Power Sports Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1801901

리서치사:Global Market Insights Inc.

발행일:2025년 08월

페이지 정보:영문 310 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

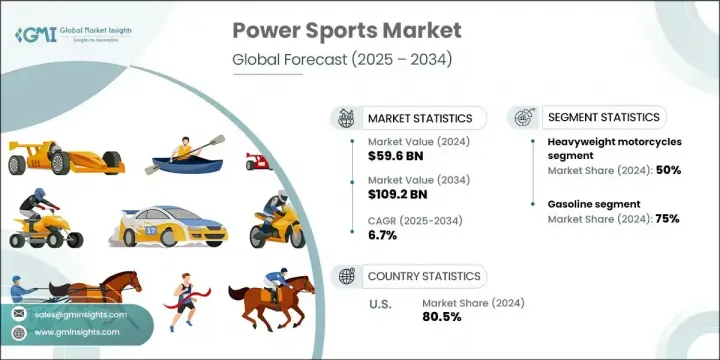

파워 스포츠 세계 시장 규모는 2024년에 596억 달러로 평가되었고, CAGR 6.7%로 성장하여 2034년까지는 1,092억 달러에 이를 것으로 추정됩니다.

이 시장은 오토바이, 개인용 수상레저기구, ATV, 스노우모빌과 같은 레크리에이션 및 성능 지향적 이동수단에 대한 소비자의 열정이 지속적으로 증가함에 따라 지속적인 모멘텀을 목격하고 있습니다. 가처분 소득 증가, 야외 레크리에이션 트렌드 확대, 모험을 기반으로 한 활동에 대한 문화적 관심 증가는 이러한 탈것의 채택을 촉진하고 있습니다. 배기가스 배출량을 줄이고 지속가능한 모빌리티를 실현하기 위한 전 세계적인 노력에 힘입어 전기차와 하이브리드 모델의 보급이 성장을 더욱 촉진하고 있습니다.

또한, 번들 서비스 제공과 금융 옵션이 주요 가치 창출 동력이 되고 있습니다. 유지보수, 로드사이드 어시스턴스, 유연한 결제 모델과 같은 지원 기능을 갖춘 풀 서비스 소유 경험을 제공하는 방향으로의 전환은 고객 참여와 브랜드 충성도를 높이고 있습니다. 인도, 일본, 중국 등 일부 아시아 시장에서는 인프라에 대한 지속적인 투자와 무역 자유화가 새로운 수요와 제조 가능성을 창출하고 있습니다. 또한, 국경 간 물류 강화, 공급망 현지화, 규제 혜택으로 인해 신흥 시장과 기존 시장에서 새로운 성장 채널이 열리고 있습니다.

시장 범위

개시 연도

2024년

예측 연도

2025-2034년

개시 금액

596억 달러

예측 금액

1,092억 달러

CAGR

6.7%

헤비급 오토바이 분야는 2034년까지 연평균 복합 성장률(CAGR) 6.9%로 성장할 것입니다. 헤비급 모터사이클의 매력은 고성능, 편안한 승차감, 상징적인 디자인으로 숙련된 라이더와 투어링 애호가들이 선호하는 선택이 되고 있습니다. 라이딩 커뮤니티의 인기와 브랜드 중심의 충성심은 이 부문을 지속적으로 강화하고 있습니다. 이 카테고리는 북미, 유럽, 아시아태평양의 특정 국가에서 특히 우위를 점하고 있으며, 프리미엄 모델의 전기 모델 채택이 더욱 촉진되고 있습니다.

2024년에는 가솔린 자동차 부문이 75%의 점유율을 차지할 것으로 예상되며, 2034년까지 연평균 복합 성장률(CAGR) 6.7%를 보일 것으로 예측됩니다. 이 부문은 우수한 출력 공급, 보급형 급유 인프라, 성능의 신뢰성으로 인해 계속해서 선두를 달리고 있습니다. 라이더는 오토바이, 사이드 바이 사이드, ATV, 스노우모빌 등 모든 차량 카테고리에서 가솔린 엔진을 선택합니다. 강력한 가속력, 긴 항속거리, 빠른 연료 보급의 장점으로 인해 특히 외딴 지역에서 성능이 요구되는 레크리에이션 및 전문적 용도에 적합합니다.

미국 파워스포츠 시장은 2024년 208억 달러 규모로 80.5%의 점유율을 차지했습니다. 이 나라는 아웃도어 및 모터스포츠 활동의 오랜 문화와 오프로드 주행 및 투어링에 대한 탄탄한 인프라가 결합되어 높은 가치를 지닌 시장입니다. 미국은 다양한 유형의 차량 생산과 소비의 중심지가 되었습니다. 미국은 또한 맞춤형, 애프터마켓 강화, 국방, 임업, 농업 등 산업에서 실용적인 목적의 파워 스포츠 차량 사용에서도 선두를 달리고 있습니다.

세계 파워스포츠 시장에 영향을 미치는 주요 기업으로는 Yamaha, Honda, BMW Motor, Suzuki Motor, CFMOTO, Kawasaki, KTM, Harley-Davidson, Polaris, BRP 등이 있습니다. 파워스포츠 업계의 주요 기업들은 자동차 전동화 혁신, 세계 유통 확대, 제품 라인의 다양화를 통해 경쟁력을 강화하고 있습니다. 각 브랜드는 관련성을 유지하기 위해 환경과 소비자 선호도 변화에 맞추어 전기 모델과 커넥티드 기능에 대한 노력을 가속화하고 있습니다. 또한, 많은 제조업체들이 보험, 유지보수, 로드사이드 지원을 포함하는 구독 서비스 및 번들 패키지를 도입하여 고객 유지를 강화하고 있습니다. 현지 생산과 딜러망을 통한 신흥 시장 진출도 최우선 과제입니다. 연구개발에 대한 전략적 투자는 모터스포츠 스폰서십과 라이더 커뮤니티를 통한 브랜딩과 함께 시장에서의 입지를 더욱 공고히 하고 있습니다.

목차

제1장 조사 방법

시장 범위와 정의

조사 디자인

조사 접근

데이터 수집 방법

데이터 마이닝 소스

지역/국가

기본 추정과 계산

기준연도 계산

시장 예측 주요 동향

1차 조사와 검증

1차 정보

예측 모델

조사 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

업계 생태계 분석

공급업체 상황

이익률 분석

부가가치 매핑

제조 부가가치와 브랜드 프리미엄

테크놀러지 통합과 혁신 가치

서비스와 애프터마켓 가치 창조

밸류체인에 대한 영향요인

기술 혁신과 전력화 영향

공급망 회복탄력성와 지역 목표 다양화

규제 준수와 환경기준

생태계 혼란

플랫폼 기반 비즈니스 모델과 디지털 변혁

수직통합 동향과 공급망 재구성

신규 진출의 위협과 시장 발전

업계에 대한 영향요인

성장 촉진요인

전략적 과제와 업계 제약

시장 기회 평가

성장 가능성 분석

제품 부문 성장 비교

시장 성숙도 평가와 수명주기 포지셔닝

성장 단계 부문

성숙 단계 부문

경쟁도이 성장 가능성에 미치는 영향

무역 플로우 분석

주요 생산국(2023년-2024년)

UTV 및 ATV

스노모빌

퍼스널 워터 크라프트(PWC)

중량급 오토바이(500cc 이상)

소비 상위국(2023년-2024년)

UTV 및 ATV

스노모빌

퍼스널 워터 크라프트(PWC)

중량급 오토바이(500cc 이상)

무역 플로우 분석

UTV 및 ATV 무역 플로우

스노모빌 무역 플로우

PWC 무역 플로우

대형 오토바이(500cc 이상) 무역 플로우

부문 고유 테이블

지속가능성 통합

수명주기 평가(LCA)와 비교 영향

ICE vs. 전기자동차 파워 스포츠

제조 단계

경쟁 벤치마킹

ROI와 비즈니스 사례

비용 절감

규제 리스크 경감

장벽과 기회

장벽

기회

정책, 투자자, 시장 성장 촉진요인

폴리시

투자자 압력

시장

베스트 프랙티스 및 사례 연구

수명주기 평가 표(ICE vs. 전기자동차)

제안

베스트 프랙티스, 사례 연구, ROI

베스트 프랙티스 및 사례 연구

Polaris (UTV/ATV, Snowmobile)

Yamaha (All segments)

BRP (Can-Am, Sea-Doo, Ski-Doo)

Harley-Davidson (Heavyweight MC)

ROI와 비즈니스 사례

전력화

폐기물 감축 및 순환성

규제 및 컴플라이언스

시장 및 투자자 가치

주요 장벽과 전략적 추천 사항

비용 내역 분석

UTV

ATV

스노모빌

퍼스널 워터 크라프트(PWC)

대형 오토바이(500cc 이상)

탄소 영향 평가(2023년-2024년)

규제 준수

부문별 성과와 갭

탄소 감축 전략

실용적인 추천 사항

규제 상황

북미

환경보호국(EPA) 배출 기준

소비자 제품 안전 위원회(CPSC) 안전기준

미국 도로 교통안전 국(NHTSA) 오토바이 기준

미국 연안경비대 퍼스널 워터 크라프트 규제

유럽

규칙(EU) 제168호에 근거한 형 식 승인 제도/2013

유로 5개 배출 가스 기준

안전 요건과 첨단시스템

소음 규제

레크리에이션 용선박 지침

아시아태평양

지역 조화 대처

시장 접근과 컴플라이언스 요건

라틴아메리카

규제 구조 진화

중동 및 아프리카

규제 개발

컴플라이언스 비용 분석과 전략적 영향

정량적인 컴플라이언스 비용 평가

전략적 시장 접근에 대한 영향

가격 동향 분석

지역적인 가격 동향

지역 재정 기회

지역적인 가격변동

시장 개척 가격 결정

가격 탄력성과 감도 분석

부문 사이 수요 탄력성

소득 탄력성과 경제 요인

경쟁적인 가격 동향

가격 결정력 분포

제조업체 가격통제

딜러 가격 결정 유연성

공급망 가격 압력

Porter의 Five Forces 분석

PESTEL 분석

향후 시장 발전

시나리오 계획과 동향 외삽

기본 시나리오 : 착실한 전동화와 시장 성장(2025년-2034년)

가속적 변혁 시나리오 : 급속한 전동화와 디지털 통합(2025년-2030년)

유지보수적인 진화 시나리오 : 단계적인 변화와 시장 통합(2025년-2034년)

기술 궤도에 대한 영향

전동화 기술 진화

자율주행 및 커넥티드카 기술

첨단 재료와 제조 기술

시장 구조 변혁

비즈니스 모델 진화

경쟁 구도 재구축

지역 목표 시장 개척

소비자 행동과 인구통계 진화

세대 교대 영향

체험 중시 소비

지속가능성과 환경 통합

탄소 중립에의 이치

순환형 경제 통합

전략적 의미와 향후 포지셔닝

테크놀러지 투자 우선순위

시장 포지셔닝 전략

기술 및 혁신 상황

현재 기술 패러다임

신기술에 의한 혼란

혁신 사이클 분석

연구개발 투자 패턴과 강도

테크놀러지 도입 장벽과 촉진요인

혁신 에코시스템 개발

기술 궤도에 대한 영향

전동화 기술 진화

접속성과 디지털 서비스 진화

전략적 혁신에 대한 영향

테크놀러지 투자 우선순위

경쟁력 있는 기술 포지셔닝

특허 분석

혁신 핫스팟과 지적재산 집중

특허절벽 분석과 그 영향

R&D 투자 패턴과 특허 상관관계

기술 분야 특허 분석

전략적 특허 정보 의미

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

인수합병(M&A)

파트너십 및 협업

신제품 발매

확장 계획과 자금조달

제5장 시장 추산·예측 : 차량별, 2021년-2034년

주요 동향

Side By Side Vehicle

ATV

중량급 오토바이

퍼스널 워터 크라프트

스노모빌

제6장 시장 추산·예측 : 추진력별, 2021년-2034년

주요 동향

가솔린

디젤

전기

제7장 시장 추산·예측 : 용도별, 2021년-2034년

주요 동향

레크리에이션

Side By Side Vehicle

ATV

중량급 오토바이

퍼스널 워터 크라프트

스노모빌

유틸리티

Side By Side Vehicle

ATV

중량급 오토바이

퍼스널 워터 크라프트

스노모빌

상업용

Side By Side Vehicle

ATV

중량급 오토바이

퍼스널 워터 크라프트

스노모빌

스포츠

Side By Side Vehicle

ATV

중량급 오토바이

퍼스널 워터 크라프트

스노모빌

Side By Side Vehicle

ATV

중량급 오토바이

퍼스널 워터 크라프트

스노모빌

건설

Side By Side Vehicle

ATV

중량급 오토바이

퍼스널 워터 크라프트

스노모빌

방위

Side By Side Vehicle

ATV

중량급 오토바이

퍼스널 워터 크라프트

스노모빌

제8장 시장 추산·예측 : 지역별, 2021년-2034년

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

러시아

북유럽 국가

아시아태평양

중국

인도

일본

호주

한국

동남아시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카공화국

사우디아라비아

아랍에미리트(UAE)

제9장 기업 개요

세계 기업-

Honda Motor Company

Yamaha Motor Company

Polaris Industries

BRP(Bombardier Recreational Products)

Harley-Davidson

Kawasaki Heavy Industries

Suzuki Motor Corporation

BMW Motorrad

KTM AG

지역 기업

Arctic Cat

CFMOTO

Ducati Motor Holding

Hisun Motors

John Deere

Kubota Corporation

KYMCO

Mahindra &Mahindra

Piaggio Group

Toro Company

Triumph Motorcycles

LSH

영문 목차

영문목차

The Global Power Sports Market was valued at USD 59.6 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 109.2 billion by 2034. This market is witnessing sustained momentum as consumer enthusiasm for recreational and performance-oriented vehicles like motorcycles, personal watercraft, ATVs, and snowmobiles continues to grow. Rising disposable income, expanding outdoor recreational trends, and a broader cultural interest in adventure-based activities are encouraging the adoption of these vehicles. Increasing traction of electric and hybrid power sports models is further supporting growth, driven by global efforts to cut emissions and implement sustainable mobility.

On top of that, bundled service offerings and financing options are becoming a major value driver. The shift toward delivering full-service ownership experiences with support features like maintenance, roadside assistance, and flexible payment models is adding to customer engagement and brand loyalty. In several Asian markets such as India, Japan, and China, continued investment in infrastructure and trade liberalization is creating fresh demand and manufacturing potential. Additionally, enhanced cross-border logistics, supply chain localization, and regulatory incentives are opening new growth channels across emerging and established markets alike.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$59.6 Billion

Forecast Value

$109.2 Billion

CAGR

6.7%

The heavyweight motorcycles segment will grow at a CAGR of 6.9% through 2034. Their appeal stems from their high-performance capabilities, extended ride comfort, and iconic design, making them a preferred option for experienced riders and touring enthusiasts. The popularity of riding communities and brand-centric loyalty continues to strengthen this segment. This category is particularly dominant across North America, Europe, and selected Asia-Pacific countries, further propelled by the adoption of electric variants among premium models.

In 2024, the gasoline-powered vehicles segment held 75% share and is projected to grow at a CAGR of 6.7% during 2034. The segment continues to lead due to its superior power delivery, widespread fueling infrastructure, and performance reliability. Riders opt for gasoline engines across all vehicle categories-including motorcycles, side-by-sides, ATVs, and snowmobiles-especially in regions where access to charging networks remains limited. Their strong acceleration, greater range, and quick refueling advantage make them especially viable for remote, performance-demanding recreational and professional applications.

United States Power Sports Market generated USD 20.8 billion and held 80.5% share in 2024. The country's long-standing culture of outdoor and motorsport activity, coupled with a robust infrastructure for off-road riding and touring, makes it a high-value market. It serves as a central hub for both manufacturing and consumption across a variety of vehicle types. The U.S. also leads in customization, aftermarket enhancements, and usage of power sports vehicles for utility purposes in industries such as defense, forestry, and agriculture.

Key players influencing the Global Power Sports Market include Yamaha, Honda, BMW Motorrad, Suzuki Motor, CFMOTO, Kawasaki, KTM, Harley-Davidson, Polaris, and BRP. Leading companies in the power sports industry are enhancing their competitive edge through innovation in vehicle electrification, expanded global distribution, and diversified product lines. To maintain relevance, brands are accelerating their push into electric models and connected features to align with shifting environmental and consumer preferences. Additionally, many manufacturers are introducing subscription services and bundled packages covering insurance, maintenance, and roadside support to boost customer retention. Expansion into emerging markets through localized production and dealer networks is also a top priority. Strategic investments in R&D, along with branding through motorsports sponsorships and rider communities, are further solidifying their market foothold.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Regional

2.2.2 Vehicle

2.2.3 Propulsion

2.2.4 Application

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Value addition mapping

3.1.3.1 Manufacturing value addition and brand premium

3.1.3.2 Technology integration and innovation value

3.1.3.3 Service and aftermarket value creation

3.1.4 Value chain impact factors

3.1.4.1 Technology disruption and electrification impact

3.1.4.2 Supply chain resilience and geographic diversification

3.1.4.3 Regulatory compliance and environmental standards

3.1.5 Ecosystem disruptions

3.1.5.1 Platform-based business models and digital transformation

3.1.5.2 Vertical integration trends and supply chain reconfiguration

3.1.5.3 New entrant threats and market evolution

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Demographic transformation and generational shift

3.2.1.2 Outdoor recreation participation surge

3.2.1.3 Electrification and technology innovation

3.2.1.4 Economic and infrastructure development

3.2.2 Strategic challenges & industry restraints

3.2.2.1 Economic pressures and market volatility

3.2.2.2 Regulatory compliance burden

3.2.2.3 Trade and tariff pressures

3.2.2.4 Market structure and distribution challenges

3.2.3 Market opportunity assessment

3.2.3.1 Electric vehicle market expansion

3.2.3.2 Military and government sector expansion

3.2.3.3 International market penetration

3.2.3.4 Technology integration and connected services

3.3 Growth potential analysis

3.3.1 Application growth potential ranking

3.3.1.1 Top-ranked growth applications

3.3.2 Product segment growth comparison

3.3.3 Market maturity assessment and lifecycle positioning

3.3.3.1 Growth stage segments

3.3.3.2 Mature stage segments

3.3.4 Competitive intensity impact on growth potential