자동차 블록체인 기술 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Automotive Blockchain Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1822542

리서치사:Global Market Insights Inc.

발행일:2025년 08월

페이지 정보:영문 230 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

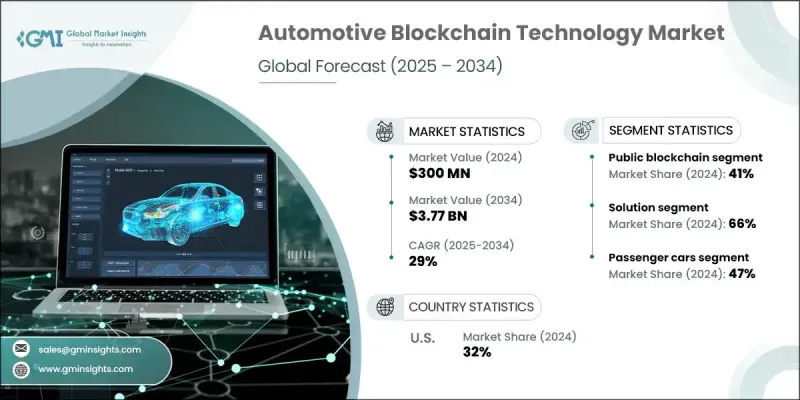

자동차 블록체인 기술 세계 시장 규모는 2024년에 3억 달러에 달했고, CAGR 29%로 성장했으며 2034년에는 37억 7,000만 달러에 이를 것으로 예측되고 있습니다.

자동차 연결과 소프트웨어 구동이 진행됨에 따라 자동차 제조업체는 데이터 무결성, 사이버 보안 및 실시간 통신에 대한 우려가 커지고 있습니다. 블록체인은 제조 및 부품 조달부터 소프트웨어 업데이트 및 소유권 이전에 이르기까지 자동차 라이프사이클 전반에 걸쳐 데이터를 안전하게 추적 및 검증하기 위한 분산형 변조 방지 시스템을 제공합니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시장 규모

3억 달러

예측 금액

37억 7,000만 달러

CAGR

29%

퍼블릭 블록체인의 보급 확대

퍼블릭 블록체인 분야는 탁월한 투명성과 분산형 구조로 2034년까지 강력한 견인력을 획득할 것으로 예측됩니다. 퍼블릭 블록체인은 자동차 제조업체, 규제 당국, 공급업체 및 최종 사용자를 포함한 여러 이해관계자가 중앙 기관에 의존하지 않고 실시간으로 데이터에 액세스하고 검증할 수 있도록 합니다. 이 모델은 차량의 기록 추적, 소유 기록 및 공유 모빌리티 용도에 특히 유용합니다.

솔루션 채택 증가

자동차 블록체인 기술 시장의 솔루션 분야는 2024년에 큰 점유율을 차지했습니다. 자동차 제조업체와 차량 운행사는 스마트 계약 실행부터 공급망 관리, 데이터 인증에 이르기까지 일련의 서비스를 제공하는 엔드 투 엔드 블록체인 플랫폼에 대한 투자를 늘리고 있습니다. 이러한 솔루션은 운영 오버헤드를 줄이고 투명성을 높이고 기업이 디지털 인프라를 미래에 유지할 수 있도록 도와줍니다.

견인역이 되는 승용차

승용차 부문은 최신 자동차에 디지털 기술이 급속히 통합되어 있기 때문에 2024년에는 큰 점유율을 차지합니다. 소비자가 보다 똑똑하고 안전하며 연결성이 높은 운전 경험을 추구하는 동안 자동차 제조업체는 블록체인을 활용하여 OTA(Over-The-Air) 업데이트의 안전성을 확보하고 차량 ID를 관리하며 데이터 수익화 모델을 가능하게 합니다. 라이드 헤일링에서 구독 모델에 이르기까지 블록체인은 자동차와 관련된 모든 거래 및 데이터 포인트가 안전하고 추적 가능하다는 것을 보장합니다.

지역별 인사이트

북미가 유망한 지역이 된다.

북미 자동차 블록체인 기술 시장은 견고한 디지털 인프라, 높은 R&D 비용, 강력한 업계 파트너십에 견인되어 2024년에 큰 수익을 올렸습니다. 미국에 본사를 둔 OEM과 기술 선두는 디지털 차량 타이틀, EV 배터리 추적, 자율 주행 데이터 검증의 파일럿 프로젝트에서 주도권을 잡고 있습니다. 또한 이 지역은 블록체인 혁신에 대한 규제 개방성을 통해 혜택을 누리고 있으며, 자동차 회사는 장벽을 줄이고 새로운 솔루션을 확대할 수 있습니다.

자동차 블록체인 기술 시장에 진입하는 주요 기업으로는 MOBI, Amazon, SAP SE, Tech Mahindra Limited, IBM Corporation, BigchainDB GmbH, Microsoft Corporation, Oracle Corporation, R3, Accenture plc 등이 있습니다.

자동차 블록체인 기술 시장의 선두 기업은 시장에서의 지위를 강화하기 위해 전략적 제휴, 파일럿 프로그램, 제품 혁신을 추진하고 있습니다. 각 회사는 자동차 OEM에 블록체인 Az A 서비스(BaaS) 플랫폼을 제공하여 보다 빠르고 안전한 배포를 가능하게 합니다. R3 및 BigchainDB와 같은 기업은 공급망, 데이터 보안 및 스마트 계약의 용도에 맞는 맞춤형 블록체인 프로토콜 개발에 주력하고 있습니다. 한편 자동차 제조업체와 하이테크 기업의 컨소시엄인 MOBI는 상호 운용성을 촉진하기 위해 업계 전반의 표준을 구축하고 있습니다.

목차

제1장 조사 방법

조사 디자인

조사 접근

데이터 수집 방법

기본 추정과 계산

기준연도 계산

GMI 독자적인 AI 시스템

AI를 활용한 조사 강화

소스 일관성 프로토콜

AI의 정밀도 지표

예측 모델

1차 조사와 검증

시장 예측의 주요 동향

정량화된 시장 영향 분석

성장 파라미터 예측에 대한 수학적 영향

시나리오 분석 프레임워크

1차 정보의 일부(단, 이것에 한정되는 것은 아니다)

데이터 마이닝 소스

2차

유료소스

공개 정보원

지역별 정보원

조사의 궤적과 신뢰도 점수

조사 트레일의 구성요소 :

채점 구성 요소

조사의 투명성에 관한 보충

소스 기여 프레임워크

품질 보증 지표

신뢰에 대한 헌신

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

공급망의 투명성과 추적성에 대한 수요 증가

커넥티드카나 자율주행차의 보급 확대

사기 방지와 안전한 거래의 필요성 증가

모빌리티 아즈 어 서비스(MaaS)와 쉐어드 차량 플랫폼 확대

업계의 잠재적 위험 및 과제

블록체인 시스템의 구현 및 통합에 드는 높은 비용

자동차 네트워크의 표준화와 상호 운용성의 부족

시장 기회

예측 유지보수를 위한 블록체인과 IoT 및 AI의 통합

차량 소유권 이전 및 디지털 ID 솔루션의 채택

스마트 모빌리티 이니셔티브에 의한 신흥 시장 진출

중소기업과 제2/제3공급업체의 통합

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현재의 기술 동향

신규 기술

특허 분석

가격 동향과 경제 분석

이용 사례

최상의 시나리오

투자 상황과 자금 조달 분석

세계 자동차 기술 투자 동향

자동차 업계의 블록체인 기술 투자

지역 투자 패턴과 정부의 지원

기업투자와 M&A 활동

비용편익분석

실장 비용 구조와 투자 요건

운용상의 이점과 효율성 향상

재무상의 이익과 비용 절감

전략적 이점과 경쟁 우위

차량 ID와 라이프사이클 관리

자율주행차와 데이터 관리

센서 데이터의 무결성과 검증

머신러닝 모델 관리

책임과 사고 조사

데이터 수익화 및 공유

모빌리티 서비스와 결제의 통합

라이드 쉐어와 카 쉐어의 플랫폼

전기차 충전 및 에너지 관리

스마트시티 통합과 인프라

보험 및 리스크 관리

사이버 보안과 데이터 보호의 틀

자동차 사이버 보안과 블록체인 통합

블록체인 보안 및 위협 평가

데이터 프라이버시 및 컴플라이언스 관리

사고 대응과 사업 계속

지속가능성과 환경영향 분석

이산화탄소 배출량 추적 및 보고

순환형 경제와 재료 추적성

환경 컴플라이언스 및 보고

그린테크놀로지와 혁신

미래의 기술 로드맵과 혁신의 타임라인

블록체인 기술의 진화(2024-2034)

자동차 기술 통합의 타임라인

업계의 변혁과 융합의 시나리오

시장의 진화와 혼란의 평가

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병과 인수

파트너십 및 협업

신제품 발매

확장계획과 자금조달

제5장 시장 추정 및 예측 : 유형별, 2021-2034

주요 동향

퍼블릭 블록체인

프라이빗 블록체인

하이브리드 블록체인

제6장 시장 추정 및 예측 : 구성요소별, 2021-2034

주요 동향

솔루션

서비스

제7장 시장 추정 및 예측 : 차량별, 2021-2034

주요 동향

승용차

해치백

세단

SUV

MPV

상용차

소형 상용차(LCV)

중형 상용차(MCV)

대형 상용차(HCV)

이륜차

제8장 시장 추정 및 예측 : 용도별, 2021-2034

주요 동향

공급망 관리

차량 ID와 라이프사이클 관리

자율주행차의 데이터 관리

모빌리티 서비스와 결제

기타

제9장 시장 추정 및 예측 : 조직 규모별, 2021-2034

주요 동향

중소기업

대기업

제10장 시장 추정 및 예측 : 최종 용도별, 2021-2034

주요 동향

OEM

자동차 소유자

서비스 제공업체로서의 이동성

기타

제11장 시장 추정 및 예측 : 지역별, 2021-2034

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

북유럽 국가

아시아태평양

중국

인도

일본

호주

한국

필리핀

인도네시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

나이지리아

제12장 기업 프로파일

세계 기업

Amazon

BMW 그룹

ConsenSys

Ford Motor

General Motors

Hyperledger Foundation

Hyundai Motor

IBM

Mercedes-Benz

Microsoft

Oracle

R3

Renault-Nissan-Mitsubishi Alliance

SAP

Toyota Motor

Volkswagen

지역 기업

MOBI

VeChain

OriginTrail

Chronicled

Ambrosus

Provenance

Everledger

신규 기업

CarVertical

AutoBlock

SHW

영문 목차

영문목차

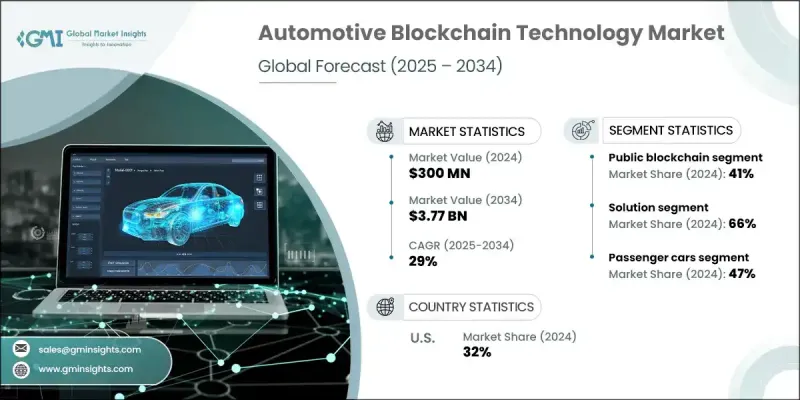

The Global Automotive Blockchain Technology Market was valued at USD 300 million in 2024 and is estimated to grow at a CAGR of 29% to reach USD 3.77 billion by 2034.

As vehicles become increasingly connected and software-driven, automakers are facing growing concerns around data integrity, cybersecurity, and real-time communication. Blockchain offers a decentralized, tamper-proof system to securely track and verify data across a vehicle's lifecycle from manufacturing and parts sourcing to software updates and ownership transfers.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$300 Million

Forecast Value

$3.77 Billion

CAGR

29%

Increasing Prevalence of Public Blockchain

The public blockchain segment is expected to gain strong traction through 2034 driven by its unmatched transparency and decentralized structure. Public blockchains allow multiple stakeholders including automakers, regulators, suppliers, and end use to access and verify data in real-time, without relying on a central authority. This model is particularly useful for vehicle history tracking, ownership records, and shared mobility applications.

Rising Adoption of Solutions

The solutions segment from the automotive blockchain technology market held sizeable share in 2024. Automakers and fleet operators are increasingly investing in end-to-end blockchain platforms that offer a complete suite of services from smart contract execution to supply chain management and data authentication. These solutions reduce operational overhead, enhance transparency, and help companies to future-proof their digital infrastructure.

Passenger Cars to Gain Traction

The passenger cars segment held substantial share in 2024, owing to the rapid integration of digital technologies in modern vehicles. As consumers demand smarter, safer, and more connected driving experiences, automakers are leveraging blockchain to secure over-the-air (OTA) updates, manage vehicle identity, and enable data monetization models. From ride-hailing to subscription models, blockchain ensures that every transaction and data point tied to a car is secure and traceable.

Regional Insights

North America to Emerge as a Lucrative Region

North America automotive blockchain technology market generated significant revenues in 2024, driven by a robust digital infrastructure, high R&D spending, and strong industry partnerships. U.S. based OEMs and technology giants are leading the charge with pilot projects in digital vehicle titles, EV battery tracking, and autonomous vehicle data verification. The region also benefits from regulatory openness to blockchain innovation, allowing automotive companies to scale new solutions with fewer barriers.

Major players involved in the automotive blockchain technology market include MOBI, Amazon, SAP SE, Tech Mahindra Limited, IBM Corporation, BigchainDB GmbH, Microsoft Corporation, Oracle Corporation, R3, Accenture plc.

Leading players in the automotive blockchain technology market are pursuing strategic collaborations, pilot programs, and product innovation to strengthen their market position. Companies are offering blockchain-as-a-service (BaaS) platforms to automotive OEMs, enabling faster and more secure deployment. Firms such as R3 and BigchainDB are focusing on developing customizable blockchain protocols tailored for supply chain, data security, and smart contract applications. Meanwhile, MOBI, a consortium of automakers and tech firms, is building industry-wide standards to promote interoperability.

Table of Contents

Chapter 1 Methodology

1.1 Research design

1.1.1 Research approach

1.1.2 Data collection methods

1.1.3 Base estimates and calculations

1.1.4 Base year calculation

1.1.5 GMI proprietary AI system

1.1.5.1 AI-Powered research enhancement

1.1.5.2 Source consistency protocol

1.1.5.3 AI accuracy metrics

1.2 Forecast model

1.3 Primary research and validation

1.3.1 Key trends for market estimates

1.3.2 Quantified market impact analysis

1.3.2.1 Mathematical impact of growth parameters on forecast

1.3.3 Scenario Analysis Framework

1.4 Some of the primary sources (but not limited to)

1.5 Data mining sources

1.5.1 Secondary

1.5.1.1 Paid Sources

1.5.1.2 Public Sources

1.5.1.3 Sources, by region

1.6 Research Trail & Confidence Scoring

1.6.1 Research Trail Components:

1.6.2 Scoring Components

1.7 Research transparency addendum

1.7.1 Source attribution framework

1.7.2 Quality assurance metrics

1.7.3 Our commitment to trust

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Regional

2.2.2 Type

2.2.3 Component

2.2.4 Vehicle

2.2.5 Application

2.2.6 Organization Size

2.2.7 End Use

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Increasing demand for supply chain transparency and traceability

3.2.1.2 Rising adoption of connected and autonomous vehicles

3.2.1.3 Growing need for fraud prevention and secure transactions

3.2.1.4 Expansion of mobility-as-a-service (MaaS) and shared vehicle platforms

3.2.2 Industry pitfalls and challenges

3.2.2.1 High implementation and integration costs for blockchain systems

3.2.2.2 Lack of standardization and interoperability across automotive networks

3.2.3 Market opportunities

3.2.3.1 Integration of blockchain with IoT and AI for predictive maintenance

3.2.3.2 Adoption in vehicle ownership transfer and digital identity solutions

3.2.3.3 Expansion into emerging markets with smart mobility initiatives

3.2.3.4 SME and tier 2/3 supplier integration

3.3 Regulatory landscape

3.3.1 North America

3.3.2 Europe

3.3.3 Asia Pacific

3.3.4 Latin America

3.3.5 Middle East & Africa

3.4 Porter's analysis

3.5 PESTEL analysis

3.6 Technology and innovation landscape

3.6.1 Current technological trends

3.6.2 Emerging technologies

3.7 Patent analysis

3.8 Pricing trends and economic analysis

3.9 Use cases

3.10 Best-case scenario

3.11 Investment landscape and funding analysis

3.11.1 Global automotive technology investment trends

3.11.2 Blockchain technology investment in automotive

3.11.3 Regional investment patterns and government support

3.11.4 Corporate investment and M&A activity

3.12 Cost-benefit analysis

3.12.1 Implementation cost structure and investment requirements

3.12.2 Operational benefits and efficiency gains

3.12.3 Financial benefits and cost reduction

3.12.4 Strategic benefits and competitive advantage

3.13 Vehicle identity and lifecycle management

3.14 Autonomous vehicle and data management

3.14.1 Sensor data integrity and validation

3.14.2 Machine learning model management

3.14.3 Liability and accident investigation

3.14.4 Data monetization and sharing

3.15 Mobility services and payment integration

3.15.1 Ride-sharing and car-sharing platforms

3.15.2 Electric vehicle charging and energy management

3.15.3 Smart city integration and infrastructure

3.15.4 Insurance and risk management

3.16 Cybersecurity and data protection framework

3.16.1 Automotive cybersecurity and blockchain integration

3.16.2 Blockchain security and threat assessment

3.16.3 Data privacy and compliance management

3.16.4 Incident response and business continuity

3.17 Sustainability and environmental impact analysis

3.17.1 Carbon footprint tracking and reporting

3.17.2 Circular economy and material traceability

3.17.3 Environmental compliance and reporting

3.17.4 Green technology and innovation

3.18 Future technology roadmap and innovation timeline