글루텐 프리 밀가루 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)

Gluten Free Flour Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1801859

리서치사:Global Market Insights Inc.

발행일:2025년 08월

페이지 정보:영문 190 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

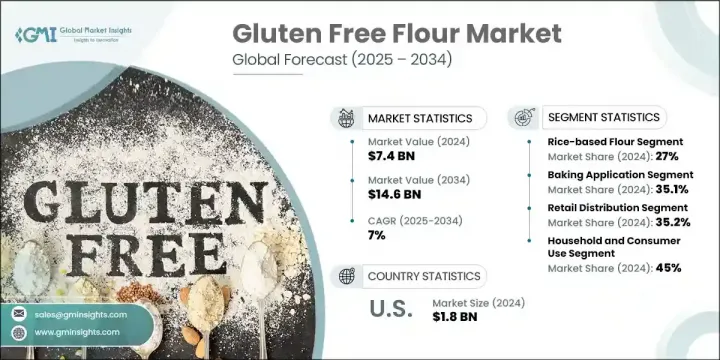

세계의 글루텐 프리 밀가루 시장 규모는 2024년에 74억 달러에 달하고, CAGR 7%로 성장할 전망이며 2034년에는 146억 달러에 이를 것으로 추정됩니다.

이러한 성장은 글루텐 민감성에 대한 소비자 인식 증가와 함께 웰빙 및 체중 조절에 주력하는 식이 동향으로의 광범위한 전환에 힘입은 것입니다. 의학적 진단을 받은 경우든 단순히 건강을 중시하는 경우든, 글루텐 함유 곡물 대체품을 찾는 사람들이 늘어남에 따라 콩류, 씨앗, 콩, 곡물, 견과류에서 추출한 밀가루에 대한 수요가 지속적으로 증가하고 있습니다. 식물성 식단과 클린 라벨 식단의 인기가 이러한 성장을 뒷받침하고 있습니다.

진단된 글루텐 관련 장애가 없더라도 많은 소비자들이 소화 및 웰빙에 도움이 된다고 인식하여 글루텐 프리 밀가루 제품을 선택하고 있습니다. 가정용 베이커부터 대규모 상업 식품 생산자에 이르기까지, 글루텐 프리 밀가루 제품의 매력은 시장 전반에 걸쳐 혁신과 확장을 촉진하고 있습니다. 북미는 잘 구축된 유통망, 높아진 소비자 인식, 글루텐 프리 라이프스타일의 광범위한 채택으로 인해 이 시장의 선두 주자 위치를 공고히 하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

74억 달러

예측 금액

146억 달러

CAGR

7%

2024년 기준 쌀가루 부문이 27%의 점유율을 기록했으며, 2034년까지 연평균 7.3% 성장할 전망입니다. 쌀가루는 부드러운 풍미, 경제성, 다양한 레시피 적용 가능성으로 특히 인기가 높습니다. 베이킹과 조리 시 밀가루의 실용적인 대체재 역할을 하여 글루텐 프리 밀가루 부문의 필수품으로 자리매김했습니다. 다양한 전분과 글루텐 프리 곡물 또는 콩류를 혼합한 블렌드 및 특수 밀가루도 점차 주목받고 있습니다. 이러한 혼합 제품은 전통적인 밀 기반 밀가루의 탄력성과 질감을 재현하도록 설계되어 글루텐 프리 베이커리 제품에 대한 소비자의 맛과 품질 기대를 충족시킵니다.

2024년 기준 베이킹 부문이 35.1%의 점유율을 기록했습니다. 쿠키, 케이크, 빵, 머핀, 페이스트리 등의 베이커리 제품이 글루텐 프리 밀가루의 주요 이용 사례로 자리매김하고 있습니다. 이러한 우위는 셀리악병 진단 증가와 건강을 중시하는 소비자들의 관심 확대와 연관이 있습니다. 밀가루 배합 및 결합제 분야의 기술적 발전으로 글루텐 프리 베이킹 제품의 질감, 외관, 맛이 상당하게 개선되어 더 넓은 소비자층을 끌어모으며 시장 확장을 지속하고 있습니다.

미국의 글루텐 프리 밀가루 시장은 2024년 18억 달러 규모를 기록했으며, 2034년까지 연평균 성장률(CAGR) 5.9%로 성장할 전망입니다. 미국 시장의 성장은 영양에 대한 공공의 관심 증대, 글루텐 관련 건강 진단 사례의 상당한 급증, 그리고 원재료 투명성과 알레르기 유발 성분 없는 식품에 대한 움직임에서 비롯됩니다. 더 많은 소비자들이 밀가루의 건강한 대체재를 적극적으로 찾으면서 미국 내 수요는 계속 증가하고 있으며, 이는 전 세계 글루텐 프리 밀가루 시장에서 가장 역동적이고 중요한 지역 중 하나로 자리매김하게 했습니다.

세계의 글루텐 프리 밀가루 시장을 형성하는 유명한 기업으로는 Bob's Red Mill Natural Foods, Ancient Harvest(Quinoa Corporation), Archer Daniels Midland Company(ADM), Arrowhead Mills(Hain Celestial Group), General Mills Inc., Enjoy Life Foods, Cargill Inc. 등이 있습니다. 전 세계 글루텐 프리 밀가루 시장 내 주요 기업들은 시장 점유율을 유지하고 확대하기 위해 혁신, 파트너십, 제품 다각화를 병행하고 있습니다. 많은 기업들이 진화하는 소비자 선호도를 반영하기 위해 고대 곡물과 고단백 재료를 도입하여 글루텐 프리 제품군을 확대되고 있습니다. 고급 제분 및 혼합 기술에 대한 투자는 제품의 일관성과 확장성 향상에 기여합니다. 브랜드들은 또한 건강을 중시하는 구매자들을 유치하기 위해 클린 라벨 인증, 매력적인 포장, 맞춤형 마케팅에 주력하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 산업 고찰

생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

산업에 미치는 영향요인

성장 촉진요인

셀리악병 유병률 및 인식 증가

프리미엄 및 수제 식품 시장 성장

건강 및 웰빙 트렌드 채택

클린 라벨 및 천연 제품 수요

산업의 잠재적 리스크 및 과제

생산 및 원자재 비용 상승

제한된 유통 기한 및 저장 문제

시장 기회

고대 곡물 및 슈퍼푸드 통합

단백질 강화 밀가루 개발

기능성 성분 강화

신흥 시장 진출

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

밀가루 유형별

장래 시장 동향

기술과 혁신의 상황

현재의 기술 동향

신흥기술

특허 상황

무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

주요 수입국

주요 수출국

지속가능성과 환경 측면

지속 가능한 사례

폐기물 감축 전략

생산의 에너지 효율

친환경 활동

탄소발자국 고려 사항

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

합병과 인수

파트너십 및 협업

신제품 발매

확대 계획

제5장 시장 추정 및 예측 : 밀가루 유형별(2021-2034년)

주요 동향

쌀가루

백미 가루

현미 가루

찹쌀 가루

특수 쌀가루

견과류와 씨앗 가루

아몬드 가루

코코넛 가루

기타 견과류 가루

종자 가루

근채와 괴경의 분말

카사바 가루

감자 가루

기타 뿌리채소 가루

고대 곡물 가루

키누아 가루

아마란서스 가루

테프 가루

기장 가루

콩류와 콩가루

병아리 콩가루

렌즈 콩가루

기타 콩가루

옥수수 기반 밀가루

콘플라워(마사할리나)

옥수수 밀

옥수수 전분

특수 밀가루와 블렌드 밀가루

멀티 그레인 블렌드

베이킹 믹스 블렌드

단백질 강화 블렌드

기능성 성분 블렌드

제6장 시장 추정 및 예측 : 용도별(2021-2034년)

주요 동향

베이킹 용도

빵과 베이커리 제품

케이크와 패스트리

쿠키와 비스킷

피자와 플랫 브레드

조리 및 요리용

농축 및 코팅

파스타 및 면 제조

아침식사용

상업용 식품 제조

포장 베어커리 제품

냉동 식품 용도

스낵 식품 제조

푸드서비스 용도

레스토랑 및 베이커리 사용

시설 내 푸드서비스

케이터링 및 이벤트

제7장 시장 추정 및 예측 : 유통 채널별(2021-2034년)

주요 동향

소매 유통

슈퍼마켓 및 대형 슈퍼마켓

건강식품 및 전문점

편의점

온라인과 전자상거래

주요 전자상거래 플랫폼

소비자 직접 유통 채널

모바일 상거래

도매와 B2B 유통

식품 도매업체

산업 및 상업 판매

대체 유통 채널

농산물 시장 및 지역 판매

협동조합 및 구매그룹

대량 및 창고 판매

수출 및 국제 무역

제8장 시장 추정 및 예측 : 최종 이용 산업별(2021-2034년)

주요 동향

가정용 및 소비자용

홈 베이킹 애호가

건강을 중시하는 가정

셀리악병 및 글루텐 민감성 가정

요리 애호가 및 요리사

상업 식품 제조

제빵 제품 제조업체

스낵 식품 제조업체

냉동 식품 회사

아침식사용 시리얼 제조업체

푸드서비스 산업

레스토랑 및 카페

베이커리 및 제과점

피자와 패스트 푸드 체인

케이터링 및 이벤트 서비스

시설 내 푸드서비스

학교와 교육기관

의료시설

기업 카페테리아

노인 커뮤니티

산업용도

반려동물 식품 제조

영양보조식품의 제조

의약품 용도

화장품 및 퍼스널케어

제9장 시장 추정 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제10장 기업 프로파일

Ancient Harvest(Quinoa Corporation)

Anthony's Goods

Archer Daniels Midland Company

Arrowhead Mills(Hain Celestial Group)

Authentic Foods

Bob's Red Mill Natural Foods

Cargill Inc.

Doves Farm Foods

Enjoy Life Foods(Mondelez International)

Firebird Artisan Mills

General Mills Inc.

Giusto's Specialty Foods

Great River Organic Milling

Hodgson Mill

Honeyville Food Products

Ingredion Incorporated

King Arthur Baking Company

Maida Place Mills

Nutiva

Pamela's Products

Shipton Mill Ltd.

Terrasoul Superfoods

HBR

영문 목차

영문목차

The Global Gluten Free Flour Market was valued at USD 7.4 billion in 2024 and is estimated to grow at a CAGR of 7% to reach USD 14.6 billion by 2034. This expansion is fueled by increasing consumer awareness about gluten sensitivity, as well as a broader shift toward healthier eating habits and dietary trends focused on wellness and weight control. As more individuals-whether medically diagnosed or simply health-conscious-seek alternatives to gluten-containing grains, demand for flour derived from legumes, seeds, beans, grains, and nuts continues to rise. The growth is supported by the popularity of plant-based and clean-label diets.

Many consumers are opting for gluten-free flour options due to perceived digestive and wellness benefits, even in the absence of diagnosed gluten-related disorders. From home bakers to large-scale commercial food producers, the appeal of gluten-free flour products is driving innovation and expansion across the market. North America remains at the forefront due to its well-established retail networks, heightened consumer awareness, and widespread adoption of gluten-free lifestyles, all of which help reinforce its leadership in this space.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$7.4 Billion

Forecast Value

$14.6 Billion

CAGR

7%

In 2024, the rice-based flour segment held the largest share, holding 27% and will grow at a CAGR of 7.3% through 2034. Rice flour is especially popular due to its mild flavor, affordability, and adaptability in a wide variety of recipes. It serves as a practical substitute for wheat flour in baking and cooking, making it a staple in the gluten-free flour sector. Blended and specialty flours, which combine various starches and gluten-free grains or legumes, are also gaining traction. These blends are engineered to replicate the elasticity and texture of traditional wheat-based flours, meeting consumer expectations for taste and quality in gluten-free baked goods.

The baking segment held a 35.1% share in 2024. Baked goods such as cookies, cakes, breads, muffins, and pastries continue to be the leading use case for gluten-free flour. This dominance is linked to the increasing diagnosis of celiac disease and growing interest among health-focused consumers. Technological advancements in flour formulations and binding agents have significantly improved the texture, appearance, and taste of gluten-free baked items, attracting a broader audience and supporting ongoing market expansion.

United States Gluten Free Flour Market generated USD 1.8 billion in 2024 and is projected to grow at a CAGR of 5.9% by 2034. The growth of the U.S. market stems from heightened public interest in nutrition, a significant rise in gluten-related health diagnoses, and a movement toward ingredient transparency and allergen-free foods. With more consumers actively searching for healthier substitutes to wheat flour, demand in the U.S. continues to climb, making it one of the most dynamic and vital regions in the global gluten-free flour space.

Prominent companies shaping the Global Gluten Free Flour Market include Bob's Red Mill Natural Foods, Ancient Harvest (Quinoa Corporation), Archer Daniels Midland Company (ADM), Arrowhead Mills (Hain Celestial Group), General Mills Inc., Enjoy Life Foods, and Cargill Inc. To maintain and grow their market share, companies within the gluten-free flour industry are employing a mix of innovation, partnerships, and product diversification. Many are expanding their gluten-free offerings by incorporating ancient grains and high-protein ingredients to cater to evolving consumer preferences. Investments in advanced milling and blending technologies help improve product consistency and scalability. Brands are also focusing on clean-label certifications, appealing packaging, and tailored marketing to appeal to health-conscious buyers.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Flour type

2.2.3 Application

2.2.4 Distribution channel

2.2.5 End use industry

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising celiac disease prevalence and awareness.

3.2.1.2 Premium and artisanal food market growth.

3.2.1.3 Health and wellness trend adoption.

3.2.1.4 Clean label and natural product demand.

3.2.2 Industry pitfalls and challenges

3.2.2.1 Higher production and raw material costs.

3.2.2.2 Limited shelf life and storage issues.

3.2.3 Market opportunities

3.2.3.1 Ancient grains and superfood integration

3.2.3.2 Protein-enriched flour development

3.2.3.3 Functional ingredient fortification

3.2.3.4 Emerging market penetration

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter’s analysis

3.6 PESTEL analysis

3.6.1 Technology and Innovation landscape

3.6.2 Current technological trends

3.6.3 Emerging technologies

3.7 Price trends

3.7.1 By region

3.7.2 By flour type

3.8 Future market trends

3.9 Technology and Innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Flour Type, 2021-2034 (USD Million & Kilo Tons)

5.1 Key Trends

5.2 Rice-based flours

5.2.1 White rice flour

5.2.2 Brown rice flour

5.2.3 Sweet rice flour

5.2.4 Specialty rice flour

5.3 Nut and seed flours

5.3.1 Almond flour

5.3.2 Coconut flour

5.3.3 Other nut flours

5.3.4 Seed flours

5.4 Root vegetable and tuber flours

5.4.1 Cassava flour

5.4.2 Potato flour

5.4.3 Other root vegetable flours

5.5 Ancient grain flours

5.5.1 Quinoa flour

5.5.2 Amaranth flour

5.5.3 Teff flour

5.5.4 Millet flour

5.6 Legume and bean flours

5.6.1 Chickpea flour

5.6.2 Lentil flour

5.6.3 Other bean flours

5.7 Corn-based flours

5.7.1 Corn flour (masa harina)

5.7.2 Cornmeal

5.7.3 Corn starch

5.8 Specialty and blend flours

5.8.1 Multi-grain blends

5.8.2 Baking mix blends

5.8.3 Protein-enhanced blends

5.8.4 Functional ingredient blends

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million & Kilo Tons)

6.1 Key trends

6.2 Baking application

6.2.1 Bread and loaf products

6.2.2 Cakes and pastries

6.2.3 Cookies and biscuits

6.2.4 Pizza and flatbreads

6.3 Cooking and culinary applications

6.3.1 Thickening and coating

6.3.2 Pasta and noodle making

6.4 Breakfast applications

6.4.1 Commercial food manufacturing

6.4.2 Packaged baked goods

6.4.3 Frozen food application

6.4.4 Snack food manufacturing

6.5 Foodservice applications

6.5.1 Restaurant and bakery use

6.5.2 Institutional foodservice

6.5.3 Catering and events

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Million & Kilo Tons)

7.1 Key Trends

7.2 Retail distribution

7.2.1 Supermarkets & hypermarkets

7.2.2 Health food and specialty stores

7.2.3 Convenience stores

7.3 Online and e-commerce

7.3.1 Major e-commerce platforms

7.3.2 Direct-to-consumer channels

7.3.3 Mobile commerce

7.4 Wholesale and b2b distribution

7.4.1 Food distributors

7.4.2 Industrial and commercial sales

7.5 Alternative distribution channels

7.5.1 Farmers markets and local sales

7.5.2 Co-op and buying groups

7.5.3 Bulk and warehouse sales

7.5.4 Export and international trade

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Million & Kilo Tons)

8.1 Key Trends

8.2 Household and consumer use

8.2.1 Home baking enthusiasts

8.2.2 Health-conscious families

8.2.3 Celiac and gluten-sensitive households

8.2.4 Culinary hobbyists and chefs

8.3 Commercial food manufacturing

8.3.1 Baked goods manufacturers

8.3.2 Snack food producers

8.3.3 Frozen food companies

8.3.4 Breakfast cereal manufacturers

8.4 Foodservice industry

8.4.1 Restaurants and cafes

8.4.2 Bakeries and patisseries

8.4.3 Pizza and fast food chains

8.4.4 Catering and event services

8.5 Institutional foodservice

8.5.1 Schools and educational institutions

8.5.2 Healthcare facilities

8.5.3 Corporate cafeterias

8.5.4 Senior living communities

8.6 Industrial applications

8.6.1 Pet food manufacturing

8.6.2 Nutritional supplement production

8.6.3 Pharmaceutical applications

8.6.4 Cosmetic and personal care

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Kilo Tons)

9.1 Key trends

9.2 North America

9.2.1 U.S.

9.2.2 Canada

9.3 Europe

9.3.1 Germany

9.3.2 UK

9.3.3 France

9.3.4 Spain

9.3.5 Italy

9.3.6 Rest of Europe

9.4 Asia Pacific

9.4.1 China

9.4.2 India

9.4.3 Japan

9.4.4 Australia

9.4.5 South Korea

9.4.6 Rest of Asia Pacific

9.5 Latin America

9.5.1 Brazil

9.5.2 Mexico

9.5.3 Argentina

9.5.4 Rest of Latin America

9.6 Middle East and Africa

9.6.1 Saudi Arabia

9.6.2 South Africa

9.6.3 UAE

9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

10.1 Ancient Harvest (Quinoa Corporation)

10.2 Anthony's Goods

10.3 Archer Daniels Midland Company

10.4 Arrowhead Mills (Hain Celestial Group)

10.5 Authentic Foods

10.6 Bob's Red Mill Natural Foods

10.7 Cargill Inc.

10.8 Doves Farm Foods

10.9 Enjoy Life Foods (Mondelez International)

10.10 Firebird Artisan Mills

10.11 General Mills Inc.

10.12 Giusto's Specialty Foods

10.13 Great River Organic Milling

10.14 Hodgson Mill

10.15 Honeyville Food Products

10.16 Ingredion Incorporated

10.17 King Arthur Baking Company

10.18 Maida Place Mills

10.19 Nutiva

10.20 Pamela's Products

10.21 Shipton Mill Ltd.

10.22 Terrasoul Superfoods

(주)글로벌인포메이션02-2025-2992kr-info@giikorea.co.kr ⓒ Copyright Global Information, Inc. All rights reserved.