접착제 및 실란트 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Adhesives and Sealants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1801933

리서치사:Global Market Insights Inc.

발행일:2025년 08월

페이지 정보:영문 192 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

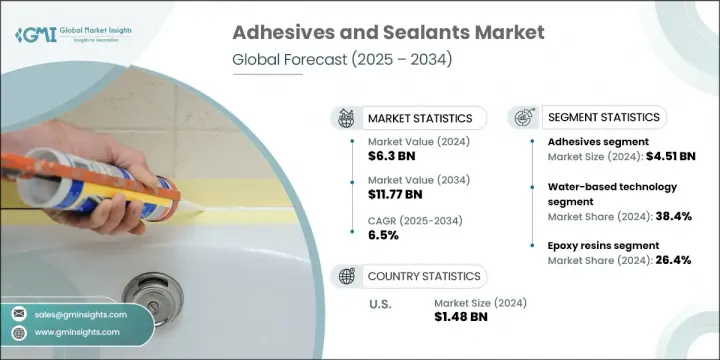

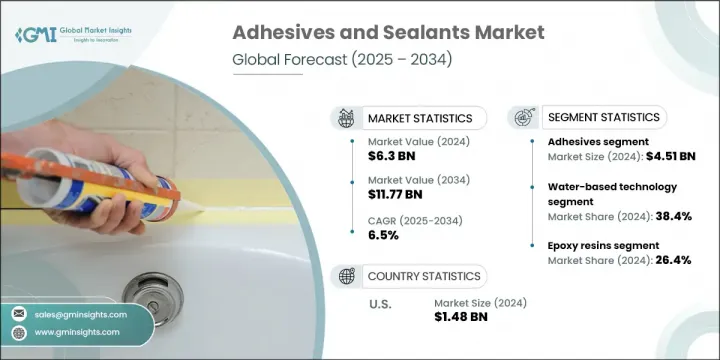

접착제 및 실란트 세계 시장 규모는 2024년에 63억 달러에 달했고, CAGR 6.5%로 성장하여 2034년에는 117억 7,000만 달러에 이를 것으로 예측됩니다.

이 시장은 여러 산업에 걸친 제품의 강도, 수명, 내성을 높이는 접착 및 씰링 재료의 개발과 사용을 중심으로 전개되고 있습니다. 이러한 재료는 건설, 자동차, 전자기기, 포장 등의 용도에서 중요한 역할을 하며 날씨, 누출, 외부 오염물질로부터 보호를 제공합니다. 인프라의 현대화와 가볍고 에너지 효율적인 자동차에 대한 세계의 뒷받침으로 인해 수요는 계속 가속화되고 있습니다.

성능, 환경적 적합성, 재료 범용성에 중점을 둔 혁신은 제품의 신뢰성과 효율성을 향상시키면서 제조업체가 진화하는 업계 표준을 충족하는 데 도움이 됩니다. 각 회사는 가혹한 조건 하에서 보다 강력한 접착을 실현하고 화학물질 및 온도 변동에 견디며 경화 시간을 단축하고 보다 신속한 조립 공정을 지원하는 고급 접착제 및 실란트 처방을 개발하는 경향을 강화하고 있습니다. 이러한 개선은 작업 효율을 향상시킬 뿐만 아니라 최종 제품의 수명 주기를 연장합니다. 동시에, 친환경 솔루션의 추진은 세계의 지속가능성 목표에 따라 낮은 VOC, 바이오, 재활용 가능한 재료로의 전환을 추진하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

63억 달러

예측 금액

117억 7,000만 달러

CAGR

6.5%

접착제 분야는 2024년에 45억 1,000만 달러를 차지했고, 2034년까지 6.5%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예측됩니다. 에폭시 및 폴리우레탄과 같은 구조용 접착제는 자동차 및 항공우주 응용 분야에서 우수한 접착력을 발휘하기 때문에 시장을 선도하고 있습니다. 접착제 분야에는 감압 접착제, 핫멜트, 솔벤트 유형 및 수성 유형이 있습니다.

기술 중에서는 수성 접착제 부문이 2024년에 38.4%의 점유율을 차지했고 지속 가능한 저 VOC 제품의 상승이 그 원동력이 되고 있습니다. 보다 안전한 적용과 환경적 적합성으로 인해 가구, 자동차, 포장, 건축 분야에서의 채택이 증가하고 있습니다. 제조업체가 대기질 규제에의 적합을 목표로 하는 가운데, 수성 접착제는 산업용과 상업용 모두에서 계속 인기를 끌고 있습니다.

미국 접착제 및 실란트 시장은 88.5%의 점유율을 차지했으며, 2024년에는 14억 8,000만 달러 수익을 올렸습니다. 미국 시장은 첨단 제조업, EV 생산, 국가 인프라 업그레이드에 대한 왕성한 투자에 힘입어 2034년까지 지속적인 성장이 예상되고 있습니다. 교통망과 공공 건축물을 대상으로 하는 연방 정부의 자금 지원 이니셔티브는 고성능 접착제 및 밀봉 제품에 대한 수요를 끌어올리고 있습니다. 또한 항공우주, 일렉트로닉스, 지속가능한 건설의 등장이 접착 기술의 주요 시장으로서의 국가의 역할을 강화하고 있습니다.

접착제 및 실란트 세계 시장에서 유력한 기업은 BASF SE, Dow Inc., Henkel AG & Co.KGaA, Sika AG, 3M Company 등입니다. 접착제 및 실링제 업계의 주요 기업은 적극적인 R&D 투자, 친환경 제품 개척, 지역 확대를 통해 시장 지위를 높이고 있습니다. 환경 규제와 소비자의 지속가능성에 대한 요구를 충족시키기 위해 낮은 VOC 및 바이오 접착제로의 전략적 변화가 진행되고 있습니다. 기업은 리드 타임을 단축하고 업무 효율을 높이기 위해 공급망을 강화하고 고성장 지역의 제조 능력을 확대하고 있습니다. 전략적 합병, 인수, 파트너십은 보다 광범위한 제품 포트폴리오와 시장 진입을 가능하게 합니다. 전기차, 전자기기, 스마트 인프라에 맞는 맞춤형 접착제 솔루션도 주목받고 있으며 차세대 산업 수요에 부응하고 있습니다.

목차

제1장 조사 방법

시장의 범위와 정의

조사 디자인

조사 접근

데이터 수집 방법

데이터 마이닝 소스

세계

지역/국가

기본 추정과 계산

기준연도 계산

시장 예측의 주요 동향

1차 조사와 검증

1차 정보

예측 모델

조사의 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

경량 제조로의 이행

그린빌딩과 친환경 배합

e모빌리티와 일렉트로닉스의 성장

포장의 혁신과 안전 요건

업계의 잠재적 위험 및 과제

환경과 규제의 압력

원재료 가격 변동

시장 기회

지속 가능하고 바이오 대체품 수요

모듈식 및 조립식 건설 증가

확대하는 헬스케어 및 의료기기 시장

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현재의 기술 동향

신흥기술

가격 동향

지역별

제품 유형별

코스트 내역 분석

특허 분석

지속가능성과 환경 측면

지속가능한 관행

폐기물 감축 전략

생산에 있어서의 에너지 효율

환경 친화적 인 노력

탄소발자국의 고려

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병과 인수

파트너십 및 협업

신제품 발매

확장계획과 자금조달

제5장 시장 추정 및 예측 : 제품 유형별, 2021년-2034년

주요 동향

접착제 시장

구조용 접착제

에폭시 접착제

폴리우레탄 접착제

아크릴계 접착제

메틸메타크릴레이트 접착제

시아노아크릴레이트 접착제

감압 접착제

아크릴 PSA

고무계 PSA

실리콘 점착제

핫멜트 접착제

EVA 핫멜트

폴리아미드 핫멜트

폴리올레핀 핫멜트

반응성 핫멜트

수성 접착제

용제계 접착제

기타 접착제의 유형

실란트 시장

실리콘 실란트

RTV 실리콘 실란트

구조용 유리 실란트

폴리우레탄 실란트

아크릴 실란트

폴리설파이드 실란트

부틸 실란트

기타 실란트의 유형

제6장 시장 추정 및 예측 : 기술별, 2021년-2034년

주요 동향

수성 기술

용제계 기술

핫멜트 기술

반응형 기술

UV/광경화 기술

압력 감지 기술

기타

제7장 시장 추정 및 예측 : 수지 유형별, 2021년-2034년

주요 동향

에폭시 수지

폴리우레탄 수지

아크릴 수지

실리콘 수지

폴리비닐아세테이트(PVA)

에틸렌 비닐 아세테이트(EVA)

스티렌계 블록 공중합체

기타

제8장 시장 추정 및 예측 : 용도별, 2021년-2034년

주요 동향

구조 결합

조립 작업

씰링과 개스킷

표면 보호

전기 절연

열 관리

진동 감쇠

기타

제9장 시장 추정 및 예측 : 최종 이용 산업별, 2021년-2034년

주요 동향

건축 및 건설

주택건설

상업건설

인프라 프로젝트

자동차 및 수송

승용차

상용차

전기자동차

애프터마켓

패키지

연질 포장

경질 포장

라벨 및 테이프

전자 및 전기

소비자 일렉트로닉스

반도체 패키징

PCB 어셈블리

디스플레이 기술

항공우주 및 방어

상용항공

군사 용도

우주 용도

의료 및 헬스케어

의료기기

외과 수술 용도

의약품 포장

신발과 가죽 제품

목공과 가구

해양 용도

기타

제10장 시장 추정 및 예측 : 지역별, 2021년-2034년

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

기타 중동 및 아프리카

제11장 기업 프로파일

3M Company

Arkema Group(Bostik)

Ashland Global Holdings Inc.

Avery Dennison Corporation

BASF SE

Dow Inc.

DuPont de Nemours, Inc.

HB Fuller Company

Henkel AG &Co. KGaA

Huntsman Corporation

Illinois Tool Works Inc.(ITW)

Momentive Performance Materials Inc.

RPM International Inc.

Sika AG

Wacker Chemie AG

SHW

영문 목차

영문목차

The Global Adhesives and Sealants Market was valued at USD 6.3 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 11.77 billion by 2034. This market revolves around the development and use of bonding and sealing materials that enhance the strength, longevity, and resistance of products across multiple industries. These materials play a key role in construction, automotive, electronics, and packaging applications, where they provide protection against weather, leakage, and external contaminants. With the global push toward infrastructure modernization and lightweight, energy-efficient vehicles, demand continues to accelerate.

Innovations focused on performance, eco-compliance, and material versatility are helping manufacturers meet evolving industry standards while improving product reliability and efficiency. Companies are increasingly developing advanced adhesive and sealant formulations that deliver stronger bonding under extreme conditions, resist chemicals and temperature fluctuations, and reduce cure times to support faster assembly processes. These improvements not only boost operational efficiency but also extend the lifecycle of end-use products. Simultaneously, the push for eco-friendly solutions is driving the shift toward low-VOC, bio-based, and recyclable materials that align with global sustainability goals.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$6.3 Billion

Forecast Value

$11.77 Billion

CAGR

6.5%

The adhesives segment accounted for USD 4.51 billion in 2024 and is expected to maintain a strong CAGR of 6.5% through 2034. Structural adhesives such as epoxy and polyurethane lead the market due to their superior bonding in automotive and aerospace applications. The adhesives segment includes pressure-sensitive adhesives, hot melts, and both solvent- and water-based variants.

Among technologies, the water-based adhesives segment held 38.4% share in 2024, driven by the rise of sustainable, low-VOC products. Their safer application and environmental compatibility have increased adoption across furniture, automotive, packaging, and construction sectors. As manufacturers aim to align with air quality regulations, water-based adhesives continue to gain popularity for both industrial and commercial applications.

United States Adhesives and Sealants Market held an 88.5% share and generated USD 1.48 billion in 2024. The U.S. market is set for continued growth through 2034, supported by robust investments in advanced manufacturing, EV production, and national infrastructure upgrades. Federal funding initiatives targeting transportation networks and public buildings are boosting the demand for high-performance adhesive and sealing products. Additionally, the rise of aerospace, electronics, and sustainable construction is reinforcing the country's role as a key market for adhesive technologies.

Prominent players in the Global Adhesives and Sealants Market include BASF SE, Dow Inc., Henkel AG & Co. KGaA, Sika AG, and 3M Company. Major companies in the adhesives and sealants industry are enhancing their market position through targeted R&D investments, eco-friendly product development, and regional expansion. There's a strategic shift toward low-VOC and bio-based adhesives to address environmental regulations and consumer sustainability demands. Companies are strengthening supply chains and expanding manufacturing capabilities in high-growth regions to reduce lead times and boost operational efficiency. Strategic mergers, acquisitions, and partnerships are enabling broader product portfolios and market access. Custom adhesive solutions tailored for electric vehicles, electronics, and smart infrastructure are also a focus, helping meet next-gen industrial demands.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Regional

2.2.2 Product type

2.2.3 Technology

2.2.4 Resin type

2.2.5 Application

2.2.6 End Use Industry

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Shift toward lightweight manufacturing

3.2.1.2 Green building and eco-friendly formulations

3.2.1.3 Growth of e-mobility and electronics

3.2.1.4 Packaging innovation and safety requirements

3.2.2 Industry pitfalls and challenges

3.2.2.1 Environmental and regulatory pressure

3.2.2.2 Raw material price volatility

3.2.3 Market opportunities

3.2.3.1 Demand for sustainable and bio-based alternatives

3.2.3.2 Rise in modular and prefabricated construction

3.2.3.3 Expanding healthcare and medical devices market

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter’s analysis

3.6 PESTEL analysis

3.7 Technology and Innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Price trends

3.8.1 By region

3.8.2 By product type

3.9 Cost breakdown analysis

3.10 Patent analysis

3.11 Sustainability and environmental aspects

3.11.1 Sustainable practices

3.11.2 Waste reduction strategies

3.11.3 Energy efficiency in production

3.11.4 Eco-friendly Initiatives

3.12 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 North America

4.2.2 Europe

4.2.3 Asia Pacific

4.2.4 LATAM

4.2.5 MEA

4.3 Competitive analysis of major market players

4.4 Competitive positioning matrix

4.5 Strategic outlook matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New Product Launches

4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 - 2034 (USD Billion, Kilo Tons)

5.1 Key trends

5.2 Adhesives market

5.2.1 Structural adhesives

5.2.1.1 Epoxy adhesives

5.2.1.2 Polyurethane adhesives

5.2.1.3 Acrylic adhesives

5.2.1.4 Methyl methacrylate adhesives

5.2.1.5 Cyanoacrylate adhesives

5.2.2 Pressure sensitive adhesives

5.2.2.1 Acrylic PSA

5.2.2.2 Rubber-based PSA

5.2.2.3 Silicone PSA

5.2.3 Hot melt adhesives

5.2.3.1 EVA hot melts

5.2.3.2 Polyamide hot melts

5.2.3.3 Polyolefin hot melts

5.2.3.4 Reactive hot melts

5.2.4 Water-based adhesives

5.2.5 Solvent-based adhesives

5.2.6 Other adhesive types

5.3 Sealants market

5.3.1 Silicone sealants

5.3.1.1 RTV silicone sealants

5.3.1.2 Structural glazing sealants

5.3.2 Polyurethane sealants

5.3.3 Acrylic sealants

5.3.4 Polysulfide sealants

5.3.5 Butyl sealants

5.3.6 Other sealant types

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 (USD Billion, Kilo Tons)

6.1 Key trends

6.2 Water-based technology

6.3 Solvent-based technology

6.4 Hot melt technology

6.5 Reactive technology

6.6 UV/light curable technology

6.7 Pressure sensitive technology

6.8 Others

Chapter 7 Market Estimates & Forecast, By Resin Type, 2021 - 2034 (USD Billion, Kilo Tons)

7.1 Key trends

7.2 Epoxy resins

7.3 Polyurethane resins

7.4 Acrylic resins

7.5 Silicone resins

7.6 Polyvinyl acetate (PVA)

7.7 Ethylene vinyl acetate (EVA)

7.8 Styrenic block copolymers

7.9 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion, Kilo Tons)

8.1 Key trends

8.2 Structural bonding

8.3 Assembly operations

8.4 Sealing and gasketing

8.5 Surface protection

8.6 Electrical insulation

8.7 Thermal management

8.8 Vibration damping

8.9 Others

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 (USD Billion, Kilo Tons)

9.1 Key trends

9.2 Building and construction

9.2.1 Residential construction

9.2.2 Commercial construction

9.2.3 Infrastructure projects

9.3 Automotive and transportation

9.3.1 Passenger vehicles

9.3.2 Commercial vehicles

9.3.3 Electric vehicles

9.3.4 Aftermarket

9.4 Packaging

9.4.1 Flexible packaging

9.4.2 Rigid packaging

9.4.3 Labels and tapes

9.5 Electronics and electrical

9.5.1 Consumer electronics

9.5.2 Semiconductor packaging

9.5.3 PCB assembly

9.5.4 Display technologies

9.6 Aerospace and defense

9.6.1 Commercial aviation

9.6.2 Military applications

9.6.3 Space applications

9.7 Medical and healthcare

9.7.1 Medical devices

9.7.2 Surgical applications

9.7.3 Pharmaceutical packaging

9.8 Footwear and leather

9.9 Woodworking and furniture

9.10 Marine applications

9.11 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion, Kilo Tons)