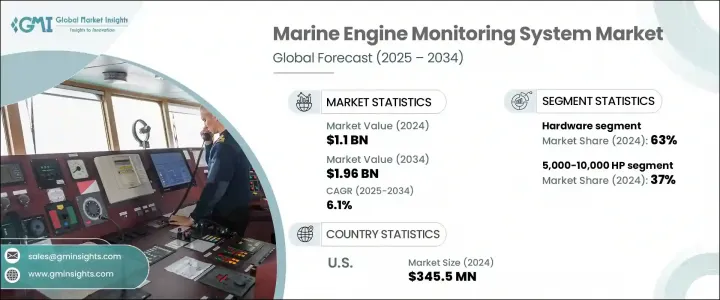

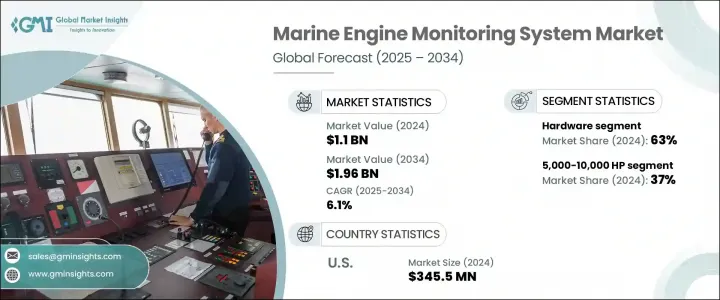

세계의 선박용 엔진 모니터링 시스템 시장 규모는 2024년 11억 달러에 달했고, CAGR 6.1%로 성장해 2034년까지 19억 6,000만 달러에 이를 것으로 예측됩니다.

배기가스 규제가 강화되고 선박용 엔진 기술이 고도화됨에 따라 모니터링 시스템은 기본적인 유지보수 도구에서 운영을 최적화하기 위한 필수 플랫폼으로 전환하고 있습니다. 이러한 시스템은 현재 실시간 데이터, 디지털 연결 및 예측 기능에 의존하며 연료 효율, 안전성 및 규정 준수 강화를 실현하고 있습니다. IoT 통합, AI 기반 분석, 지능형 센서 네트워크 등의 기술은 운영자가 함대 성능을 관리하는 방법을 재구성합니다. 업계는 또한 스마트 해상 운영에 맞는 고급 훈련 생태계를 구축하는 OEM 주도의 노력과 함께 해사에서 디지털화를 추진하는 관민 이니셔티브로부터 기세를 얻고 있습니다. 데이터 중심의 통찰력에 대한 수요는 해운 산업 전반에서 지능형 엔진 모니터링 툴의 채택을 가속화하고 있습니다.

팬데믹(세계적 유행) 후 원격 진단 및 모니터링 채택이 가속화되었습니다. 대규모 상업용 함대에서는 연료 효율 저하, 실린더 과도한 마모, 윤활 불량 등의 문제를 조기에 발견할 수 있는 예측 및 상태 기반 모니터링 기능이 표준화되고 있습니다. 이러한 시스템은 가동 중지 시간을 최소화하고 세계의 지속가능성 목표에 부합합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 11억 달러 |

| 예측 금액 | 19억 6,000만 달러 |

| CAGR | 6.1% |

2024년 하드웨어 부문은 63%의 점유율을 차지하며 2034년까지 연평균 복합 성장률(CAGR) 5%를 보일 것으로 예측됩니다. 이 부문에는 선상에서 원활한 데이터 수집 및 시스템 통합을 촉진하는 제어 유닛, 센서, 데이터 로거, 통신 모듈 등의 주요 구성 요소가 포함됩니다. 선박의 신설과 개조가 증가하고, 특히 배기 가스 규제에 대한 대응과 예지 보전 기능이 중요해짐에 따라, 하드웨어의 설치 수요가 높아지고 있습니다. Siemens, ABB, Wartsila와 같은 주요 OEM은 첨단 센서 기술을 추진 시스템과 보조 시스템에 직접 통합하여 종합적인 성능 모니터링을 가능하게 합니다.

5,000-10,000HP의 출력 범위 부문은 2024년에 37%의 점유율을 차지했고 2034년까지 연평균 복합 성장률(CAGR) 6%를 보일 것으로 예측되고 있습니다. 이 범위의 선박(주로 중형 유조선, 해양 지원 선박, 화물 운반선)은 운전 시간 연장과 엄격한 규제 요구 사항으로 인해 견고한 모니터링이 필요합니다. 이 출력 범위를 위한 모니터링 시스템은 상세한 분석, 예측 통찰력, AI 대응 진단을 제공하며, 예방 보전, 선대 최적화 및 진화하는 환경 기준 준수를 지원합니다. 이 범위를 목표로 하는 OEM은 서비스 제공에 예측 도구를 통합하는 경향이 커지고 있습니다.

미국의 선박용 엔진 모니터링 시스템 시장은 83%의 점유율을 차지하며, 2024년에는 3억 4,550만 달러를 벌었습니다. 이 나라의 주도적 지위는 상업선박과 방위선박의 대규모 선대, 배출에 관한 규제압력, 디지털 해사기술의 보급에 의해 지원되고 있습니다. 엣지 컴퓨팅, AI 기반 엔진 진단 및 연결 시스템에 대한 투자는 공공 및 민간 해양 사업자 모두 성능을 간소화하는 데 도움이 됩니다. 정부와의 계약 및 강력한 기술 인프라에 대한 액세스를 통해 미국 OEM과 통합자는 하이 엔드 스마트 시스템으로 국내 수요를 충족시킬 수 있습니다. MEMS 및 바이오연료전지로 현장 모니터링과 같은 기술은이 지역의 고급 엔지니어링 능력 덕분에보다 광범위한 애플리케이션을 발견하고 있습니다.

세계 선박용 엔진 모니터링 시스템 시장을 적극적으로 형성하는 주요 기업으로는 Caterpillar, Wartsila, Cummins, Siemens, ABB, Kongsberg Maritime, MAN Energy Solutions 등이 있습니다. 해양 엔진 모니터링 시스템 시장에서 경쟁하는 기업들은 디지털 기능 확대, 스마트 컴포넌트 개발, 세계 서비스 강화에 주력하고 있습니다. 대부분은 AI, IoT 및 클라우드 연결을 엔진 모니터링 솔루션에 통합하여 고급 진단, 자동 보고서 및 실시간 통찰력을 제공합니다. 해운 사업자와의 파트너십을 통해 이러한 기업은 운항 효율을 향상시키는 맞춤형 솔루션을 공동 개발할 수 있습니다. 또한 하이브리드 추진 시스템에 주력하고 모니터링 도구를 활용하여 연료 소비량과 배출량을 최적화하는 기업도 있습니다. 교육 플랫폼 및 애프터 서비스 생태계에 대한 투자는 고객 유지를 보장하는 데 도움이 됩니다.

The Global Marine Engine Monitoring System Market was valued at USD 1.1 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 1.96 billion by 2034. As emission standards tighten and marine engine technologies become more advanced, monitoring systems have transitioned from basic maintenance tools to essential platforms for optimizing operations. These systems now rely on real-time data, digital connectivity, and predictive capabilities to deliver enhanced fuel efficiency, safety, and regulatory compliance. Technologies like IoT integration, AI-based analytics, and intelligent sensor networks are reshaping how operators manage fleet performance. The industry is also gaining momentum from public-private initiatives pushing digitalization in maritime, alongside OEM-led efforts to create advanced training ecosystems tailored for smart maritime operations. The demand for data-driven insights continues to accelerate the adoption of intelligent engine monitoring tools across the shipping industry.

Remote diagnostics and monitoring saw faster adoption following the pandemic, as restrictions prompted marine operators to adopt cloud-based tools to maintain operational continuity. Predictive and condition-based monitoring features are becoming standard across larger commercial fleets, enabling early detection of issues such as fuel inefficiency, excessive cylinder wear, or lubrication faults. These systems help minimize downtime and align with global sustainability goals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.1 Billion |

| Forecast Value | $1.96 Billion |

| CAGR | 6.1% |

In 2024, the hardware segment held 63% share and is forecasted to grow at a CAGR of 5% through 2034. This segment includes key components such as control units, sensors, data loggers, and communication modules that facilitate seamless data collection and system integration onboard. The rise in new vessel construction and retrofitting activities is boosting demand for hardware installations, especially as compliance with emission regulations and predictive maintenance capabilities becomes more critical. Leading OEMs like Siemens, ABB, and Wartsila are embedding advanced sensor technologies directly into propulsion and auxiliary systems to enable comprehensive performance monitoring.

The 5,000-10,000 HP power range segment held 37% share in 2024 and is projected to grow at a CAGR of 6% through 2034. Vessels within this range-typically medium-sized tankers, offshore support ships, and cargo carriers-require robust monitoring due to extended operational hours and strict regulatory requirements. Monitoring systems for this power range offer detailed analytics, predictive insights, and AI-enabled diagnostics that support preventive maintenance, fleet optimization, and compliance with evolving environmental standards. OEMs targeting this range are increasingly integrating predictive tools into their service offerings.

United States Marine Engine Monitoring System Market held 83% share and earned USD 345.5 million in 2024. The country's leadership position is supported by a sizable fleet of commercial and defense vessels, regulatory pressure on emissions, and widespread use of digital maritime technologies. Investments in edge computing, AI-based engine diagnostics, and connected systems are helping both public and private marine operators streamline performance. Access to government contracts and strong tech infrastructure allows US-based OEMs and integrators to meet domestic demand with high-end, smart systems. Technologies like MEMS and on-site monitoring via biofuel cells are finding broader applications thanks to the advanced engineering capabilities of the region.

Key players actively shaping the Global Marine Engine Monitoring System Market include Caterpillar, Wartsila, Cummins, Siemens, ABB, Kongsberg Maritime, and MAN Energy Solutions. Companies competing in the marine engine monitoring system market are focused on expanding digital capabilities, developing smart components, and enhancing global service reach. Many are integrating AI, IoT, and cloud connectivity into engine monitoring solutions to offer advanced diagnostics, automated reporting, and real-time insights. Partnerships with shipping operators allow these firms to co-develop customized solutions that improve operational efficiency. Some companies are also focusing on hybrid propulsion systems, leveraging monitoring tools to optimize fuel consumption and emissions. Investments in training platforms and aftersales service ecosystems help ensure customer retention.