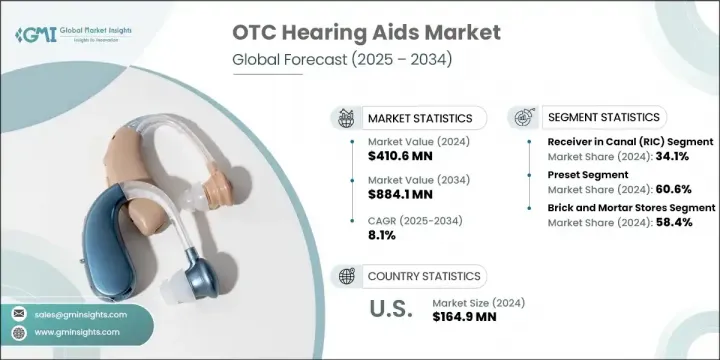

OTC 보청기 세계 시장은 2024년에는 4억 1,060만 달러에 달했고, CAGR 8.1%로 성장하여 2034년에는 8억 8,410만 달러에 이를 것으로 예측됩니다.

난청 환자 증가, 급속한 고령화, 기존의 처방 보청기에 비해 시판 보청기가 저렴한 가격 등이 시장 성장에 박차를 가하고 있습니다. 특히 보건기구에 의한 지지적인 규제의 움직임, 처방전 모델에 대한 충분한 보험 적용이 없는 것이, 보다 많은 소비자가 자기 관리형 이용하기 쉬운 대체품을 요구하는 원동력이 되고 있습니다. 또한 블루투스 연결, 스마트폰과의 연계, 앱에 의한 소리의 조정 등 하이테크를 구사한 기능의 인지도와 이용 가능성이 높아지고 있는 것도 특히 디지털 네이티브 유저에게 OTC 보청기의 매력을 높이고 있습니다. 이러한 혁신은 합리적인 가격과 고급 청각 솔루션의 성능 차이를 줄이고 소비자층을 확대하며 시장 침투를 뒷받침합니다.

이어폰 분야는 액티브한 라이프 스타일을 지원하고 스마트폰과 호환되는 컴팩트한 무선 오디오 장치 수요가 급증하기 때문에 2034년까지 연평균 복합 성장률(CAGR) 8.4%로 성장할 것으로 예측됩니다. 경량 구조와 쾌적성이 중심적인 촉진요인이며, 오픈 피트 설계의 채택에 의해 주위의 소리의 듣기 쉬움이 향상하고 있습니다. 스피커와 마이크를 분리한 RIC 모델은 하울링을 최소화하고, 선명도를 향상시키고, 다양한 청력 상실에 대응합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작금액 | 4억 1,060만 달러 |

| 예측 금액 | 8억 8,410만 달러 |

| CAGR | 8.1% |

2024년에는 프리셋형 OTC 보청기가 60.6%의 점유율을 차지했습니다. 프로그래밍이 불필요한 프리셋 유형은 알기 쉬운 기능을 요구하는 소비자, 특히 최초의 유저나 노인에게 소구합니다. 약국이나 전자상거래 플랫폼에서의 소매 성장도 보급을 뒷받침하고 있습니다. 증폭 기술의 진보로 품질이 더욱 향상되고 경도에서 중등도의 청력을 필요로 하는 사람들에게 이러한 장비는 신뢰할 수 있는 옵션이 되었습니다.

북미 OTC 보청기 2024년 점유율은 42.6% 이 지역은 특히 미국과 캐나다에서 고령화율이 높고, 소비자의 자기관리형 케어 툴의 도입이 진행되는 헬스케어 환경의 혜택을 받고 있습니다. 디지털에 익숙하고 기술에 대한 액세스가 용이한 것이 보급을 가속시키고 있습니다. 주요 약국 체인과 온라인 마켓플레이스를 포함한 강력한 소매 생태계가 제품에 대한 접근성을 높입니다. 이를 통해 OTC 보청기는 특히 건강 의식이 높고 기술에 익숙한 사용자를 중심으로 보다 폭넓은 층에 침투하고 있습니다.

OTC 보청기 시장의 유력 기업으로는 NuvoMed, SOUNDWAVE HEARING, Lucid Hearing, AUDICUS, Starkey, AcoSound, NUHEARA, EARGO, AUSTAR, HearX Group, Audien Hearing, WS Audiology, B. Braun, GN Store Nord, MD Hearing, Sonova 등이 있습니다. 주요 OTC 보청기 제조업체의 주요 전략에는 소리의 명료성, 배터리 수명 및 연결성을 높이기 위한 R&D에 대한 적극적인 투자가 포함됩니다. 각 회사는 맞춤화를 돕기 위해 앱 기반 컨트롤을 최적화하고 소비자 이어폰의 편안함과 스타일을 반영하는 제품을 배포합니다. 소매 체인과 온라인 스토어와의 전략적 제휴로 인지도가 확대되고 타겟 마케팅을 통해 젊은이와 처음으로 이어폰을 구입하는 사용자의 브랜드 리콜이 향상되고 있습니다. 또한 기업은 제품 인가를 가속화하고 시장에서 조기 우위를 확보하기 위해 규제 당국과의 제휴를 추진하고 있습니다. 구독 계획과 원격 지원 제공은 장기 고객 로열티를 구축하는 데에도 도움이 됩니다.

The Global OTC Hearing Aids Market was valued at USD 410.6 million in 2024 and is estimated to grow at a CAGR of 8.1% to reach USD 884.1 million by 2034. The rise in hearing loss cases, along with a rapidly aging population and the affordability of over-the-counter options compared to traditional prescription hearing aids, is fueling market growth. Supportive regulatory moves, particularly from health agencies, and the lack of sufficient insurance coverage for prescription models have driven more consumers to seek self-managed, accessible alternatives. In addition, growing awareness and the increasing availability of tech-enabled features like Bluetooth connectivity, smartphone integration, and app-controlled sound adjustment are making OTC hearing aids more appealing, especially to digital-native users. These innovations are narrowing the performance gap between budget-friendly and high-end hearing solutions, expanding the consumer base and pushing market penetration.

The earbuds segment is projected to grow at a CAGR of 8.4% through 2034, as demand surges for compact, wireless audio devices that support active lifestyles and are compatible with smartphones. Lightweight construction and comfort are core drivers, while the inclusion of open-fit designs ensures better ambient sound perception. RIC models with separate speaker and mic components minimize feedback and offer improved clarity, catering to varied degrees of hearing loss.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $410.6 Million |

| Forecast Value | $884.1 Million |

| CAGR | 8.1% |

In 2024, the preset OTC hearing aids segment held share at 60.6%, owing to their simplicity, immediate usability, and cost advantages. With no need for programming, preset models appeal to consumers seeking straightforward functionality, particularly first-time users and older adults. Retail growth across pharmacies and e-commerce platforms has also supported widespread availability. Advances in amplification technology have further improved quality, making these devices a reliable option for those with mild to moderate hearing needs.

North America OTC Hearing Aids Market held 42.6% share in 2024. The region benefits from a large aging population, especially in the U.S. and Canada, and a healthcare environment where consumers are increasingly adopting self-directed care tools. High digital fluency and easy access to technology accelerate adoption. A strong retail ecosystem, including major pharmacy chains and online marketplaces, enhances product accessibility. This has helped OTC hearing aids reach broader audiences, particularly among health-conscious and tech-savvy users.

Prominent companies in the OTC Hearing Aids Market include NuvoMed, SOUNDWAVE HEARING, Lucid Hearing, AUDICUS, Starkey, AcoSound, NUHEARA, EARGO, AUSTAR, HearX Group, Audien Hearing, WS Audiology, B. Braun, GN Store Nord, MD Hearing, and Sonova. Key strategies among leading OTC hearing aid manufacturers include aggressive investment in R&D to enhance sound clarity, battery life, and connectivity. Companies are optimizing app-based controls for ease of customization and rolling out products that mirror the comfort and style of consumer earbuds. Strategic alliances with retail chains and online stores have expanded visibility, while targeted marketing is improving brand recall among younger and first-time buyers. In addition, players are engaging in regulatory collaborations to expedite product approvals and gain early market advantage. Offering subscription plans and remote support also helps in building long-term customer loyalty.