EV Platform Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1801916

리서치사:Global Market Insights Inc.

발행일:2025년 08월

페이지 정보:영문 310 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

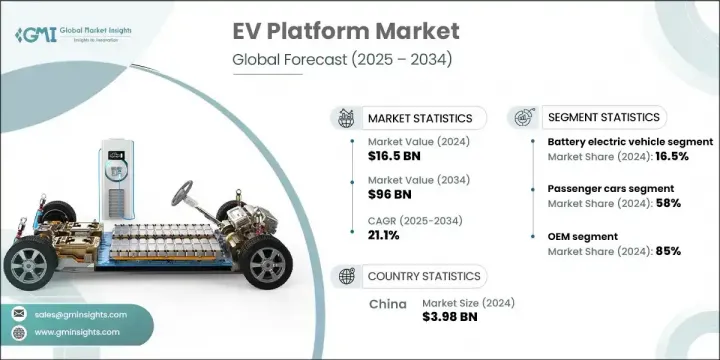

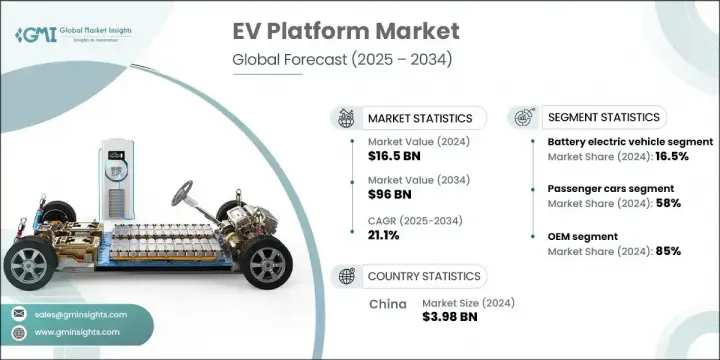

전 세계 EV 플랫폼 시장은 2024년에는 165억 달러에 달했고, CAGR 21.1%로 성장하고, 2034년에는 960억 달러에 이를 것으로 추정됩니다.

지속가능하고 무공해 이동성 솔루션으로의 이동 증가는 EV 플랫폼의 급속한 혁신에 불을 붙였습니다. 이러한 플랫폼은 현재 자율주행, 배터리 통합, 확장 가능한 파워트레인 등의 고급 기능을 지원하는 모듈형 소프트웨어 정의 시스템으로 진화하고 있습니다. 자동차 제조업체는 비용 효율적인 생산과 에너지 효율 향상을 실현하면서 차량 클래스를 넘어 유연한 아키텍처를 가능하게 하는 플랫폼을 설계하고 있습니다.

AI 주도의 기능과 무선 업데이트는 항속 거리와 성능을 최적화하는데 있어서 매우 중요한 역할을 합니다. 팬데믹은 디지털 퍼스트 차량 경험에 대한 수요를 가속화하고 각 회사가 비접촉 기능 및 실시간 연결 도구를 플랫폼 설계에 통합하도록 추진했습니다. 원격 진단, 음성 보조 제어, 지능형 루트 관리 등의 발전으로 EV 플랫폼은 기본 구조 부품에서 차세대 이동성을 위한 지능적이고 적응성이 높은 백본으로 승화되었습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작금액

165억 달러

예측 금액

960억 달러

CAGR

21.1%

배터리 전기자동차 분야의 점유율은 16.5%로, 2034년까지의 CAGR은 21%를 나타낼 전망입니다. BEV는 깨끗한 아키텍처와 차내 공간, 배터리 배치 및 설계 유연성을 극대화하는 스케이트 보드 스타일 플랫폼과의 호환성으로 지원됩니다. 순수한 전기자동차이기 때문에 연소 시스템이 필요 없으며 제조업체는 합리적인 구조를 설계하고 생산 비용을 줄이고 성능 효율을 높일 수 있습니다.

승용차 부문은 2024년에 58%로 가장 높은 점유율을 차지하고, 2025년부터 2034년까지의 CAGR은 20%로 강력한 성장을 유지할 것으로 예측됩니다. 전기 승용차의 보급은 소비자 수요가 증가하고 OEM에 의한 플랫폼 개발에 많은 투자가 이루어지고 있습니다. 각 회사는 세단, 해치백, 컴팩트 SUV에 최적화된 EV 전용 아키텍처를 구축하여 유연한 설계, 강화된 배터리 수명, 연결 기능 지원을 제공합니다. 이러한 광범위한 적응성을 통해 자동차 제조업체는 항속 거리, 안전성 및 디지털 통합을 향상시키고 대중 시장을 타겟팅할 수 있습니다.

중국의 EV 플랫폼 시장은 69%의 점유율을 차지하며, 2024년에는 39억 8,000만 달러를 창출합니다. 이 나라는 주요 EV 제조업체이자 소비자이자 시장에서 매우 중요한 역할을 하고 있습니다. 보조금, 생산 의무, 충전 인프라 투자를 통한 전략적 정부 지원으로 플랫폼 혁신에 강한 기세가 탄생했습니다. 국내 기업은 확장하는 전기자동차 사용자의 요구에 부응하면서 성능과 항속 거리의 균형을 맞추고 확장성이 뛰어난 저렴한 EV 플랫폼을 계속 개발하고 있습니다.

세계 EV 플랫폼 시장을 형성하는 주요 기업으로는 포드, 테슬라, 도요타, 폭스바겐, BMW, 제너럴 모터스, 볼보 등이 있습니다. 시장에서의 지위를 강화하기 위해 EV 플랫폼 분야의 기업들은 전략적 투자와 제휴를 선호합니다. OEM은 새로운 소프트웨어 구동 기술과의 호환성을 확보하면서 광범위한 차량 크기와 기능을 지원하는 모듈형 플랫폼을 개발하기 위해 연구 개발에 많은 투자를 하고 있습니다. 또한 자동차 제조업체는 연결, 충전 및 자율성을 위한 통합 생태계를 구축하기 위해 배터리 제조업체 및 하이테크 기업과 협력하고 있습니다. 또한 모터, 컨트롤러, 배터리 팩 등 주요 구성 요소를 제어하기 위해 많은 제조업체들이 수직 통합 모델을 채택하여 성능과 비용 관리를 강화하고 있습니다. 이러한 전략은 진화하는 EV 상황에서 확장성, 적응성 및 장기적인 경쟁력을 확보하는 데 도움이 됩니다.

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

부품 공급자

플랫폼 개발자

제조업자

유통 채널

최종 사용자

업계에 미치는 영향요인

성장 촉진요인

세계의 전기자동차 보급의 급증

배터리 기술의 진보

OEM의 모듈식 EV 아키텍처로의 전환

EV충전 인프라 확장

업계의 잠재적 위험 및 과제

EV 플랫폼에 대한 초기 투자액이 크다

신흥 지역에 있어서의 인프라의 미정비

시장 기회

EV-as-a-Service(EVaaS) 모델의 성장

자율형 및 커넥티드 기술과의 통합

상용차의 전동화

도시에서의 마이크로 이동성 솔루션 수요 증가

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현재의 기술 동향

신흥기술

특허 분석

가격 동향

지역별

차량별

이익률 분석

코스트 내역 분석

원재료비의 구성요소

제조 및 기계 비용

물류 및 배송 비용

인건비와 조립비

연구개발비 및 시험비

EV 플랫폼 시장 발전와 성숙 분석

ICE에의 적응으로부터 전용 플랫폼에의 역사적 개발

플랫폼 아키텍처의 진화의 타임라인

기술 도입 라이프사이클 분석

지속가능성과 환경 측면

지속가능한 관행

폐기물 감축 전략

생산에 있어서의 에너지 효율

환경 친화적인 노력

탄소발자국 고려

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병과 인수

파트너십 및 협업

신제품 발매

확장계획과 자금조달

제5장 시장 추정 및 예측 : 추진별, 2021년-2034년

주요 동향

배터리 전기자동차(BEV)

하이브리드 전기자동차(HEV)

플러그인 하이브리드 전기자동차(PHEV)

제6장 시장 추정 및 예측 : 차량별, 2021년-2034년

주요 동향

승용차

세단

SUV/크로스오버

해치백

상용차

소형 상용차

대형 상용차

제7장 시장 추정 및 예측 : 플랫폼별, 2021년-2034년

주요 동향

P0

P1

P2

P3

P4

제8장 시장 추정 및 예측 : 컴포넌트별, 2021년-2034년

주요 동향

배터리

서스펜션 시스템

모터 시스템

섀시

전자제어유닛(ECU)

기타

제9장 시장 추정 및 예측 : 판매 채널별, 2021년-2034년

주요 동향

OEM

애프터마켓

제10장 시장 추정 및 예측 : 지역별, 2021년-2034년

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

네덜란드

러시아

아시아태평양

중국

인도

일본

호주

한국

필리핀

인도네시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제11장 기업 프로파일

세계기업

BMW

Ford

General Motors

현대자동

Nissan Motor

Renault

Stellantis

Tesla

Toyota Motor

Volkswagen

지역 기업

Avatar Technology

BYD Auto

Leapmotor

Mahindra Electric

Seres

Tata Motors

Zeekr

신흥기업

Bollinger Motors

Canoo

Cenntro

Foxconn

Geely

Gaussin

Lucid Motors

NIO

OSVehicle

REE Automotive

Rivian Automotive

XPeng Motors

Zero Labs Automotive

SHW

영문 목차

영문목차

The Global EV Platform Market was valued at USD 16.5 billion in 2024 and is estimated to grow at a CAGR of 21.1% to reach USD 96 billion by 2034. The increasing shift toward sustainable and zero-emission mobility solutions has sparked rapid innovation in EV platforms. These platforms are now evolving into modular, software-defined systems that support advanced features like autonomous driving, battery integration, and scalable powertrains. Automakers are designing platforms that allow flexible architecture across vehicle classes while enabling cost-efficient production and improved energy efficiency.

AI-driven features and over-the-air updates play a crucial role in optimizing range and performance. The pandemic accelerated demand for digital-first vehicle experiences, pushing companies to integrate contactless functionalities and real-time connectivity tools into platform design. Advancements in remote diagnostics, voice-assisted controls, and intelligent route management have elevated EV platforms from basic structural components to intelligent, adaptable backbones for next-gen mobility.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$16.5 Billion

Forecast Value

$96 Billion

CAGR

21.1%

The battery electric vehicles segment held 16.5% share and is forecasted to grow at a CAGR of 21% through 2034. BEVs are favored due to their clean architecture and compatibility with skateboard-style platforms that maximize interior space, battery placement, and design flexibility. Their pure electric nature eliminates combustion systems, allowing manufacturers to engineer streamlined structures, reduce production costs, and boost performance efficiency.

The passenger car segment held the highest share at 58% in 2024 and is projected to maintain strong growth with a CAGR of 20% from 2025 to 2034. Widespread adoption of electric passenger vehicles has been fueled by growing consumer demand, paired with substantial OEM investment in platform development. Companies are creating dedicated EV architectures optimized for sedans, hatchbacks, and compact SUVs, offering flexible designs, enhanced battery life, and support for connected features. This broad adaptability enables automakers to target a mass-market audience with improved range, safety, and digital integration.

China EV Platform Market held 69% share, generating USD 3.98 billion in 2024. The country plays a pivotal role in the market as both a major EV manufacturer and consumer. Strategic government support through subsidies, production mandates, and charging infrastructure investments has created strong momentum in platform innovation. Domestic firms continue to engineer scalable, affordable EV platforms that balance performance and range while catering to the needs of their expanding electric vehicle user base.

Leading companies shaping the Global EV Platform Market include Ford, Tesla, Toyota, Volkswagen, BMW, General Motors, and Volvo. To reinforce their market position, companies in the EV platform sector are prioritizing a mix of strategic investments and partnerships. OEMs are heavily investing in R&D to develop modular platforms that support a wide range of vehicle sizes and functions, while ensuring compatibility with emerging software-driven technologies. Automakers are also collaborating with battery producers and tech firms to create integrated ecosystems for connectivity, charging, and autonomy. Furthermore, many are adopting vertical integration models to control key components such as motors, controllers, and battery packs, which enhances performance and cost control. These strategies help ensure scalability, adaptability, and long-term competitiveness in the evolving EV landscape.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Regional

2.2.2 Propulsion

2.2.3 Vehicle

2.2.4 Platform

2.2.5 Component

2.2.6 Sales Channel

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Component suppliers

3.1.3 Platform developers

3.1.4 Manufacturers

3.1.5 Distribution channel

3.1.6 End users

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Surge in global electric vehicle adoption

3.2.1.2 Advancements in battery technology

3.2.1.3 OEM shift to modular EV architectures

3.2.1.4 Expansion of EV charging infrastructure

3.2.2 Industry pitfalls and challenges

3.2.2.1 High initial investment in EV platforms

3.2.2.2 Underdeveloped infrastructure in emerging regions

3.2.3 Market opportunities

3.2.3.1 Growth in EV-as-a-service (EVaaS) models

3.2.3.2 Integration with autonomous & connected tech

3.2.3.3 Electrification of commercial fleets

3.2.3.4 Rising demand for urban micro-mobility solutions

3.3 Regulatory landscape

3.3.1 North America

3.3.2 Europe

3.3.3 Asia Pacific

3.3.4 Latin America

3.3.5 Middle East & Africa

3.4 Porter’s analysis

3.5 PESTEL analysis

3.6 Technology and Innovation landscape

3.6.1 Current technological trends

3.6.2 Emerging technologies

3.7 Patent analysis

3.8 Price Trend

3.8.1 By region

3.8.2 By Vehicle

3.9 Profit margin analysis

3.10 Cost breakdown analysis

3.10.1 Raw material cost components

3.10.2 Manufacturing and machinery costs

3.10.3 Logistics and distribution costs

3.10.4 Labor and assembly costs

3.10.5 R&D and testing costs

3.11 EV platform market evolution and maturity analysis

3.11.1 Historical development from ICE adaptations to dedicated platforms