1 Global footprint analysis

4.3.3.2 Service network coverage

4.3.3.3 Market penetration by region

4.3.4 Competitive positioning matrix

4.3.4.1 Leaders

4.3.4.2 Challengers

4.3.4.3 Followers

4.3.4.4 Niche players

4.3.5 Strategic outlook matrix

4.4 Key developments, 2021-2024

4.4.1 Mergers and acquisitions

4.4.2 Partnerships and collaborations

4.4.3 Technological advancements

4.4.4 Expansion and investment strategies

4.4.5 Digital transformation initiatives

4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Sensor Type, 2021 - 2034 (USD Million & Thousand Units)

5.1 Key trends

5.2 Pressure sensors

5.3 Temperature sensors

5.4 Force sensors

5.5 Torque sensors

5.6 Speed sensors

5.7 Position & displacement sensors

5.8 Level sensors

5.9 Proximity sensors

5.10 Flow sensors

5.11 Optical sensors

5.12 Motion sensors

5.13 Radar sensors

5.14 Smoke detection sensors

5.15 GPS sensors

5.16 Acoustic sensors

5.17 Current sensors

5.18 Others

Chapter 6 Market Estimates and Forecast, By Connectivity, 2021 - 2034 (USD Million & Thousand Units)

6.1 Key trends

6.2 Wired

6.3 Wireless

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million & Thousand Units)

7.1 Key trends

7.2 Intelligence, surveillance & reconnaissance

7.3 Communication & navigation services

7.4 Environmental monitoring

7.5 HVAC system

7.6 Fuel & propulsion system

7.7 Others

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million & Thousand Units)

8.1 Key trends

8.2 Commercial

8.2.1 Cruise ship

8.2.2 Passenger ferries

8.2.3 Yachts

8.2.4 Tankers

8.2.5 Bulk carriers

8.2.6 Cargo ships

8.2.7 Others

8.3 Military & defense

8.3.1 Aircraft carriers

8.3.2 Amphibious ships

8.3.3 Frigates

8.3.4 Destroyers

8.3.5 Submarines

8.3.6 Others

8.4 Unmanned underwater vehicles

8.4.1 Autonomous underwater vehicles

8.4.2 Remotely operated underwater vehicles

8.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million & Thousand Units)