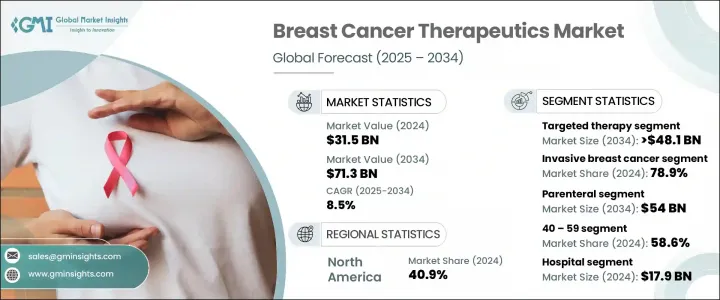

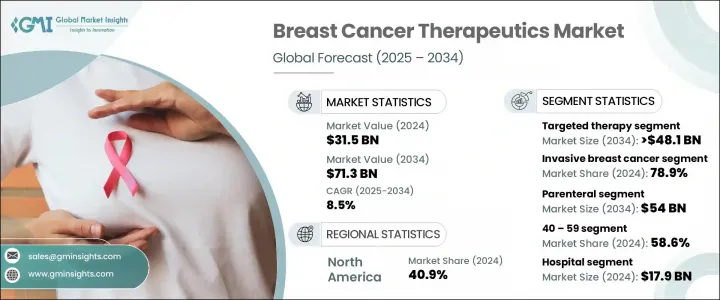

세계의 유방암 치료 시장은 2024년 315억 달러로 평가되며 CAGR 8.5%로 성장해 2034년까지 713억 달러에 이를 것으로 추정되고 있습니다.

시장 성장의 요인은 높은 유방암 이환율, 조기 발견 및 치료에 대한 의식이 높아지고, 정부나 비영리 단체에 의한 검진 지원이 많기 때문입니다. 검진이 증가하고 조기에 발견되는 사례가 증가함에 따라 효과적인 치료 옵션에 대한 수요가 증가하고 시장 기세를 지원하고 있습니다. 또한 고령화율 상승, 비만, 앉기 쉬운 라이프스타일, 도시화가 유방암 유병률 상승에 기여하고 있습니다. 신흥국 시장에서의 의료 접근의 확대가 치료의 보급을 더욱 뒷받침하고 있습니다. 표적치료, 호르몬요법, 면역요법 등의 맞춤형 의료의 진보가 치료 성적을 향상시켜 시장 확대에 박차를 가하고 있습니다.

유방암 치료 질환의 진행을 억제하고, 재발을 예방하고, 생존율을 향상시키는 것을 목적으로 한 일련의 치료가 포함됩니다. Merck, AstraZeneca, Novartis, Pfizer, and F. Hoffmann-La Roche 등 주요 제약 회사는 연구 개발에 많은 투자를 하고 있으며, 특히 프리시전 종양와 바이오마커 주도형 치료에 주력하고 있습니다. 정부의 검진 프로그램과 계몽 캠페인은 조기 진단을 가속화하고 나아가 선진적 치료에 대한 수요를 견인하고 있습니다. 신흥국의 헬스케어 인프라의 성장과 상환제도 개혁을 통해 보다 광범위한 접근이 가능합니다. 단일클론항체, 저분자 억제제, 면역종양약 등, 보다 표적을 좁힌 치료로의 전환이, 부작용을 억제하면서 효능을 향상시켜, 채용을 한층 더 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 315억 달러 |

| 예측 금액 | 713억 달러 |

| CAGR | 8.5% |

표적 치료제는 암 관련 바이오마커를 표적으로 하고 부작용이 적기 때문에 2024년 214억 달러의 매출을 기록했습니다. 항체 약물 복합체, HER2 억제제, PARP 억제제 등의 치료 형태는 초기 단계부터 후기 단계까지의 치료 프로토콜에서 널리 사용됩니다. HER2 낮은 하위유형 치료제와 AI를 통한 환자 계층화의 혁신은 이 범주의 지속적인 시장 리더십을 지원합니다.

침윤성 유방암 부문은 2024년에 78.9%의 점유율을 차지하며, 가장 이환율이 높은 병형입니다. 침윤성 유관암만으로 침윤성 증례의 약 80%, 유방암 진단의 약 55%를 차지합니다. 침윤성 유방암은 그 공격적인 성질과 유관외로의 전이의 가능성으로부터, 표적약, SERM 등의 호르몬 조정약, 화학요법, 면역요법 등 폭넓은 치료 어프로치가 요구되어 강한 임상 수요를 견인하고 있습니다.

북미의 유방암 치료 시장 점유율은 2024년 40.9%로 미국과 캐나다가 이끌고 있습니다. 고도의 헬스케어 인프라, 조기 발견에 대한 의식의 높이, 왕성한 암 연구 투자, 유리한 상환 제도가 치료제 채용을 뒷받침했습니다. 이 지역은 신속한 규제 당국의 승인, 독자적인 치료법의 높은 보급률, 새로운 치료법의 광범위한 도입 등의 혜택을 받아 세계 유방암 치료 상황에서의 리더십을 강화하고 있습니다.

이 업계를 형성하는 주요 기업은 기술 혁신과 세계 전개를 추진하고 있습니다. 주요 제약 회사는 동반자 진단에 의해 최적화된 정밀 표적 치료를 가능하게 하는 분자 아형에 의한 환자의 층별화에 중점을 둡니다. 많은 기업들이 항체 약물 복합체, 이중특이적 항체, CDK4/6 억제제, 면역요법의 조합 등 신규 치료법의 파이프라인을 확충하고 포트폴리오의 충실을 도모하고 있습니다. 바이오테크놀러지 기업과의 전략적 인수, 라이선싱 계약, 전략적 제휴로 혁신적인 화합물과 새로운 R&D 인력에 대한 접근이 가속화되고 있습니다. 신흥 시장으로의 세계 확장은 지역 판매자 및 의료 시스템과의 제휴를 통해 이루어지고 있습니다. 또한 기업은 상환협상을 지원하기 위해 실제 임상시험과 가치를 바탕으로 하는 성과에 투자하고 있습니다.

The Global Breast Cancer Therapeutics Market was valued at USD 31.5 billion in 2024 and is estimated to grow at a CAGR of 8.5% to reach USD 71.3 billion by 2034. The market growth is attributed to a combination of factors: high incidence of breast cancer, expanded awareness of early detection and treatment, and rising support from government and nonprofit screening initiatives. As screening increases and more cases are identified at earlier stages, demand for effective treatment options rises, supporting the market's momentum. Also, rising rates of aging populations, obesity, sedentary lifestyles, and urbanization are contributing to higher breast cancer prevalence. Expanded health access in developing markets further boosts therapy uptake. Advances in personalized medicine-such as targeted treatments, hormone therapy, and immunotherapy-are enhancing outcomes and fueling market expansion.

Breast cancer therapeutics encompass a spectrum of treatments aimed at controlling disease progression, preventing recurrence, and improving survival. Leading pharmaceutical firms such as Merck, AstraZeneca, Novartis, Pfizer, and F. Hoffmann-La Roche are investing heavily in R&D, particularly focusing on precision oncology and biomarker-driven therapies. Government screening programs and awareness campaigns are accelerating early diagnosis, which in turn drives demand for advanced treatments. Growth in emerging economies' healthcare infrastructure and reimbursement reforms enabling broader access. The shift toward more targeted interventions-including monoclonal antibodies, small-molecule inhibitors, and immuno-oncology agents-is improving efficacy while reducing side effects, further boosting adoption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $31.5 Billion |

| Forecast Value | $71.3 Billion |

| CAGR | 8.5% |

The targeted therapies generated USD 21.4 billion in 2024, dominating due to their ability to target cancer-associated biomarkers with fewer adverse reactions. Formats such as antibody-drug conjugates, HER2 inhibitors, and PARP inhibitors are widely adopted across both early- and late-stage treatment protocols. Innovations in HER2 low subtype therapies and AI guided patient stratification support continued market leadership of this category.

The invasive breast cancer segment held 78.9% share in 2024 and is the most prevalent form of disease. Invasive ductal carcinoma alone accounts for about 80% of all invasive cases and roughly 55% of breast cancer diagnoses. Because of its aggressive nature and potential to metastasize beyond the ducts, invasive breast cancer demands broad treatment approaches, including targeted agents, hormone modulators such as SERMs, chemotherapy, and immunotherapies, driving strong clinical demand.

North America Breast Cancer Therapeutics Market held 40.9% share in 2024, with the United States and Canada leading. Advanced healthcare infrastructure, high early detection awareness, strong oncology research investment, and favorable reimbursement systems drove therapeutic adoption. This region benefits from rapid regulatory approvals, high proprietary therapy penetration, and widespread uptake of emerging treatment modalities, reinforcing its leadership in the global breast cancer therapeutics landscape.

Major companies shaping this industry include Pfizer, F. Hoffmann-La Roche, Merck, AstraZeneca, Novartis, and Eli Lilly, driving innovation and global reach. Leading pharmaceutical players are focusing heavily on patient stratification by molecular subtype, enabling precision-targeted therapies optimized with companion diagnostics. Many firms are expanding pipelines in novel modalities such as antibody-drug conjugates, bispecific antibodies, CDK4/6 inhibitors, and immunotherapy combinations to strengthen portfolio depth. Strategic acquisitions, licensing agreements, and strategic partnerships with biotech firms accelerate access to innovative compounds and emerging R&D talent. Global expansion into emerging markets is being achieved through collaborations with regional distributors and healthcare systems. Additionally, firms invest in real-world studies and value-based outcomes to support reimbursement negotiations.