생분해성 스마트 재료 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)

Biodegradable Smart Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1801839

리서치사:Global Market Insights Inc.

발행일:2025년 08월

페이지 정보:영문 210 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

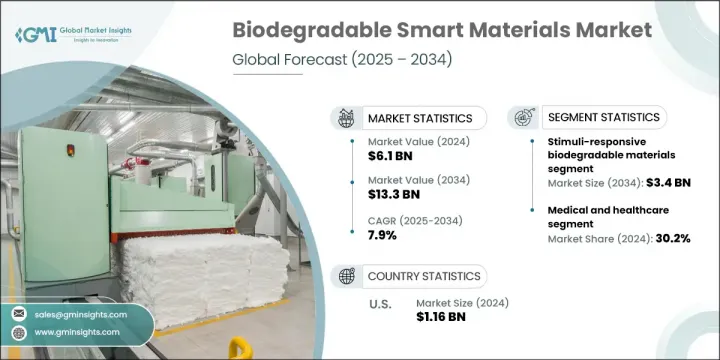

세계의 생분해성 스마트 재료 시장 규모는 2024년에 61억 달러가 되고, CAGR 7.9%로 성장할 전망이며 2034년에는 133억 달러에 이를 것으로 예측되고 있습니다.

이러한 성장은 플라스틱 오염과 전자 폐기물에 대한 전 세계적 인식 제고로 촉진되며, 이는 정부로 하여금 더 엄격한 환경 법규를 시행하도록 유도하고 있습니다. 여기에는 제품 수명 주기 의무화, 일회용 플라스틱 금지, 생산자 책임 규정 등이 포함됩니다. 소비자들의 지속가능성과 탄소 발자국에 대한 인식이 높아짐에 따라 산업계는 친환경 대체재로 관심을 전환하고 있다. 생분해성 스마트 소재는 순환경제 원칙과 환경 법규에 부합하는 유망한 해결책으로 부상 중이다. 다기능성을 갖춘 이 소재들은 성능이나 규정 준수를 저해하지 않는 실용적 대안을 제공하며 산업 전반에서 성장세를 보이고 있다.

고분자 과학, 나노기술, 생명공학 분야의 지속적인 고급 발전은 생분해성 스마트 소재 분야를 변화시키고 있습니다. 이러한 혁신은 열이나 빛과 같은 자극에 대한 반응성, 기억 및 자가 보수 특성을 포함한 향상된 성능을 지닌 스마트 생분해성 고분자의 개발을 가능하게 합니다. 그 결과, 다양한 이용 사례에 걸친 유연성과 적응성 덕분에 채택이 가속화되고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

61억 달러

예측 금액

133억 달러

CAGR

7.9%

2024년 자극 반응성 생분해성 소재 부문은 16억 달러를 기록했으며, 2034년까지 34억 달러에 달할 것으로 전망됩니다. 이 소재들의 매력은 pH, 온도, 효소, 빛과 같은 환경적 입력에 반응하여 정밀하고 시기적절한 반응을 제공하는 역동적인 능력에 있습니다. 특히 소재 반응성과 적응성이 성능과 효율성에 필수적인 스마트 패키징 및 생의학 분야에서 매우 특화된 용도 경작지로의 활용이 확대되고 있습니다.

의료 및 헬스케어 부문은 2024년 30.2%의 점유율을 기록했으며, 이는 생체적합성 소재에 대한 수요 증가가 촉진한 결과입니다. 생분해성 스마트 소재는 유독성 잔류물을 남기지 않고 안전하게 분해되어 수술적 제거가 필요 없고 부작용 위험을 최소화한다는 점에서 의료 분야에서 널리 채택되고 있습니다. 이 소재의 임플란트, 재생의학, 약물 전달 용도는 합병증 발생률을 낮추고 환자 치료 결과를 개선함으로써 임상 관행을 재편하고 있습니다.

미국의 생분해성 스마트 재료 시장 규모는 2024년에 11억 6,000만 달러로 2034년까지의 CAGR은 7.8%로 예상되고 있습니다. 이 지역의 수요는 환경 의식의 확산에 크게 힘입고 있습니다. 미국 소비자들은 지속 가능한 제품을 점점 더 선호하며, 기업들이 생분해성 솔루션으로 전환하도록 압박하고 있습니다. 이러한 수요는 제품 개발과 혁신의 핵심 촉진 요인이 되어 시장 확장에 유리한 조건을 조성하고 있습니다.

생분해성 스마트 재료 시장을 독점하는 주요 기업은 BASF SE, Novamont SpA, NatureWorks LLC, Covestro AG, Evonik Industries AG 등입니다. 생분해성 스마트 소재 시장의 업체들은 시장 지위를 강화하기 위해 여러 핵심 전략을 활용하고 있습니다. 자극 반응성 및 메모리 기능 통합 등 소재 기능성 향상을 위해 R&D 투자를 확대되고 있습니다. 연구 기관 및 기술 기업과의 협력을 통해 혁신 주기를 가속화하고 있습니다. 또한 기업들은 용도 기반을 확대하기 위해 포장, 의료, 소비재 기업들과 전략적 파트너십을 구축하고 있습니다. 많은 기업들이 증가하는 수요를 충족시키기 위해 생산 능력을 확대하는 동시에 생물 기반 원료를 통합하여 석유 기반 원료에 대한 의존도를 낮추고 있습니다. 더불어 기업들은 친환경 라벨링 및 지속가능성 인증을 통해 소비자와 최종 사용자를 교육하여 제품 채택과 브랜드 신뢰도를 높이는 데 주력하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

업계의 잠재적 위험 및 과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

장래 시장 동향

기술과 혁신의 상황

현재의 기술 동향

신흥기술

특허 상황

무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

주요 수입국

주요 수출국

지속가능성과 환경 측면

지속가능한 관행

폐기물 감축 전략

생산의 에너지 효율

환경 친화적인 노력

탄소발자국 고려 사항

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병과 인수

파트너십 및 협업

신제품 발매

확장 계획

제5장 시장 규모와 예측 : 재료 유형별(2021-2034년)

주요 동향

형상 기억 생분해성 재료

열 반응성 형상 기억 폴리머

pH 반응성 및 화학적으로 유도되는 시스템

자기 반응성 형상 기억 재료

다자극 반응 형상 기억 시스템

자기 수복성 생분해성 재료

본질적인 자기 복구 폴리머 시스템

외인성 자기 복구 및 마이크로 캡슐 시스템

생물에 착상을 얻은 자기 치유 메커니즘

가역성과 반복성을 갖춘 자기 복구 재료

자극 반응성 생분해성 재료

온도 반응성 및 열 감수성 시스템

pH 반응성 및 화학 감지 재료

광 반응성 및 광 감수성 시스템

수분 반응성 및 습도 감지 재료

전도성 생분해성 스마트 재료

전도성 폴리머 시스템

이온 전도성 및 전해질 재료

압전 재료 및 에너지 수집 재료

전자파 차폐 및 보호 재료

생물 기반 및 천연 스마트 소재

셀룰로오스 기반 스마트 머티리얼 시스템

단백질 기반 및 생체분자 스마트 재료

키토산과 해양 유래의 스마트 머티리얼

전분계 및 농업 폐기물 스마트 머티리얼

제6장 시장 규모와 예측 : 용도별(2021-2034년)

주요 동향

의료 및 헬스케어

약물전달 시스템과 제어 방출

조직 공학 및 재생 의료

의료용 임플란트 및 생체 적합성 장치

상처치유와 치료

포장 및 소비재

능동형 및 지능형 포장 시스템

식품 포장과 신선도 모니터링

의약품 포장과 의약품 보호

소비자 전자기기 포장과 보호

전자기기 및 웨어러블 디바이스

유연 및 신축성 전자 부품

웨어러블 건강 모니터링 및 감지 장치

임시 전자 문신 및 피부 패치

생분해성 센서와 환경 모니터링

농업과 환경

제어 방출 비료 및 영양소 전달

농약 살포 및 작물 보호 시스템

토양 모니터링 및 농업 감지

환경 수리 및 오염 제어

섬유 및 패션 산업

스마트 직물 및 반응형 섬유

운동복 및 퍼포먼스 웨어

의료용 섬유 및 헬스케어 원단

패션과 미적 스마트 텍스타일

제7장 시장 규모와 예측 : 최종 용도별(2021-2034년)

주요 동향

헬스케어 및 의료기기

제약 및 생명공학

의료기기 제조 업체 및 공급업체

병원 및 의료 제공자

연구기관 및 임상조직

포장 및 소비재 산업

식품 및 음료 포장

의약품 포장 제조업체

가전제품 및 기술기업

소매 및 전자상거래 조직

전자 및 기술 산업

가전 제조업체

웨어러블 기술 및 IoT 디바이스 기업

반도체 및 부품 제조업체

통신 및 네트워크 기업

농업과 환경산업

농약 및 비료회사

정밀 농업 및 기술 공급자

환경 모니터링 및 센싱 기업

정부기관 및 환경단체

조사 및 학술 기관

대학 및 학술연구센터

정부의 연구기관 및 연구기관

민간 연구 개발 기관

기술 인큐베이터와 혁신 센터

제8장 시장 규모와 예측 : 기술별(2021-2034년)

주요 동향

생물 기반 재료 기술

합성 생분해성 기술

스마트 기능 통합 기술

제조 및 가공 기술

제9장 시장 규모와 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

기타 유럽

아시아태평양

중국

인도

일본

한국

호주

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

기타 중동 및 아프리카

제10장 기업 프로파일

BASF SE

Covestro AG

Evonik Industries AG

NatureWorks LLC

Novamont SpA

Corbion

Danimer Scientific

Biome Bioplastics

Solvay

Eastman Chemical Company

HBR

영문 목차

영문목차

The Global Biodegradable Smart Materials Market was valued at USD 6.1 billion in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 13.3 billion by 2034. This growth is fueled by rising global awareness of plastic pollution and electronic waste, driving governments to impose stricter environmental laws. These include product lifecycle mandates, single-use plastic bans, and producer responsibility regulations. With consumers increasingly conscious of sustainability and their carbon footprint, industries are shifting focus toward eco-compatible alternatives. Biodegradable smart materials are emerging as a promising solution that aligns with circular economy principles and environmental legislation. Their multifunctional capabilities are gaining momentum across industries, offering practical alternatives that don't compromise performance or compliance.

Ongoing advancements in polymer science, nanotech, and bioengineering are transforming the biodegradable smart materials space. These innovations are enabling the development of smart biodegradable polymers with enhanced performance, including responsiveness to stimuli like heat or light, as well as memory and self-repair properties. As a result, adoption is accelerating due to their flexibility and adaptability across diverse use cases.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$6.1 Billion

Forecast Value

$13.3 Billion

CAGR

7.9%

In 2024, the stimuli-responsive biodegradable materials segment generated USD 1.6 billion and is forecasted to reach USD 3.4 billion by 2034. The appeal of these materials lies in their dynamic ability to react to environmental inputs like pH, temperature, enzymes, or light, delivering precise and timely responses. Their use in highly specific applications is expanding, particularly in smart packaging and biomedical fields, where material reactivity and adaptability are essential to performance and efficiency.

The medical and healthcare segment held 30.2% share in 2024, driven by a growing need for biocompatible materials. Biodegradable smart materials are widely adopted in healthcare due to their ability to safely degrade without leaving toxic residues, eliminating the need for surgical extraction and minimizing risk of adverse reactions. Their application in implants, regenerative medicine, and drug delivery is reshaping clinical practices by reducing complication rates and improving patient outcomes.

United States Biodegradable Smart Materials Market generated USD 1.16 billion in 2024 and is anticipated to register a CAGR of 7.8% through 2034. Demand in the region is heavily supported by a rising wave of environmental consciousness. American consumers are increasingly favoring sustainable products, pressuring businesses to pivot toward biodegradable solutions. This demand has become a central driver of product development and innovation, creating favorable conditions for market expansion.

Key players dominating the Biodegradable Smart Materials Market include BASF SE, Novamont S.p.A., NatureWorks LLC, Covestro AG, and Evonik Industries AG. To enhance their market position, companies in the biodegradable smart materials sector are leveraging several key strategies. They are expanding R&D investments to enhance material functionality-such as incorporating stimuli-responsiveness and memory capabilities. Collaboration with research institutions and tech firms accelerates innovation cycles. Businesses are also forging strategic partnerships with packaging, healthcare, and consumer goods companies to widen their application base. Many are scaling up manufacturing capacities to meet growing demand while integrating bio-based inputs to reduce dependency on petroleum-based feedstocks. Additionally, firms are focusing on educating consumers and End users through eco-labeling and sustainability certifications to drive adoption and brand trust.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Material type

2.2.3 Application

2.2.4 End use

2.2.5 Technology

2.3 TAM analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.2 Industry pitfalls and challenges

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter’s analysis

3.6 PESTEL analysis

3.6.1 Technology and innovation landscape

3.6.2 Current technological trends

3.6.3 Emerging technologies

3.7 Price trends

3.7.1 By region

3.8 Future market trends

3.9 Technology and innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent landscape

3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Size and Forecast, By Material Type, 2021-2034 (USD Million) (Tons)

5.1 Key trends

5.2 Shape memory biodegradable materials

5.2.1 Thermally responsive shape memory polymers

5.2.2 pH-responsive and chemically triggered systems