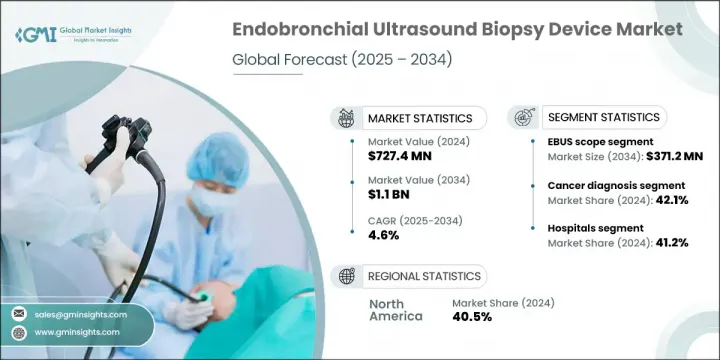

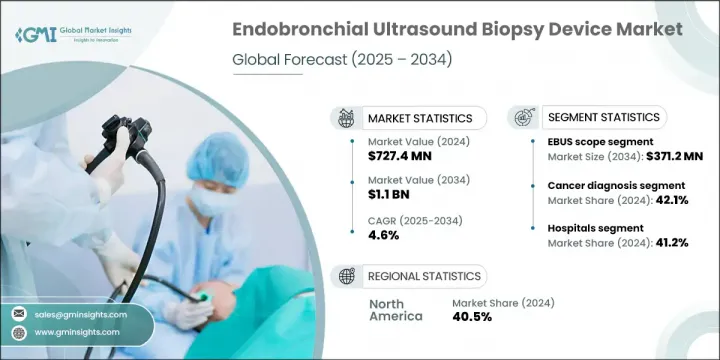

세계의 기관지 내 초음파 생검 장치 시장은 2024년에 7억 2,740만 달러로 평가되어 CAGR 4.6%로 성장할 전망이며, 2034년에는 11억 달러에 달할 것으로 예측되고 있습니다.

이 시장의 성장은 고령 인구 증가, 호흡기 질환 발생률 상승, 최소 침습적 진단 기술에 대한 수요 증가, 생검 장비의 지속적인 기술적 발전에 의해 촉진되고 있습니다. 이 기기들은 의료진이 폐 및 주변 림프절에서 조직 샘플을 높은 정확도로 채취하고 환자의 불편을 최소화하도록 설계되었습니다. 비침습적 진단으로의 전환에 따라 병원, 진단 실험실, 암 치료 센터는 폐암 및 기타 흉부 질환을 진단하고 병기를 결정하기 위해 이러한 초음파 유도 솔루션을 점점 더 많이 도입하고 있습니다. 조기 질환 발견과 효율적인 임상 절차에 대한 수요 증가 역시 일상적인 의료 실무에서 EBUS 도구 활용이 확대되는 데 기여하고 있습니다.

생검 플랫폼의 기술적 혁신은 진단 절차의 미래를 변화시키고 있습니다. 최근 솔루션은 이제 탄성영상술, AI 기반 내비게이션, 하이브리드 영상과 같은 기능을 포함하여 향상된 정확성과 절차 효율성을 제공합니다. 이러한 혁신은 합병증 위험을 줄이고, 워크플로우를 간소화하며, 환자 경험 개선에 기여합니다. 또한 의료 시스템이 조기 및 정확한 진단을 강조함에 따라, 더 침습적인 수술의 필요성을 줄일 수 있는 능력으로 인해 이러한 시스템에 대한 의존도가 높아지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 7억 2,740만 달러 |

| 예측 금액 | 11억 달러 |

| CAGR | 4.6% |

EBUS 바늘 부문은 2024년 2억 430만 달러를 기록했으며, 2034년까지 연평균 성장률(CAGR) 5.2%로 성장할 전망이며 3억 3650만 달러에 달할 것으로 전망됩니다. 이 부문의 성장은 다양한 바늘 게이지 옵션과 시술 중 가시성을 향상시키는 에코제닉 팁 기술에 의해 뒷받침됩니다. 기관지경검사와 초음파 프로브를 결합한 EBUS 스코프는 기도 근처 조직 및 림프절의 실시간 영상 촬영을 가능하게 합니다. 이 스코프는 개흉 수술 없이도 진단용 검체를 채취할 수 있는 기관지경 바늘 흡인술(TBNA) 수행에 필수적입니다. 이 기술은 불편감을 최소화할 뿐만 아니라 폐 또는 흉부 검사를 받는 환자의 회복 속도를 높이고 위험을 낮춥니다.

2024년 기준 암 진단 용도 부문이 42.1%의 점유율을 차지했습니다. 흉부암 발생률 증가로 정밀한 실시간 진단 도구에 대한 수요가 급증하고 있습니다. EBUS 내시경, TBNA 장치, 탄성영상 기능이 탑재된 프로브는 병기 결정 및 조기 발견에 필수적이며, 의료진이 맞춤형 치료 계획을 수립하는 데 필요한 데이터를 제공합니다. 암 사례가 지속적으로 증가함에 따라 의료 서비스 제공자들은 증가하는 진단 수요를 충족시키기 위해 고급 초음파 유도 생검 장비 도입을 촉진하고 있습니다.

미국의 기관지 내 초음파 생검 장치 시장은 2024년 기준 2억 6,940만 달러 규모로 평가되었습니다. 이러한 상승세는 만성 폐쇄성 폐질환(COPD), 결핵, 암과 같은 폐 질환의 높은 유병률에 기인합니다. 또한 체계적인 규제 프레임워크, 인구의 인식 제고, 연구개발(R&D)에 대한 강력한 투자가 전국적으로 임상 현장에 첨단 EBUS 기술의 광범위한 통합을 뒷받침하고 있습니다.

기관지 내 초음파 생검 장치 시장의 주요 기업은 시장에서의 존재감을 높이기 위해 다양한 전략을 전개하고 있습니다.

많은 기업들이 인공지능(AI) 지원 내비게이션 시스템, 향상된 시각화 도구, 인체공학적 생검 장비를 개발하기 위해 연구개발(R&D)에 막대한 투자를 하고 있습니다. 여러 기업들은 진단 정확도와 환자 안전 기능을 개선한 기기 출시를 통해 제품 포트폴리오를 확대되고 있습니다. 병원 및 진단 센터와의 전략적 협력도 기업들이 기술 도입을 가속화하는 데 도움이 되고 있습니다. 임상 시험 및 의사 교육 프로그램에 대한 파트너십은 실제 환경에서의 검증과 사용자 역량 확대를 지원합니다.

The Global Endobronchial Ultrasound Biopsy Device Market was valued at USD 727.4 million in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 1.1 billion by 2034. Growth in this market is driven by the increasing aging population, a growing incidence of respiratory diseases, rising demand for minimally invasive diagnostic techniques, and ongoing technological advancements in biopsy equipment. These devices are designed to assist clinicians in collecting tissue samples from the lungs and surrounding lymph nodes with high accuracy and minimal patient discomfort. With a shift toward less invasive diagnostics, hospitals, diagnostic labs, and cancer care centers are increasingly adopting these ultrasound-guided solutions to diagnose and stage diseases such as lung cancer and other thoracic conditions. The rising demand for early disease detection and efficient clinical procedures is also contributing to the growing utilization of EBUS tools in routine medical practice.

Technological breakthroughs in biopsy platforms are transforming the landscape of diagnostic procedures. Modern solutions now include features like elastography, AI-enabled navigation, and hybrid imaging, which offer enhanced accuracy and procedural efficiency. These innovations help reduce complication risks, streamline workflow, and contribute to improved patient experiences. Additionally, as healthcare systems emphasize early and accurate diagnosis, there's a higher reliance on these systems for their ability to reduce the need for more invasive surgeries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $727.4 Million |

| Forecast Value | $1.1 Billion |

| CAGR | 4.6% |

The EBUS needle segment generated USD 204.3 million in 2024 and is forecast to reach USD 336.5 million by 2034, growing at a CAGR of 5.2%. The growth of this segment is supported by diverse needle gauge options and echogenic tip technology, which improve visibility during procedures. EBUS scopes, which incorporate ultrasound probes with bronchoscopy, enable real-time imaging of tissues and lymph nodes near the airways. These scopes are essential for performing transbronchial needle aspiration (TBNA), a method that allows clinicians to obtain diagnostic samples without resorting to open procedures. This technique not only minimizes discomfort but also ensures faster recovery and lower risks for patients undergoing lung or thoracic evaluations.

In 2024, the cancer diagnosis application segment held 42.1% share. The increasing incidence of thoracic cancers has sharply raised the need for precise, real-time diagnostic tools. EBUS scopes, TBNA devices, and elastography-equipped probes are vital for staging and early detection, offering clinicians the data necessary to design personalized treatment plans. As cases of cancer continue to rise, healthcare providers are accelerating the adoption of advanced ultrasound-guided biopsy equipment to meet growing diagnostic demands.

United States Endobronchial Ultrasound Biopsy Device Market was valued at USD 269.4 million in 2024. This upward trajectory is attributed to the high prevalence of lung conditions like COPD, tuberculosis, and cancer. Additionally, a well-structured regulatory framework, growing awareness among the population, and strong investments in R&D have supported the widespread integration of advanced EBUS technology in clinical practices across the country.

Notable companies involved in the Global Endobronchial Ultrasound Biopsy Device Market include Siemens Healthineers, B. Braun, Cook Medical, Argon Medical Devices, Fujifilm Holdings, Praxis Medical, Hobbs Medical, Olympus Corporation, Boston Scientific, ACE Medical Devices, GE Healthcare, Koninklijke Philips, Clinodevice, Medi-Globe, and Medtronic. Key players in the endobronchial ultrasound biopsy device market are deploying a range of strategies to strengthen their market presence.

Many are heavily investing in R&D to develop AI-assisted navigation systems, enhanced visualization tools, and more ergonomic biopsy instruments. Several companies are expanding their product portfolios through the launch of devices with improved diagnostic accuracy and patient safety features. Strategic collaborations with hospitals and diagnostic centers are also helping firms to accelerate technology adoption. Partnerships for clinical trials and physician training programs support real-world validation and broaden user competence.