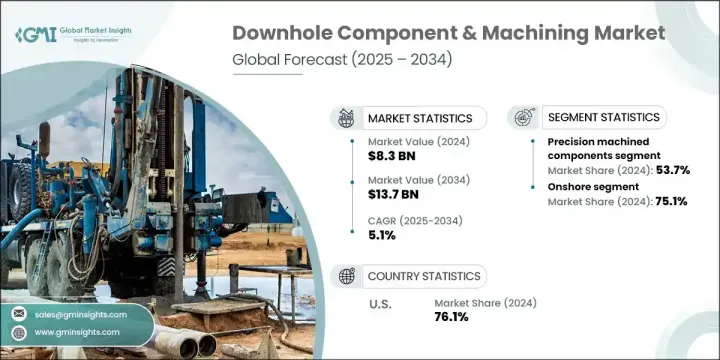

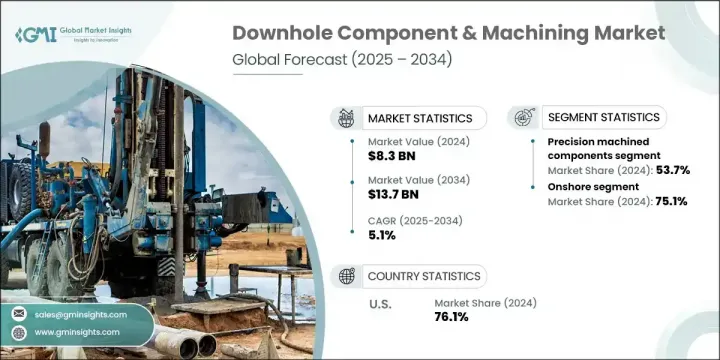

세계의 다운홀 부품 및 가공 시장은 2024년 83억 달러로 평가되었으며 CAGR 5.1%로 성장할 전망이며 2034년에는 137억 달러에 이를 것으로 추정됩니다.

석유 및 가스 기업들이 더 깊고 가혹한 저류층 환경으로 확대됨에 따라 고내구성 소재에 대한 수요가 지속적으로 증가하고 있습니다. 초합금, 고성능 세라믹, 복합 재료로 제작된 부품들은 강도, 내식성, 극한 온도에서의 안정성 덕분에 점점 더 필수적입니다. 동시에, 산업계의 증강 석유 회수 및 비전통적 시추에 주력하는 것은 첨단 유량 제어 및 통합 센싱과 같은 극도의 정밀 기능을 가능케 하는 정교하게 가공된 부품에 대한 수요를 촉진하고 있습니다.

다운홀 장비는 스마트 기술 도입으로 급속히 진화하고 있습니다. 정밀 가공 기술은 오늘날의 극한 시추 환경에서 요구되는 더 엄격한 공차로 복잡한 형상을 생산할 수 있게 합니다. 최근 유전은 밸브, 모터, 완결 시스템 같은 부품에 지능형 센서를 내장함으로써 사전 예방적 운영으로 전환하고 있습니다. 이러한 센서는 압력, 온도, 진동, 유체 조성 등 핵심 지표를 실시간으로 추적하여 장비 고장을 방지하고 시추 성능을 최적화하는 예측적 인사이트를 제공합니다. 이러한 디지털 전환은 기업이 자산을 관리하고 운영 연속성을 유지하는 방식을 재편하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 83억 달러 |

| 예측 금액 | 137억 달러 |

| CAGR | 5.1% |

정밀 가공 부문은 2024년 53.7%의 점유율을 기록했으며, 2034년까지 연평균 4.5% 성장할 것으로 예상됩니다. 센서 및 모니터링 장비의 사용 증가는 극한 운영 조건 하에서 지속적인 성능 데이터에 대한 업계의 증가하는 수요와 직결됩니다. 유량, 압력, 저류층 행동과 같은 핵심 성과 지표는 생산 효율성, 장비 안전성, 자원 최적화와 관련된 의사 결정을 안내합니다. 운영사들은 장기간 시추 주기 동안 일관된 성능을 제공하는 고정밀 내구성 센서 통합 부품이 필요합니다.

육상 부문은 장주기 유정 설계, 다단계 파쇄 수요, 부식성 유체 등 견고한 정밀 제조 부품이 필수인 요인들로 2024년 62억 달러 규모를 기록했습니다. 이러한 환경은 스마트 센서와 통합 분석 플랫폼을 통한 디지털화도 빠르게 도입 중입니다. 유량, 압력, 온도에 대한 실시간 인사이트는 원격 자산 관리, 예측 유지보수, 공정 최적화를 지원하여 운영 효율성을 높이고 계획되지 않은 가동 중단을 줄입니다.

유럽의 다운홀 부품 및 가공 시장은 2024년 14억 달러 규모로 평가되었습니다. 이 지역의 에너지 전환 및 자동화에 주력함에 따라 석유·가스 장비 미래 진화에 중추적인 역할을 하고 있습니다. 성숙한 해양 유전이 최대 효율을 요구하고 육상 운영이 현대화를 추진함에 따라, 장수명 센서 탑재 부품의 채택이 지속적으로 증가하고 있습니다. 개입 효율성, 자동화 모니터링, 디지털 통합 분야의 혁신은 지역 전망을 형성하고 장기 성장 잠재력을 촉진하고 있습니다.

세계의 다운홀 부품 및 가공 시장의 경쟁 환경을 형성하는 주요 기업으로는 Weatherford, SLB, Halliburton, Saipem, Baker Hughes 등이 있습니다. 다운홀 부품 및 가공 시장의 주요 업체들은 경쟁력 강화를 위해 혁신, 자동화, 소재 발전에 주력하고 있습니다. 선도 기업들은 열악한 환경에서 향상된 내열성과 내식성을 갖춘 향후 소재 개발을 위해 연구개발(R&D)에 막대한 투자를 진행 중입니다.

또한 기업들은 초정밀 공차의 부품을 제조하기 위해 CNC 및 다축 시스템과 같은 정밀 가공 기술을 도입하고 있습니다. 유전 서비스 제공업체 및 디지털 솔루션 제공업체와의 전략적 협력을 통해 IoT 및 센서 기술을 다운홀 도구에 더 폭넓게 통합하고 있습니다. 많은 기업들은 신속한 납품과 맞춤화를 지원하기 위해 지역별 제조 거점과 서비스 네트워크도 확대되고 있습니다. 이러한 전략은 시추 작업 전반에 걸쳐 운영 위험을 줄이고 고객 가치를 높이는 동시에 고성능, 내구성, 지능형 부품을 제공하기 위한 것입니다.

The Global Downhole Component & Machining Market was valued at USD 8.3 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 13.7 billion by 2034. As oil & gas companies expand into deeper and harsher reservoir environments, the demand for highly durable materials continues to surge. Components made from superalloys, high-performance ceramics, and composite materials are increasingly essential due to their strength, resistance to corrosion, and stability under extreme temperatures. At the same time, the industry's focus on enhanced oil recovery and unconventional drilling is driving the need for intricately machined parts with extreme precision-enabling functions such as advanced flow control and integrated sensing.

Downhole equipment is evolving rapidly with the adoption of smart technologies. Precision machining techniques now enable the production of complex geometries with tighter tolerances needed in today's extreme drilling scenarios. Modern oilfields are shifting toward proactive operations by embedding intelligent sensors in components like valves, motors, and completion systems. These sensors enable real-time tracking of vital metrics, including pressure, temperature, vibration, and fluid makeup, providing predictive insights that help avoid equipment failures and optimize drilling performance. This digital shift is reshaping how companies manage assets and maintain operational continuity.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.3 Billion |

| Forecast Value | $13.7 Billion |

| CAGR | 5.1% |

The precision-machined segment held a 53.7% share in 2024 and is expected to grow at a CAGR of 4.5% through 2034. The rising use of sensors and monitoring instruments is tied to the industry's increasing need for continuous performance data under extreme operational conditions. Key performance indicators such as flow rates, pressure, and reservoir behavior guide decisions around production efficiency, equipment safety, and resource optimization. Operators require highly accurate and durable sensor-integrated parts that deliver consistent performance over long drilling cycles.

The onshore segment generated USD 6.2 billion in 2024, driven by long-cycle well designs, multi-stage fracturing demands, and corrosive fluids-all of which require ruggedized, precision-manufactured components. These environments are also rapidly embracing digitalization through smart sensors and integrated analytics platforms. Real-time insights into flow, pressure, and temperature support remote asset management, predictive maintenance, and process optimization, enhancing operational efficiency while reducing unplanned downtime.

Europe Downhole Component & Machining Market was valued at USD 1.4 billion in 2024. The region's focus on energy transition and automation is playing a pivotal role in the evolution of its oil and gas equipment landscape. As mature offshore fields demand maximum efficiency and onshore operations push for modernization, the adoption of long-life, sensor-enabled components continues to rise. Innovations in intervention efficiency, automated monitoring, and digital integration are shaping the regional outlook and fueling long-term growth potential.

The leading companies shaping the competitive landscape in the Global Downhole Component & Machining Market include Weatherford, SLB, Halliburton, Saipem, and Baker Hughes. Major players in the Downhole Component & Machining Market are focusing on innovation, automation, and material advancement to strengthen their competitive position. Leading firms are investing heavily in R&D to develop next-generation materials with improved thermal and corrosion resistance for hostile environments.

In addition, companies are adopting precision machining technologies such as CNC and multi-axis systems to manufacture components with ultra-tight tolerances. Strategic collaborations with oilfield service providers and digital solution providers are enabling broader integration of IoT and sensor technologies into downhole tools. Many firms are also expanding their regional manufacturing bases and service networks to support rapid delivery and customization. These strategies aim to deliver high-performance, durable, and intelligent components while reducing operational risks and increasing client value across drilling operations.