바이오스티뮬런트 제형 재료 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)

Biostimulants Formulation Material Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1801811

리서치사:Global Market Insights Inc.

발행일:2025년 08월

페이지 정보:영문 192 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

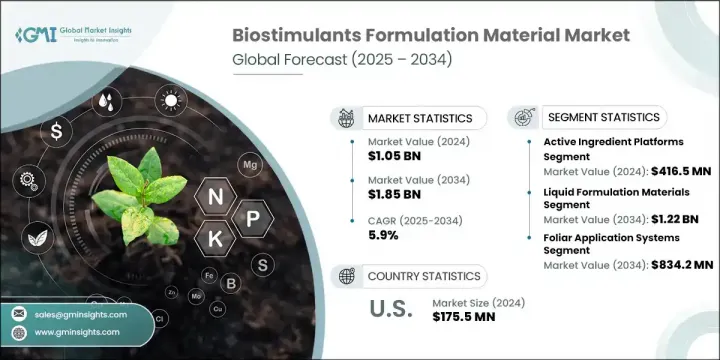

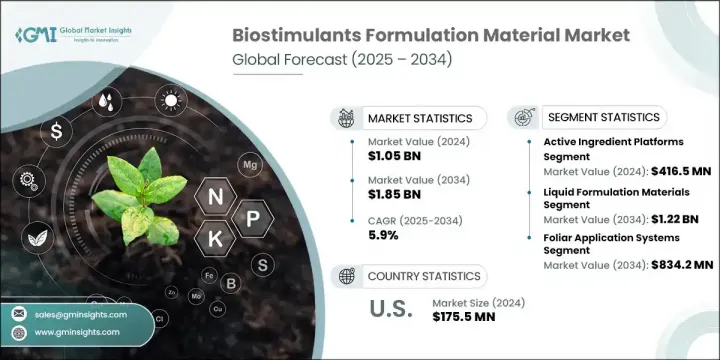

세계의 바이오스티뮬런트 제형 재료 시장 규모는 2024년에 10억 5,000만 달러가 되고, CAGR 5.9%로 성장할 전망이며, 2034년에는 18억 5,000만 달러에 달할 것으로 예측되고 있습니다.

전 세계적으로 지속 가능한 농업 관행에 대한 강조와 생산성 향상은 물론 환경 친화적인 투입재에 대한 수요 증가로 인해 시장이 상당한 주목을 받고 있습니다. 자연 기반 및 생물학적 작물 증진 솔루션으로의 광범위한 전환과 유리한 정책 환경이 시장을 확장시키고 있습니다. 엽면 살포가 전체 용도의 거의 절반을 차지하며 여전히 주요 사용 방법입니다. 그러나 표적 전달 방식의 혁신이 더욱 고급화하고 널리 보급됨에 따라 종자 처리 및 토양 적용 제형에 대한 관심이 증가하면서 산업 역학이 재편되고 있습니다.

미생물 용액, 해초 추출물, 천연 다당류 등 천연 제형 재료로의 전환이 가속화되고 있습니다. 화학 투입물 감축을 위한 규제 압박과 잔류물 없는 식품에 대한 소비자 선호가 지속 가능한 바이오스티뮬런트로의 전환을 촉진하고 있습니다. 생산자들은 최근 농업을 지원하는 생분해성, 효과적, 지속 가능한 솔루션에 초점을 맞춘 연구 개발에 자원을 집중하고 있습니다. 특정 작물 종류, 토양 조건, 지역 기후에 맞춰 고도로 맞춤화된 제형 개발이 증가하는 추세입니다. 기업들은 고급 데이터 분석과 농업학적 인사이트를 활용하여 수확량을 증대시키고 프리미엄 가격을 실현하며, 정밀하고 고부가가치 작물 솔루션을 추구하는 재배자와의 장기적 관계를 구축하는 맞춤형 바이오스티뮬런트를 제공하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

10억 5,000만 달러

예측 금액

18억 5,000만 달러

CAGR

5.9%

안정제 및 보조제 부문은 유효 성분 보존, 유통 기한 개선, 다양한 용도에서 바이오스티뮬런트의 기능적 전달 향상 능력에 힘입어 2034년까지 연평균 7.4%의 성장률을 보일 것으로 예상됩니다. 유화제 및 계면활성제를 포함한 이러한 성분들은 제형 균일성 유지, 흡수 보장, 기타 농산물과의 호환성 지원에 핵심적인 역할을 합니다. 이들의 사용 증가 추세는 현대 작물 투입물 제형에 요구되는 복잡성과 정밀도가 높아지고 있음을 보여줍니다.

건조 제형 재료 부문은 2034년까지 연평균 4.6%의 성장률을 보일 전망이다. 사용 편의성과 혁신으로 액상 제형이 부각되고 있으나, 장기간 유통기한과 안정성이 요구되는 상황에서는 건조 형태가 여전히 핵심적이다. 시장이 진화함에 따라 건조 제형 점유율은 소폭 하락할 것으로 예상되나, 특정 이용 사례에서는 수요가 꾸준히 유지될 것이다.

미국의 바이오스티뮬런트 제형 재료 시장은 80.1%의 점유율을 차지하며, 2024년에는 1억 7,550만 달러를 창출합니다. 이 지역은 잘 구축된 규제 미래, 지속적인 농업 연구개발 투자, 환경 친화적 농업 관행에 대한 강력한 추진의 혜택을 받고 있습니다. 다당류는 환경적 호환성과 효과성으로 인해 미국에서 널리 선호됩니다. 이 고도로 산업화되고 기술 중심의 시장에서는 안정제와 보조제는 제품 안정성 유지 및 다른 농약 시스템과의 호환성 확보에 필수적입니다. 미생물 접종제, 아미노산, 해초류 기반 재료와 같은 유효 성분의 주된 사용은 최근 농업에서 생물학적 제제와 정밀 투입물에 대한 선호도가 증가하고 있음을 보여줍니다.

세계의 바이오스티뮬런트 제형 재료 시장을 형성하고 있는 주요 기업으로는 Novozymes A/S, BASF SE, Valagro SpA, UPL Limited, Syngenta AG 등이 있습니다. 전 세계 바이오스티뮬런트 제형 재료 시장에서 강력한 입지를 구축하기 위해 기업들은 환경 기준을 준수하면서 수확량을 향상시키는 지속 가능한 작물별 제품 개발을 위한 연구에 막대한 투자를 하고 있습니다. 주요 초점은 혁신, 특히 다양한 기후 및 토양 조건에 적합한 생분해성 맞춤형 제형 개발에 있습니다. 농업 기술 기업, 연구 기관 및 재배자와의 전략적 협력을 통해 기업들은 지역별 맞춤형 솔루션을 공동 개발하고 있습니다. 또한 전 세계 유통망을 확대되고 신흥 시장에 진출하여 새로운 성장 영역을 개척하고 있습니다. 디지털 플랫폼과 정밀 농업 도구에 대한 강조는 제품 제공의 실시간 맞춤화를 지원합니다.

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

지속가능하고 유기적인 농업 투입재에 대한 수요 증가

친환경 작물 보호 제품에 대한 규제 지원

작물 수확량 및 품질 향상에 대한 관심 증가

제형 및 전달 시스템의 기술적 발전

업계의 잠재적 위험 및 과제

농가의 의식과 기술 지식 부족

환경 요인에 따른 제품 효능의 변동성

시장 기회

작물별 맞춤형 제형 개발

디지털 농업 및 정밀 농업과의 통합

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신 미래

현재의 기술 동향

신흥기술

가격 동향

지역별

소재 유형별

코스트 내역 분석

특허 분석

지속가능성과 환경 측면

지속가능한 관행

폐기물 감축 전략

생산 에너지 효율

친환경 이니셔티브

탄소발자국의 고려

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병과 인수

파트너십 및 협업

신제품 발매

확장계획과 자금조달

제5장 시장 추계 및 예측 : 재료 유형별(2021-2034년)

주요 동향

천연 다당류

안정제 및 보조제

유효 성분 플랫폼

해초 추출물 제형 원료

푸민산 및 플루보산 유도체

아미노산 및 단백질 가수분해 염기

미생물 캡슐화 재료

제6장 시장 추계 및 예측 : 형태별(2021-2034년)

주요 동향

액체 제형 재료

유화제 및 용해제

현탁제 및 증점제

방부제 및 항균제

동결-해동 안정제

건조 제형 재료

과립 및 펠렛화 보조제

고결 방지제 및 유동성 향상제

분진 억제 및 취급성 향상제

방습 코팅

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

종자 처리 제형 재료

코팅재 및 결합제

접착 촉진제 및 필름 형성제

착색료 및 식별 시스템

보호 밀봉재

잎면 살포 시스템

스프레이 보조제 및 침투 촉진제

비산 방지 및 침착 보조

자외선 차단제 및 안정성 증진제

탱크 혼합용 상용성제

토양 시용 재료

과립 보조제 및 결합제

서방형 코팅 시스템

토양 침투 촉진제

수분 관리 재료

기타

제8장 시장 추계 및 예측 : 작물별(2021-2034년)

주요 동향

곡물

과일 및 채소

기타

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

영국

프랑스

이탈리아

스페인

독일

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

이집트

기타 중동 및 아프리카

제10장 기업 프로파일

Ashland Global Holdings Inc.

BASF SE

Biotechnica(UK)

Citymax Group(China)

Croda International Plc

Elemental Enzymes

Evonik Industries AG

Fertinagro Biotech

Genvor

Natural Growth Biostimulants LLC

Novozymes A/S

SIPCAM Inagra(유럽)

Syngenta AG

UPL Limited

Valagro SpA

HBR

영문 목차

영문목차

The Global Biostimulants Formulation Material Market was valued at USD 1.05 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 1.85 billion by 2034. The market is gaining significant traction due to the worldwide emphasis on sustainable agricultural practices and the increasing demand for productivity-boosting yet environmentally conscious inputs. The broader shift toward nature-based and biological crop enhancement solutions, combined with favorable policy environments, is propelling market expansion. Foliar application remains the dominant method of usage, accounting for nearly half of all applications. However, growing interest in seed treatments and soil-applied formulations is reshaping industry dynamics, especially as innovation in targeted delivery methods becomes more advanced and widely available.

The transition to natural formulation materials-such as microbial solutions, seaweed extracts, and natural polysaccharides-is intensifying. Regulatory pressure to reduce chemical inputs, coupled with consumer preference for residue-free food, is accelerating this move toward sustainable biostimulants. Producers are dedicating resources to research and development focused on biodegradable, effective, and sustainable solutions that support modern agriculture. There's a growing trend toward highly tailored formulations designed for specific crop types, soil conditions, and local climates. Companies are leveraging advanced data analytics and agronomic insights to offer customized biostimulants that boost yields, command premium pricing, and foster long-term relationships with growers seeking precise, high-value crop solutions.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$1.05 Billion

Forecast Value

$1.85 Billion

CAGR

5.9%

The stabilizers and adjuvants segment will grow at a CAGR of 7.4% through 2034, supported by their ability to preserve active ingredients, improve shelf-life, and enhance the functional delivery of biostimulants across a wide range of applications. These ingredients, including emulsifiers and surfactants, play a key role in maintaining formulation uniformity, ensuring absorption, and supporting compatibility with other agricultural products. Their rising use highlights the growing complexity and precision required in today's crop input formulations.

The dry formulation materials segment will grow at a CAGR of 4.6% through 2034. While liquid formulations are becoming more prominent due to ease of use and innovation, dry forms remain critical in scenarios requiring long shelf-life and stability. As the market evolves, a slight decline in dry formulation share is anticipated, although demand will remain steady in certain use cases.

U.S. Biostimulants Formulation Material Market held 80.1% share, generating USD 175.5 million in 2024. The region benefits from a well-developed regulatory landscape, ongoing investment in agricultural R&D, and a strong push for environmentally responsible farming practices. Polysaccharides are widely favored in the U.S. due to their environmental compatibility and effectiveness. In this highly industrialized and tech-focused market, stabilizers and adjuvants are essential to maintaining product stability and ensuring alignment with other agrochemical systems. The dominant use of active ingredients such as microbial inoculants, amino acids, and seaweed-based materials underscores a growing preference for biologicals and precision inputs in modern agriculture.

Key players shaping the Global Biostimulants Formulation Material Market include Novozymes A/S, BASF SE, Valagro S.p.A., UPL Limited, and Syngenta AG. To establish a strong foothold in the Biostimulants Formulation Material Market, companies are investing heavily in research to develop sustainable, crop-specific products that enhance yield while aligning with environmental standards. A major focus lies in innovation-particularly in creating biodegradable, tailored formulations suited for varied climatic and soil conditions. Strategic collaborations with agricultural tech firms, research institutes, and growers are helping companies co-develop region-specific solutions. Firms are also expanding global distribution networks and entering emerging markets to tap into new growth areas. Emphasis on digital platforms and precision agriculture tools supports real-time customization of product offerings.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Material type

2.2.2 Form

2.2.3 Application method

2.2.4 Crop type

2.2.5 Regional

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising demand for sustainable and organic agricultural inputs

3.2.1.2 Regulatory support for eco-friendly crop protection products

3.2.1.3 Increasing focus on crop yield and quality enhancement

3.2.1.4 Technological advancements in formulation and delivery systems

3.2.2 Industry pitfalls and challenges

3.2.2.1 Limited farmer awareness and technical knowledge

3.2.2.2 Variability in product efficacy due to environmental factors

3.2.3 Market opportunities

3.2.3.1 Development of crop-specific and customized formulations

3.2.3.2 Integration with digital agriculture and precision farming

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter’s analysis

3.6 PESTEL analysis

3.7 Technology and innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Price trends

3.8.1 By region

3.8.2 By material type

3.9 Cost breakdown analysis

3.10 Patent analysis

3.11 Sustainability and environmental aspects

3.11.1 Sustainable practices

3.11.2 Waste reduction strategies

3.11.3 Energy efficiency in production

3.11.4 Eco-friendly Initiatives

3.12 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 North America

4.2.2 Europe

4.2.3 Asia Pacific

4.2.4 LATAM

4.2.5 MEA

4.3 Competitive analysis of major market players

4.4 Competitive positioning matrix

4.5 Strategic outlook matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New Product Launches

4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, by Material Type, 2021 - 2034 (USD Bn, Tons)