Cargo Drones Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1801848

리서치사:Global Market Insights Inc.

발행일:2025년 08월

페이지 정보:영문 185 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

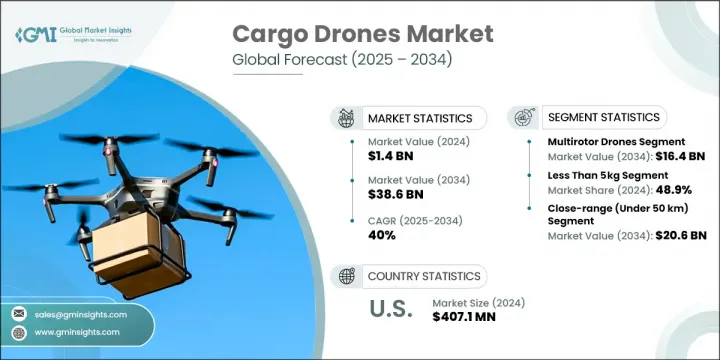

세계의 화물 드론 시장 규모는 2024년에 14억 달러에 달하고, CAGR 40%로 성장할 전망이며 2034년에는 386억 달러에 이를 것으로 추정됩니다.

이러한 성장은 주로 드론 네트워크 서비스(DNaaS) 모델의 확산, 급성장하는 전자상거래 산업, 그리고 라스트마일 물류의 중요성 증대에 촉진된 것입니다. 전자상거래 활동이 확대됨에 따라 빠르고 비용 효율적이며 자동화된 배송 시스템의 필요성이 필수적입니다. 화물 드론은 낮은 운영 비용과 최소한의 지상 기반 인프라로 빠른 서비스를 제공하는 효율적인 대안으로 부상했습니다. 단거리 노선과 라스트마일 배송을 지원할 수 있는 능력은 진화하는 물류 생태계에서 핵심 구성 요소로 자리매김하게 합니다. 범용 도킹 및 충전 시스템의 도입은 드론 운영을 간소화하고 크로스 플랫폼 호환성을 향상시키고 있습니다. 주요 산업 단체들의 통합 표준 도입 노력은 상업 물류 분야에서의 대규모 채택과 효율적인 전개를 위한 길을 더욱 넓히고 있습니다.

멀티로터 드론 부문은 수직 이착륙 능력과 도시 운영에서의 기동성으로 2034년까지 164억 달러의 시장 규모를 기록할 전망입니다. 이러한 드론은 정밀성, 기동성, 최소 공간 활용이 필수적인 밀집된 도시 환경에 특히 적합합니다. 시장 침투율을 높이기 위해 제조사들은 배터리 기술 발전과 무게 경량화를 통해 비행 시간 최적화와 탑재량 증대에 주력하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

14억 달러

예측 금액

386억 달러

CAGR

40%

2024년 기준 5kg 미만 적재량 부문이 48.9%의 점유율을 기록했습니다. 특히 의료 및 온라인 소매 분야에서 소형 소포 배송 수요가 증가하면서 이 부문의 성장세가 가속화되고 있습니다. 규제 장벽과 정교한 추진 시스템의 필요성에도 불구하고, 고성능을 제공하는 소형 드론에 대한 수요가 높습니다. 해당 분야의 기업들은 더 빠르고 효율적인 라스트마일 서비스에 대한 기대를 충족시키기 위해 신뢰성 있고 기동성 있는 드론 개발을 최우선 과제로 삼고 있습니다.

캐나다의 화물 드론 시장은 2025-2034년에 걸쳐 CAGR 38.1%로 성장할 전망입니다. 외딴 지역 및 접근이 어려운 지역의 물류적 한계를 극복하기 위한 정부 프로그램이 이러한 성장에 상당한 기여를 하고 있습니다. 유리한 정책과 시범 사업이 지속적으로 추진됨에 따라, 최종 배송 공급망, 자원 배분 및 의료 물류 분야에서 드론 사용이 증가하는 추세입니다.

세계의 화물 드론 시장을 형성하는 주요 기업으로는 Elroy Air, Sabrewing Aircraft Company, Natilus, Silent Arrow, Dronamics 등이 있습니다. 화물 드론 시장의 선도 업체들은 시장 지위를 공고히 하기 위해 여러 전략적 접근 방식을 채택하고 있습니다. 많은 업체들이 고급 소재를 통해 드론의 적재량 증대, 비행 지속 시간 연장, 무게 감소를 위해 연구개발(R&D)에 막대한 투자를 하고 있습니다. 물류 기업 및 정부 기관과의 협력과 파트너십을 통해 실제 현장 전개와 규제 승인을 경화 촉진제로 가속화하고 있습니다. 기업들은 또한 드론 인프라 네트워크 구축과 최적화된 경로 계획을 위한 인공지능(AI) 통합에 주력하고 있습니다. 더불어 여러 업체들은 신뢰 구축과 운영 범위 확대를 위해 항공 당국의 인증 획득을 추진 중입니다. 전략적 지역적 확장, 특히 외딴 지역 및 서비스 미달 지역 진출과 확장 가능한 드론 서비스 플랫폼(DNaaS)에 대한 투자는 장기적 가치 확보와 지속적인 성장을 보장하기 위한 핵심 전략으로 부상하고 있습니다.

목차

제1장 조사 방법

시장의 범위와 정의

조사 디자인

조사 접근

데이터 수집 방법

데이터 마이닝 소스

세계

지역/국가

기본 추정과 계산

기준연도 계산

시장 예측의 주요 동향

1차 조사와 검증

1차 정보

예측 모델

조사의 전제와 한계

제2장 주요 요약

제3장 산업 고찰

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

산업에 미치는 영향요인

성장 촉진요인

드론 네트워크 서비스(DNaaS) 모델의 등장

전자상거래 및 라스트마일 물류 확대대

지원적 규제 발전 및 무인항공기(UAV) 정책

무인 물류의 군사 및 방위 분야 용도

외딴 지역 및 접근이 어려운 지역의 접근성 개선 필요성

산업의 잠재적 리스크 및 과제

규제 불확실성과 공역 제한

제한된 적재량 및 비행 거리

시장 기회

외딴 지역 물류 수요 증가

스마트 시티 및 도심 항공 모빌리티 프로그램과의 통합

BVLOS 운영을 위한 AI 및 자율성 고급 발전

해양 및 산업 공급망에서의 용도

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현재의 기술 동향

신흥기술

새로운 비즈니스 모델

규정 준수 요건

국방예산 분석

세계의 방위비 동향

지역 방위 예산 배분

북미

유럽

아시아태평양

중동 및 아프리카

라틴아메리카

주요 방위 현대화 프로그램

예산 예측(2025-2034년)

산업의 성장에 미치는 영향

국가별 방위 예산

공급 체인의 탄력

지정학적 분석

인재 분석

디지털 변혁

합병, 인수, 전략적 파트너십의 상황

위험 평가 및 관리

주요 계약 체결(2021-2024년)

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 진출기업의 경쟁 벤치마킹

재무실적의 비교

수익

이익률

연구개발

제품 포트폴리오 비교

제품 라인업의 넓이

기술

혁신

지리적 존재의 비교

세계 실적 분석

서비스 네트워크의 범위

지역에 의한 시장 침투율

경쟁 포지셔닝 매트릭스

선도 기업

도전자

팔로워

틈새 진출기업

전략적 전망 매트릭스

주요 개발(2021-2024년)년

합병과 인수

파트너십 및 협업

기술 발전

확대 및 투자 전략

지속가능성에 대한 노력

디지털 변혁의 대처

신흥기업/스타트업기업경쟁 구도

제5장 시장 추정 및 예측 : 드론 유형별(2021-2034년)

주요 동향

고정익 드론

멀티로터 드론

하이브리드 드론

제6장 시장 추정 및 예측 : 적재량별(2021-2034년)

주요 동향

5kg 미만

5-20kg

20-50kg

50kg 초과

제7장 시장 추정 및 예측 : 범위별(2021-2034년)

주요 동향

근거리(50km 미만)

단거리(50-149km)

중거리(150-650km)

장거리(650km 초과)

제8장 시장 추정 및 예측 : 기술별(2021-2034년)

주요 동향

자율형 드론

원격조작 드론

제9장 시장 추정 및 예측 : 용도별(2021-2034년)

주요 동향

헬스케어와 응급 서비스

의료용품의 배달

혈액과 장기의 운송

긴급 대응과 재해 구호

기타

소매업 및 전자상거래

마지막 마일 배송

허브간 화물 운송

창고 이송 업무

기타

방위와 안보

야전 보급

국경 경비대의 물류

재해 피난 지원

기타

농업

인프라와 건설

기타

제10장 시장 추정 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

네덜란드

아시아태평양

중국

인도

일본

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제11장 기업 프로파일

세계 주요 기업

Natilus

DRONAMICS

Sabrewing Aircraft Company

Elroy Air

Silent Arrow

지역별 주요 기업

북미

DroneUp

Flirtey

UPS Flight Forward

Zipline International

유럽

Wingcopter

Manna Aero

FlyingBasket

아시아태평양

Chengdu JOUAV Automation Tech

SZ DJI Technology

Throttle Aerospace Systems

틈새 진출기업/혁신 기업

Skye Air Mobility

H3 Dynamics Holdings

Matternet

Wing Aviation

UAVOS

HBR

영문 목차

영문목차

The Global Cargo Drones Market was valued at USD 1.4 billion in 2024 and is estimated to grow at a CAGR of 40% to reach USD 38.6 billion by 2034. This growth is largely driven by the increasing adoption of drone-network-as-a-service (DNaaS) models, a booming e-commerce industry, and the growing importance of last-mile logistics. As e-commerce activities escalate, the need for fast, cost-effective, and automated delivery systems becomes essential. Cargo drones have emerged as an efficient alternative, offering fast service with low operating costs and requiring minimal ground-based infrastructure. Their ability to support short-haul routes and last-mile delivery positions them as a crucial component in the evolving logistics ecosystem. The introduction of universal docking and charging systems is streamlining drone operations and enhancing cross-platform compatibility. Efforts from key industry groups to introduce unified standards are further paving the way for wider-scale adoption and streamlined deployment in commercial logistics.

The multirotor drones segment will generate USD 16.4 billion by 2034 due to their vertical takeoff and landing capabilities and agility in urban operations. These drones are particularly well-suited for dense city environments where precision, maneuverability, and minimal space usage are vital. To increase market penetration, manufacturers are focusing on optimizing flight duration and enhancing payload capacity by advancing battery technologies and minimizing drone weight.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$1.4 Billion

Forecast Value

$38.6 Billion

CAGR

40%

In 2024, the less than 5 kg payload segment held 48.9% share. The growing demand for small parcel deliveries, especially in healthcare and online retail sectors, is fueling the momentum of this segment. Despite regulatory hurdles and the need for more sophisticated propulsion systems, compact drones delivering high performance are in demand. Companies in this space are prioritizing the development of reliable and agile drones to meet expectations for faster and more efficient last-mile services.

Canada Cargo Drones Market is expected to grow at a 38.1% CAGR from 2025 to 2034. Government programs focused on overcoming logistical limitations in isolated and hard-to-reach regions are contributing significantly to this growth. The increasing use of drones in last-mile supply chains, resource distribution, and medical logistics is gaining traction as favorable policies and pilot initiatives continue to roll out.

Key companies shaping the Global Cargo Drones Market include Elroy Air, Sabrewing Aircraft Company, Natilus, Silent Arrow, and Dronamics. Leading players in the cargo drones market are adopting several strategic approaches to solidify their market position. Many are investing heavily in R&D to enhance drone payload capacity, increase flight endurance, and reduce weight through advanced materials. Collaborations and partnerships with logistics firms and government agencies are being leveraged to accelerate real-world deployment and regulatory approvals. Companies are also focusing on establishing drone infrastructure networks and integrating AI for optimized route planning. Additionally, several players are pursuing certification from aviation authorities to build trust and expand operational range. Strategic geographic expansion, particularly into remote and underserved areas, and investment in scalable DNaaS platforms are becoming key moves to capture long-term value and ensure consistent growth.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Drone type trends

2.2.2 Payload capacity trends

2.2.3 Range trends

2.2.4 Technology trends

2.2.5 End use application trends

2.2.6 Regional trends

2.3 TAM analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Emergence of drone-network-as-a-service (DNaaS) models

3.2.1.2 Expansion of e-commerce and last-mile logistics

3.2.1.3 Supportive regulatory developments and UAV policies

3.2.1.4 Military and defense applications for unmanned logistics

3.2.1.5 Need for improved access in remote and hard-to-reach areas

3.2.2 Industry pitfalls and challenges

3.2.2.1 Regulatory uncertainty and airspace restrictions

3.2.2.2 Limited payload capacity and range

3.2.3 Market opportunities

3.2.3.1 Rising demand for remote area logistics

3.2.3.2 Integration with smart city and urban air mobility programs

3.2.3.3 Advancements in AI and autonomy for BVLOS operations

3.2.3.4 Application in offshore and industrial supply chains

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter’s analysis

3.6 PESTEL analysis

3.7 Technology and Innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Emerging business models

3.9 Compliance requirements

3.10 Defense budget analysis

3.11 Global defense spending trends

3.12 Regional defense budget allocation

3.12.1 North America

3.12.2 Europe

3.12.3 Asia Pacific

3.12.4 Middle East and Africa

3.12.5 Latin America

3.13 Key defense modernization programs

3.14 Budget forecast (2025-2034)

3.14.1 Impact on industry growth

3.14.2 Defense budgets by country

3.15 Supply chain resilience

3.16 Geopolitical analysis

3.17 Workforce analysis

3.18 Digital transformation

3.19 Mergers, acquisitions, and strategic partnerships landscape

3.20 Risk assessment and management

3.21 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 Latin America

4.2.1.5 Middle East & Africa

4.3 Competitive benchmarking of key players

4.3.1 Financial performance comparison

4.3.1.1 Revenue

4.3.1.2 Profit margin

4.3.1.3 R&D

4.3.2 Product portfolio comparison

4.3.2.1 Product range breadth

4.3.2.2 Technology

4.3.2.3 Innovation

4.3.3 Geographic presence comparison

4.3.3.1 Global footprint analysis

4.3.3.2 Service network coverage

4.3.3.3 Market penetration by region

4.3.4 Competitive positioning matrix

4.3.4.1 Leaders

4.3.4.2 Challengers

4.3.4.3 Followers

4.3.4.4 Niche players

4.3.5 Strategic outlook matrix

4.4 Key developments, 2021-2024

4.4.1 Mergers and acquisitions

4.4.2 Partnerships and collaborations

4.4.3 Technological advancements

4.4.4 Expansion and investment strategies

4.4.5 Sustainability initiatives

4.4.6 Digital transformation initiatives

4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Drone Type, 2021 - 2034 (USD Million & Units)

5.1 Key trends

5.2 Fixed-wing drones

5.3 Multirotor drones

5.4 Hybrid drones

Chapter 6 Market Estimates and Forecast, By Payload Capacity, 2021 - 2034 (USD Million & Units)

6.1 Key trends

6.2 Less than 5 kg

6.3 5 kg to 20 kg

6.4 20 kg to 50 kg

6.5 Above 50 kg

Chapter 7 Market Estimates and Forecast, By Range, 2021 - 2034 (USD Million & Units)

7.1 Key trends

7.2 Close-range (under 50 km)

7.3 Short-range (50-149 km)

7.4 Mid-range (150-650 km)

7.5 Long range (more than 650 km)

Chapter 8 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Million & Units)

8.1 Key trends

8.2 Autonomous drones

8.3 Remote-controlled drones

Chapter 9 Market Estimates and Forecast, By End Use Application, 2021 - 2034 (USD Million & Units)

9.1 Key trends

9.2 Healthcare and emergency services

9.2.1 Medical supply delivery

9.2.2 Blood and organ transport

9.2.3 Emergency response and disaster relief

9.2.4 Others

9.3 Retail and e-commerce

9.3.1 Last-mile delivery

9.3.2 Inter-hub cargo transport

9.3.3 Warehouse transfer operations

9.3.4 Others

9.4 Defense and security

9.4.1 Field resupply

9.4.2 Border patrol logistics

9.4.3 Disaster evacuation support

9.4.4 Others

9.5 Agriculture

9.6 Infrastructure and construction

9.7 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million & Units)