광전자증배관(PMT) 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Photomultiplier Tube (PMT) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1822584

리서치사:Global Market Insights Inc.

발행일:2025년 08월

페이지 정보:영문 180 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

광전자증배관(PMT) 세계 시장은 2024년에 5억 6,980만 달러로 평가되었고, CAGR 6.8%로 성장하여 2034년에는 10억 7,000만 달러에 이를 것으로 예측되고 있습니다.

광전자증배관은 매우 미약한 빛을 감지하는데 도움이 되며, 양전자 방사선 단층촬영(PET) 및 감마 카메라와 같은 의료 이미징 기술에 필수적입니다. 질병의 조기 진단과 정밀 이미징에 대한 세계적인 수요의 확대가 건강 관리에서 광전자증배관의 채택을 크게 뒷받침하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시장 규모

5억 6,980만 달러

예측 금액

10억 7,000만 달러

CAGR

6.8%

싱글 채널 PMT가 견인 역할

단일 입력 소스로부터 높은 정밀도, 저잡음 신호 감지로 단일 채널 PMT 부문이 2024년에 주목해야 할 점유율을 차지했습니다. 이러한 PMT는 소형화, 고속 응답 시간, 신뢰성이 중요한 실험 연구, 의료 이미징, 분석 장비에 널리 사용됩니다. 다중 채널 PMT의 상승에도 불구하고, 단일 채널 PMT는 단순성, 낮은 집적 비용 및 제어된 환경에서 입증된 성능으로 인해 지위를 유지하고 있습니다.

넓은 스펙트럼 감도에서의 채택 증가

2024년에는 자외(UV)에서 가시, 근적외(NIR)까지의 넓은 파장 범위에서 동작하는 광검출기에 의해 광 스펙트럼 감도 부문이 큰 점유율을 차지합니다. 광파장 영역을 수용하도록 설계된 PMT는 형광 분광, 천문학 및 환경 감지에 특히 유용하며, 멀티밴드 검출은 신호 명확성과 데이터 정확도를 크게 향상시킵니다.

온도 내성 PMT 수요 증가

내온도 PMT분야는 엄격한 산업환경, 항공우주, 과학적인 필드워크에 힘입어 2024년 지속적인 점유율을 유지했습니다. 이 부문의 PMT는 큰 온도 변동이나 고온 환경에 노출되어도 안정적인 이득과 낮은 노이즈를 유지할 수 있도록 설계되었습니다. 이 신뢰성은 원자력 연구 및 심우주 관측과 같은 미션 크리티컬 용도에서 안정적인 성능을 보장합니다.

지역별 인사이트

유리한 지역으로 상승하는 북미

북미의 광전자증배관(PMT) 시장은 고수준의 연구개발비, 견조한 방위부문, 고도의 헬스케어 인프라에 힘입어 2024년에 강력한 성장을 유지했습니다. 핵의학, 국토 안보, 우주 개발, 생명 과학 연구 등의 용도가 정부 연구 기관, 대학, 민간 기관의 광전자증배관 통합을 뒷받침하고 있습니다. 성숙한 기술 기반과 선도적 인 제조 업체 및 시스템 통합 업체의 강력한 존재로 이 지역은 고감도 포토닉스 기술에 대한 꾸준한 투자를 목표로하고 있습니다.

이 광전자증배관(PMT) 시장에 진입하고 있는 주요 기업은 Photok Ltd, Ametek Inc, Exosens, Thorlabs, Inc, Jeol Ltd, Et Enterprises, Ltd, Newport Corporation, Hamamats Photonics, First Sensor AG, Excelitas Technologies Corp, Broadcom, Laser Components, On Lux

광전자증배관(PMT) 시장의 각 사는 자사의 포지션을 강화하기 위해 재료의 혁신, 시스템 통합, 시장의 다양화를 조합한 대처에 주력하고 있습니다. 많은 기업들이 새로운 광전면 기술에 투자하고 더 넓은 스펙트럼 영역에서 감도를 높이는 동시에 노이즈와 전력 소비를 줄이고 있습니다. OEM 및 연구 기관과의 전략적 제휴는 일반적으로 의료 진단, 고에너지 물리학, 항공우주 등 차세대 용도를 위한 맞춤형 PMT 솔루션의 공동 개발을 가능하게 합니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

의료 영상 진단에서 수요 증가

고에너지·원자핵 물리학 조사의 확대

분석기기 및 산업기기의 진보

환경·방사선 모니터링 용도의 급증

우주항공 용도의 출현

업계의 잠재적 위험 및 과제

고체 대체품으로부터의 경쟁의 격화

높은 생산 비용과 운영 비용

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현재의 기술 동향

신규기술

가격 동향

지역별

제품별

가격 전략

새로운 비즈니스 모델

컴플라이언스 요건

소비자 감정 분석

특허 및 지적재산 분석

지정학과 무역의 역학

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

시장 집중 분석

주요 기업의 경쟁 벤치마킹

재무실적의 비교

수익

이익률

연구개발

제품 포트폴리오 비교

제품 라인업의 넓이

기술

혁신

지리적 존재의 비교

세계 실적 분석

서비스 네트워크의 범위

지역별 시장 침투율

경쟁 포지셔닝 매트릭스

리더들

도전자

팔로워

틈새 기업

전략적 전망 매트릭스

주요 발전, 2021-2024

합병과 인수

파트너십 및 협업

기술적 진보

확대 및 투자 전략

디지털 변혁 이니셔티브

신규기업/스타트업기업경쟁 구도

제5장 시장 추정 및 예측 : 유형별, 2021-2034

주요 동향

싱글 채널 PMT

멀티 채널 PMT(멀티 애노드 PMT)

마이크로채널 플레이트 PMT(MCP-PMT)

선형 어레이 PMT

기타

제6장 시장 추정 및 예측 : 파장 범위별, 2021-2034

주요 동향

자외선 검출

가시광 검출

적외선 검출

광범위한 감도

제7장 시장 추정 및 예측 : 최종 이용 산업별, 2021-2034

주요 동향

헬스케어 및 생명과학

연구기관

공업 및 제조업

국방·국토 안보

기타

제8장 시장 추정 및 예측 : 지역별, 2021-2034

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

네덜란드

아시아태평양

중국

인도

일본

한국

호주

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제9장 기업 프로파일

Ametek Inc

Broadcom

Caen SPA

Et Enterprises, Ltd.

Excelitas Technologies Corp.

Exosens

First Sensor AG

Hamamatsu Photonics

Jeol Ltd.

Laser Components

Luxium Solutions

Newport Corporation

ON Semiconductor

Photek Ltd

Thorlabs, Inc.

SHW

영문 목차

영문목차

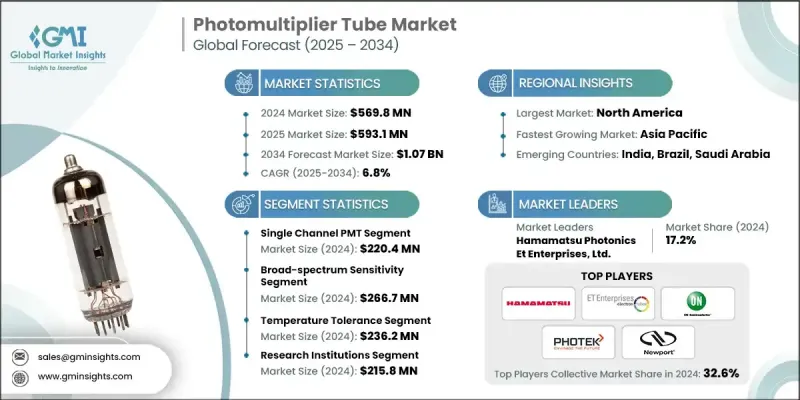

The Global Photomultiplier Tube Market was valued at USD 569.8 million in 2024 and is estimated to grow at a CAGR of 6.8% to reach USD 1.07 billion by 2034.

The photomultiplier tube helps in detecting extremely low levels of light, making them essential in medical imaging technologies such as positron emission tomography (PET) and gamma cameras. The expanding global demand for early disease diagnosis and precision imaging is significantly boosting PMT adoption in healthcare.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$569.8 Million

Forecast Value

$1.07 Billion

CAGR

6.8%

Single Channel PMT to Gain Traction

The single channel PMT segment held notable share in 2024, driven by high precision, low-noise signal detection from a single input source. These PMTs are widely used in laboratory research, medical imaging, and analytical instrumentation where compact size, fast response time, and reliability are critical. Despite the rise of multi-channel alternatives, single channel PMTs continue to hold their ground due to their simplicity, lower integration cost, and proven performance in controlled environments.

Rising Adoption in Broad Spectrum Sensitivity

The broad-spectrum sensitivity segment held substantial share in 2024 driven by photodetectors that can operate across wide wavelength ranges, from ultraviolet (UV) through visible to near infrared (NIR). PMTs designed for broad spectral responsiveness are particularly valuable in fluorescence spectroscopy, astronomy, and environmental sensing, where multi-band detection can significantly improve signal clarity and data accuracy.

Rising demand in Temperature Tolerance PMT

The temperature tolerance segment held sustainable share in 2024 backed by rugged industrial settings, aerospace, and scientific fieldwork. PMTs in this segment are engineered to maintain stable gain and low noise even when exposed to wide temperature fluctuations or elevated thermal environments. This reliability ensures consistent performance in mission-critical applications, such as nuclear research or deep-space observation.

Regional Insights

North America to Emerge as a Lucrative Region

North America photomultiplier tube market held robust growth in 2024 supported by high levels of R&D spending, a robust defense sector, and advanced healthcare infrastructure. Applications in nuclear medicine, homeland security, space exploration, and life sciences research continue to drive PMT integration across government labs, universities, and private institutions. With a mature technology base and strong presence of leading manufacturers and system integrators, the region witnesses steady investment in high-sensitivity photonics technologies.

Major players involved in the photomultiplier tube (PMT) market are Photek Ltd, Ametek Inc, Exosens, Thorlabs, Inc., Jeol Ltd., Et Enterprises, Ltd., Newport Corporation, Hamamatsu Photonics, First Sensor AG, Excelitas Technologies Corp., Broadcom, Laser Components, ON Semiconductor, Luxium Solutions, Caen S.P.A.

To strengthen their position, companies in the photomultiplier tube (PMT) market are focusing on a mix of material innovation, system integration, and market diversification. Many are investing in new photocathode technologies to enhance sensitivity across broader spectral ranges while simultaneously reducing noise and power consumption. Strategic collaborations with OEMs and research institutions are common, allowing companies to co-develop custom PMT solutions for next-generation applications in medical diagnostics, high-energy physics, and aerospace.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Component trends

2.2.2 Training type trends

2.2.3 Training device trends

2.2.4 Platform type trends

2.2.5 end use trends

2.2.6 Regional trends

2.3 TAM Analysis, 2025-2034 (USD Billion)

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising Demand in Medical Imaging and Diagnostics

3.2.1.2 Expansion of High-Energy and Nuclear Physics Research

3.2.1.3 Advancements in Analytical and Industrial Instruments

3.2.1.4 Surging Environmental and Radiation Monitoring Applications

3.2.1.5 Emergence of Space and Aerospace Applications

3.2.2 Industry pitfalls and challenges

3.2.2.1 Rising Competition from Solid-State Alternatives

3.2.2.2 High Production and Operational Costs

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Technology and innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Price trends

3.8.1 By region

3.8.2 By product

3.9 Pricing strategies

3.10 Emerging business models

3.11 Compliance requirements

3.12 Consumer sentiment analysis

3.13 Patent and IP analysis

3.14 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 Latin America

4.2.1.5 MEA

4.2.2 Market concentration analysis

4.3 Competitive benchmarking of key players

4.3.1 Financial performance comparison

4.3.1.1 Revenue

4.3.1.2 Profit margin

4.3.1.3 R&D

4.3.2 Product portfolio comparison

4.3.2.1 Product range breadth

4.3.2.2 Technology

4.3.2.3 Innovation

4.3.3 Geographic presence comparison

4.3.3.1 Global footprint analysis

4.3.3.2 Service network coverage

4.3.3.3 Market penetration by region

4.3.4 Competitive positioning matrix

4.3.4.1 Leaders

4.3.4.2 Challengers

4.3.4.3 Followers

4.3.4.4 Niche players

4.3.5 Strategic outlook matrix

4.4 Key developments, 2021-2024

4.4.1 Mergers and acquisitions

4.4.2 Partnerships and collaborations

4.4.3 Technological advancements

4.4.4 Expansion and investment strategies

4.4.5 Digital Transformation Initiatives

4.5 Emerging/ Startup Competitors Landscape

Chapter 5 Market estimates and forecast, by Type, 2021 - 2034 (USD million)

5.1 Key trends

5.2 Single Channel PMTs

5.3 Multi-Channel PMTs (Multi-Anode PMTs)

5.4 Microchannel Plate PMTs (MCP-PMTs)

5.5 Linear Array PMTs

5.6 Others

Chapter 6 Market estimates and forecast, by Wavelength Range, 2021 - 2034 (USD million)

6.1 Key trends

6.2 Ultraviolet Detection

6.3 Visible Light Detection

6.4 Infrared Detection

6.5 Broad-spectrum Sensitivity

Chapter 7 Market estimates and forecast, by End Use Industry, 2021 - 2034 (USD million)