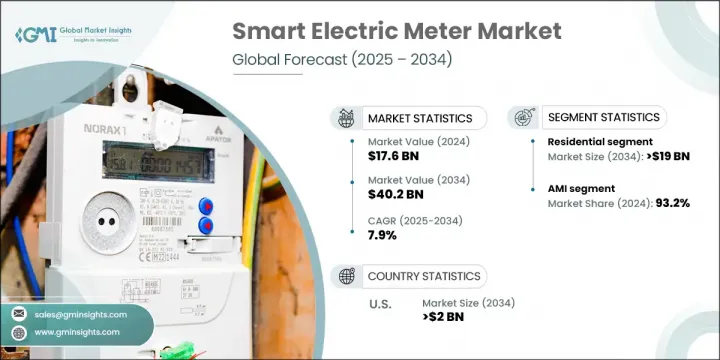

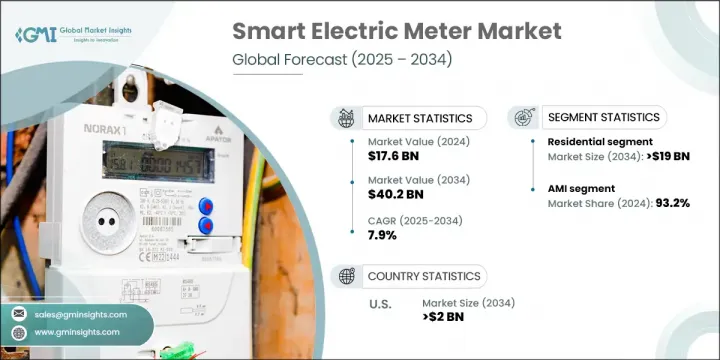

세계의 스마트 전기 미터 시장은 2024년에는 176억 달러로 평가되었고, CAGR 7.9%로 성장하여 2034년에는 402억 달러에 이를 것으로 추정되고 있습니다.

이러한 성장은 첨단 그리드 기술에 대한 전 세계 투자 증가로 인해 크게 촉진되고 있습니다. 각국이 노후화된 전력 인프라를 현대화하고, 정전을 줄이고, 재생에너지의 통합을 지원하기 위해 노력하고 있는 가운데, 스마트 미터는 이러한 최신 시스템의 핵심 구성 요소로 자리 잡고 있습니다. 이 계량기는 전력회사에 세밀한 소비 데이터를 제공하여 전력망 효율을 최적화하고, 서비스 문제를 실시간으로 파악하며, 전체 운영 비용을 절감하는 데 도움이 됩니다.

IoT, 무선 기술, 데이터 분석의 끊임없는 기술 혁신은 스마트미터의 가격과 성능을 향상시키고 있습니다. 소비자들은 현재 에너지 사용에 대한 실시간 통찰력을 통해 더 나은 수요 관리, 에너지 비용 절감, 그리드 밸런싱 지원 강화 등 다양한 혜택을 누리고 있습니다. 스마트 미터는 홈 오토메이션 및 수요응답 플랫폼과 함께 채택되어 현대 에너지 생태계에서 그 역할을 더욱 강화하고 있습니다. 이산화탄소 배출량 감축이 시급한 상황에서 이러한 장비는 효율적인 전력 분배를 가능하게 하고 청정 에너지를 촉진하는 데 중요한 역할을 할 수 있습니다. 재정적 인센티브, 정책적 의무화, 전력회사 주도의 전개로 세계 각지에서 도입이 가속화되고 있으며, 시장 전반의 상황을 강화시키고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 개시 금액 | 176억 달러 |

| 예측 금액 | 402억 달러 |

| CAGR | 7.9% |

주택 부문은 개인 주택 및 공동주택의 스마트 미터기 수요 증가로 인해 2034년까지 190억 달러에 달할 것으로 예측됩니다. 에너지 효율성, 태양에너지 통합, 정확한 청구에 대한 강조가 이 부문 확대의 주요 요인으로 작용하고 있습니다. 특히 주거 공간에서 태양광 발전 설치가 증가함에 따라 스마트 미터는 에너지 모니터링을 간소화하고 사용자가 데이터에 기반한 소비 결정을 내릴 수 있도록 도와줍니다. 전력회사들도 고객과의 소통을 강화하고, 지역 전체에서 높아지는 지속가능성 목표에 대응하기 위해 스마트미터 설치를 늘리고 있습니다.

기술적으로 시장은 고급 계측 인프라(AMI)와 자동 검침(AMR)으로 나뉩니다. AMI 부문은 2024년 93.2%의 점유율을 차지하며 양방향 통신, 실시간 데이터 전송, 유틸리티 관리 시스템과의 원활한 통합을 제공할 수 있는 AMI 부문이 계속해서 선두를 달리고 있습니다. AMR이 효율성을 개선하고 인적 오류를 줄이는 반면, AMI는 에너지 네트워크의 완전한 디지털 전환을 가능하게 하고 에너지 흐름의 제어를 강화합니다.

미국 스마트 전기 계량기 시장은 2034년까지 20억 달러에 달할 것으로 예상되며, 증가하는 재생에너지 투입을 관리하기 위해 최신 그리드 시스템을 필요로 하는 진화하는 규제에 의해 뒷받침될 것으로 예측됩니다. 세계에서 가장 정교한 경제 국가 중 하나인 미국은 세계 무역에서 중요한 역할을 하고 있으며, 이는 이러한 계량기와 같은 스마트 그리드 기술의 개발 및 보급에도 영향을 미치고 있습니다. 특히 전기자동차의 보급과 재생에너지의 통합이 진행되고 있는 주에서는 안정적인 전력 공급을 위한 움직임이 보다 광범위한 계량기 설치에 박차를 가하고 있습니다.

세계 스마트 전기 계량기 시장을 적극적으로 형성하고 있는 주요 기업으로는 지멘스, 랜디스+기어, 슈나이더 일렉트릭, 허니웰 인터내셔널, 이트론 등이 있습니다. 스마트 전기 계량기 산업의 주요 기업들은 유틸리티 사업자와의 제휴 및 스마트 그리드 프로젝트를 통해 지리적 범위 확대에 주력하고 있습니다. 기업들은 경쟁력을 유지하기 위해 AI, 엣지 컴퓨팅, IoT 기능을 통합하고 계량기의 정확성, 연결성, 기능성을 향상시키기 위해 연구개발에 많은 투자를 하고 있습니다. 또한, 지역적 컴플라이언스 및 그리드 인프라와의 상호운용성을 위한 커스터마이징도 우선순위의 핵심입니다. 이트론이나 슈나이더 일렉트릭과 같은 진출기업들은 실시간 모니터링과 디지털 그리드 관리 수요를 충족시키기 위해 AMI 기반 솔루션을 우선시하고 있습니다. 전략적 인수, 정부 기관과의 장기 계약, 재생에너지 개발 참여는 시장 진출기업의 입지를 더욱 공고히 하고 있습니다. 또한, 기업들은 유틸리티 사업자와 최종 소비자의 신뢰를 구축하기 위해 사이버 보안과 데이터 프라이버시를 중요시하고 있습니다.

The Global Smart Electric Meter Market was valued at USD 17.6 billion in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 40.2 billion by 2034. This growth is largely propelled by increasing global investments in advanced grid technologies. As nations work to modernize outdated power infrastructure, reduce blackouts, and support renewable integration, smart meters are becoming a core component of these modern systems. These meters provide utilities with granular consumption data that helps optimize grid efficiency, identify service issues in real time, and lower overall operating expenses.

Continuous innovation in IoT, wireless technology, and data analytics is improving the affordability and performance of smart meters. Consumers now benefit from real-time insights into energy usage, leading to better demand management, reduced energy costs, and greater support for grid balancing. Smart meters are also being adopted alongside home automation and demand-response platforms, further increasing their role in modern energy ecosystems. As the urgency to cut carbon emissions grows, these devices are becoming instrumental in enabling efficient power distribution and promoting cleaner energy. Financial incentives, policy mandates, and utility-driven rollouts continue to accelerate adoption across global regions, reinforcing the overall smart electric meter market landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $17.6 Billion |

| Forecast Value | $40.2 Billion |

| CAGR | 7.9% |

The residential sector will reach USD 19 billion by 2034, driven by the rising demand for smart meters in individual homes and multifamily dwellings. Increasing emphasis on energy efficiency, solar energy integration, and accurate billing are major factors behind this segment's expansion. As solar PV installations rise, particularly in residential spaces, smart meters help streamline energy monitoring and allow users to make data-driven consumption decisions. Utilities are also increasingly installing smart meters to enhance communication with customers and meet growing sustainability goals across neighborhoods.

Technologically, the market is split into advanced metering infrastructure (AMI) and automatic meter reading (AMR). The AMI segment held a 93.2% share in 2024 and continues to lead due to its ability to provide two-way communication, real-time data transmission, and seamless integration with utility management systems. While AMR improves efficiency and reduces human error, AMI enables full digital transformation of energy networks and enhances control over energy flows.

United States Smart Electric Meter Market will reach USD 2 billion by 2034, supported by evolving regulations that require modern grid systems to manage growing renewable energy inputs. With one of the world's most sophisticated economies, the US plays a major role in global trade, which also influences the development and deployment of smart grid technologies like these meters. The push for stable power delivery, especially in states with rising electric vehicle adoption and renewable integration, is driving broader meter installations.

Key players actively shaping the Global Smart Electric Meter Market include Siemens, Landis + Gyr, Schneider Electric, Honeywell International, and Itron. Leading companies in the smart electric meter industry are focusing on expanding their geographic reach through partnerships with utility providers and smart grid projects. Firms are investing heavily in R&D to enhance the accuracy, connectivity, and functionality of their meters, integrating AI, edge computing, and IoT capabilities to stay competitive. Customization for regional compliance and interoperability with grid infrastructure is also a core priority. Players like Itron and Schneider Electric are prioritizing AMI-based solutions to cater to demand for real-time monitoring and digital grid management. Strategic acquisitions, long-term contracts with government bodies, and participation in renewable energy rollouts are further strengthening market positions. Additionally, businesses are emphasizing cybersecurity and data privacy to build trust among utilities and end consumers.