아스팔트 첨가제 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)

Asphalt Additives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1797730

리서치사:Global Market Insights Inc.

발행일:2025년 07월

페이지 정보:영문 210 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

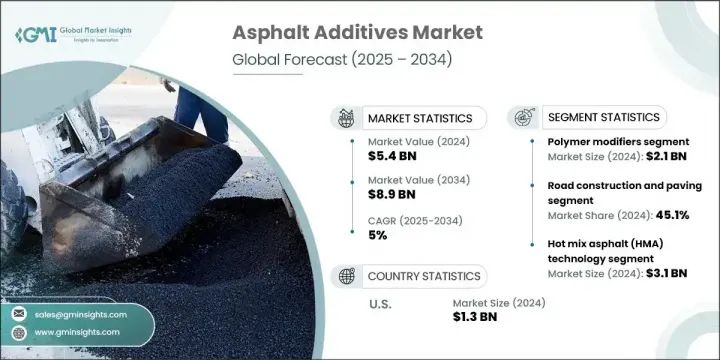

세계의 아스팔트 첨가제 시장은 2024년에 54억 달러로 평가되었으며 CAGR 5%를 나타내 2034년에는 89억 달러에 이를 것으로 추정됩니다.

세계적으로 대규모 인프라 프로젝트가 증가함에 따라 내구성, 지속가능성 및 비용 효과를 제공하는 아스팔트 솔루션에 대한 수요가 계속 증가하고 있습니다. 회춘제, 박리 방지제, 고분자 개질제 등의 첨가제는 점차 파고, 균열, 습기 관련 손상에 대한 내성을 향상시켜 아스팔트 혼합물을 강화하는 데 점점 더 많이 사용되고 있습니다. 장기적인 유지관리 예산을 억제하면서 도로의 수명을 연장하려는 정부는 이러한 자료에 주목하고 있습니다.

보다 저온의 혼합 기술과 재활용 재료의 사용 확대가 표준이 됨에 따라, 환경에 관한 지령이 이 부문의 기술 혁신을 형성하고 있습니다. 아스팔트 첨가제는 성능상의 이점뿐만 아니라 저 배출 가스 및 에너지 사용량을 줄이는 등 환경면에서의 이점에서도 지지를 받고 있습니다. 바이오 베이스와 나노 가공된 대체 재료의 상승은 보다 친환경 건설 프랙티스라는 세계의 목표에 더욱 부합하는 것입니다. 북미는 현대적인 인프라와 첨단 건설 시책에 의해 지원되며 여전히 주요 시장입니다. 한편, 유럽은 지속가능성에 초점을 맞춘 건설기준을 시행하고 순환형 경제모델을 중시하고 있기 때문에 이 부문에서 빠르게 전진하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

54억 달러

예측 금액

89억 달러

CAGR

5%

폴리머 개질제 부문은 2024년에 21억 달러를 창출했습니다. 아스팔트 강화에서 폴리머 개질제의 지속적인 이점은 격렬한 교통과 혹독한 날씨 하에서의 변형을 견디며 탄성과 강도를 높이는 능력에서 비롯됩니다. 이러한 첨가제는 기존의 아스팔트 제형에 원활하게 녹아 도로가 최소한의 혼란으로 장기적인 성능을 유지하는 데 도움이 됩니다.

2024년 도로 건설 및 포장 부문의 점유율은 45.1%였습니다. 이 부문의 성장은 격렬한 교통 부하와 날씨의 변화 모두를 견디는 오래 지속되는 고성능 도로에 대한 수요 증가를 반영합니다. 고분자 변성 첨가제 및 박리 방지 첨가제의 사용은 새로운 도시 도로 및 고속도로 인프라 프로젝트에서 노면의 내구성과 균열성을 실현하는 데 필수적입니다.

2024년 미국의 아스팔트 첨가제 시장 규모는 13억 달러로 평가되었습니다. 이 지역은 견고한 도로 시스템, 명확한 규제 방향, 교통 업그레이드에 대한 공공 부문과 민간 부문의 투자 증가로 계속 이어지고 있습니다. 이 나라의 연구와 혁신의 노력은 인프라의 탄력성을 높이면서 유지 보수의 필요성을 줄이는 지속 가능한 고성능 재료 개발에 중점을 둡니다. 이 트렌드는 기후에 적응한 도로망과 웜믹스 기술과 차세대 폴리머 배합을 포함한 친환경 건축자재의 긴급 요구가 주요 요인입니다.

아스팔트 첨가제 시장에서는 BASF SE, Arkema Group, Evonik Industries AG, Ingevity Corporation, DuPont de Nemours, Inc.와 같은 주요 기업이 이 부문에서 주요 역할을 하고 있으며 완만한 통합을 볼 수 있습니다. 아스팔트 첨가제 부문의 주요 기업은 지속 가능한 제품 혁신에 투자하고 낮은 VOC, 바이오, 웜 믹스 호환 첨가제 개발에 주력하고 있습니다. 이러한 기업들은 기후 변화에 강한 도로 인프라에 대한 수요 증가에 대응하기 위해 연구개발 능력을 적극적으로 확대하고 있습니다. 대부분은 인프라 개발자 및 정부 기관과 파트너십을 맺고 환경 지침을 충족하고 도로 수명을 향상시키는 고급 첨가제 배합을 검사적으로 개발하고 있습니다. 지리적 확대는 여전히 핵심 전략이며, 각 회사는 판매 제휴와 현지 생산을 통해 신흥 시장을 대상으로 하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 산업 고찰

생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

파괴적 혁신

산업에 미치는 영향요인

성장 촉진요인

산업의 잠재적 리스크 및 과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현재의 기술 동향

신흥기술

가격 동향

지역별

재료 유형별

향후 시장 동향

기술과 혁신의 상황

현재의 기술 동향

신흥기술

특허 상황

무역 통계(HS코드)

(참고 : 무역 통계는 주요 국가에서만 제공됩니다)

주요 수입국

주요 수출국

지속가능성과 환경 측면

지속 가능한 사례

폐기물 감축 전략

생산에 있어서의 에너지 효율

친환경 활동

탄소발자국의 고려

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

합병과 인수

파트너십 및 협업

신제품 발매

확대 계획

제5장 시장 추정·예측 : 제품 유형별(2021-2034년)

주요 동향

폴리머 개질제

스티렌-부타디엔-스티렌(SBS)

스티렌-부타디엔 고무(SBR)

에틸렌 비닐 아세테이트(EVA)

폴리에틸렌 및 폴리프로필렌

기타 폴리머 개질제

스트리핑 방지제

아민계 제제

석회계 제제

인산 유도체

유기 실란 화합물

유화제 및 계면활성제

음이온 유화제

양이온 유화제

비이온 유화제

온믹스 아스팔트 첨가제

왁스계 첨가제

화학계 첨가제

발포 첨가제

회춘제 및 재활용제

나노 재료 첨가제

나노실리카

나노클레이

탄소나노튜브

그래핀 및 산화 그래핀

바이오 기반 및 지속 가능한 첨가제

기타 특수 첨가제

제6장 시장 추정·예측 : 용도별(2021-2034년)

주요 동향

도로건설 및 포장

고속도로 건설

도시도로 개발

농촌도로 인프라

도로의 유지 관리 및 수리

표면 처리

오버레이 적용

균열 실링 및 수리

공항 활주로 건설

지붕재 용도

상업용 루핑

주택용 루핑

산업용 루핑

방수 및 밀봉

기타

제7장 시장 추정·예측 : 기술별(2021-2034년)

주요 동향

핫믹스 아스팔트(HMA) 기술

온믹스 아스팔트(WMA) 기술

콜드 믹스 아스팔트 기술

반온 믹스 아스팔트 기술

재활용 기술

핫 인 플레이스 재활용

콜드 인 플레이스 재활용

식물 유래 재활용

제8장 시장 추정·예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

네덜란드

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제9장 기업 프로파일

Arkema Group

BASF SE

DuPont de Nemours, Inc.

Evonik Industries AG

Nouryon(구 AkzoNobel Specialty Chemicals)

Ingevity Corporation

Kraton Corporation

Honeywell International Inc.

The Dow Chemical Company

Sasol Limited

KTH

영문 목차

영문목차

The Global Asphalt Additives Market was valued at USD 5.4 billion in 2024 and is estimated to grow at a CAGR of 5% to reach USD 8.9 billion by 2034. As large-scale infrastructure projects increase worldwide, demand continues to rise for asphalt solutions that offer durability, sustainability, and cost-effectiveness. Additives such as rejuvenators, anti-stripping agents, and polymer modifiers are increasingly used to enhance asphalt mixtures by improving resistance to rutting, cracking, and moisture-related damage. Governments are turning to these materials as they seek to extend the lifespan of roads while keeping long-term maintenance budgets under control.

Environmental mandates are shaping innovation in this sector, as lower-temperature mixing technologies and greater use of recycled materials become standard. Asphalt additives are gaining traction not only for their performance benefits but also for their environmental advantages, including lower emissions and reduced energy usage. The rise of bio-based and nano-modified alternatives further aligns with global goals for greener construction practices. North America remains the leading market, backed by modern infrastructure and progressive construction policies. Meanwhile, Europe is rapidly advancing in this space as it enforces sustainability-focused construction standards and emphasizes circular economy models.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$5.4 billion

Forecast Value

$8.9 billion

CAGR

5%

The polymer modifiers segment generated USD 2.1 billion in 2024. Their continued dominance in asphalt enhancement stems from the ability to boost elasticity and strength while resisting deformation under intense traffic and severe weather. These additives blend seamlessly into existing asphalt formulations and help roads maintain long-term performance with minimal disruption.

The road construction and paving segment represented a 45.1% share in 2024. The sector's growth reflects increased demand for long-lasting, high-performance roads that can withstand both heavy traffic loads and shifting weather patterns. Use of polymer-modified and anti-stripping additives remains essential for delivering surface durability and crack resistance in new urban roadways and highway infrastructure projects.

United States Asphalt Additives Market generated USD 1.3 billion in 2024. The region continues to lead thanks to its robust road systems, clear regulatory direction, and rising public and private sector investment in transportation upgrades. Research and innovation efforts in the country are focused on developing sustainable, high-performance materials that lower maintenance requirements while enhancing infrastructure resilience. This trend is largely driven by the urgent need for climate-adapted road networks and environmentally conscious construction materials, including warm mix technologies and next-generation polymer formulations.

The Asphalt Additives Market shows moderate consolidation, with leading companies such as BASF SE, Arkema Group, Evonik Industries AG, Ingevity Corporation, and DuPont de Nemours, Inc. playing a major role in the sector. Leading firms in the asphalt additives space are investing in sustainable product innovation, focusing on the development of low-VOC, bio-based, and warm mix-compatible additives. These companies are actively expanding R&D capabilities to address the growing demand for climate-resilient road infrastructure. Many are forming partnerships with infrastructure developers and government agencies to pilot advanced additive formulations that meet environmental guidelines and improve road longevity. Geographic expansion remains a core strategy, with companies targeting emerging markets through distribution partnerships and local production.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Product type trends

2.2.2 Application trends

2.2.3 Technology trends

2.2.4 Regional

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.2 Industry pitfalls and challenges

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Technology and Innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Price trends

3.8.1 By region

3.8.2 By material type

3.9 Future market trends

3.10 Technology and Innovation landscape

3.10.1 Current technological trends

3.10.2 Emerging technologies

3.11 Patent Landscape

3.12 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only

3.12.1 Major importing countries

3.12.2 Major exporting countries

3.13 Sustainability and environmental aspects

3.13.1 Sustainable practices

3.13.2 Waste reduction strategies

3.13.3 Energy efficiency in production

3.13.4 Eco-friendly initiatives

3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo tons)

5.1 Key trends

5.2 Polymer modifiers

5.2.1 Styrene-butadiene-styrene (sbs)

5.2.2 Styrene-butadiene rubber (sbr)

5.2.3 Ethylene vinyl acetate (eva)

5.2.4 Polyethylene and polypropylene

5.2.5 Other polymer modifiers

5.3 Anti-stripping agents

5.3.1 Amine-based agents

5.3.2 Lime-based agents

5.3.3 Phosphoric acid derivatives

5.3.4 Organosilane compounds

5.4 Emulsifiers and surfactants

5.4.1 Anionic emulsifiers

5.4.2 Cationic emulsifiers

5.4.3 Non-ionic emulsifiers

5.5 Warm mix asphalt additives

5.5.1 Wax-based additives

5.5.2 Chemical-based additives

5.5.3 Foaming additives

5.6 Rejuvenators and recycling agents

5.7 Nanomaterial additives

5.7.1 Nanosilica

5.7.2 Nanoclay

5.7.3 Carbon nanotubes

5.7.4 Graphene and graphene oxide

5.8 Bio-based and sustainable additives

5.9 Other specialty additives

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo tons)

6.1 Key trends

6.2 Road construction and paving

6.2.1 Highway construction

6.2.2 Urban road development

6.2.3 Rural road infrastructure

6.3 Road maintenance and rehabilitation

6.3.1 Surface treatments

6.3.2 Overlay applications

6.3.3 Crack sealing and repair

6.4 Airport runway construction

6.5 Roofing applications

6.5.1 Commercial roofing

6.5.2 Residential roofing

6.5.3 Industrial roofing

6.6 Waterproofing and sealing

6.7 Other applications

Chapter 7 Market Estimates and Forecast, By Technology, 2021-2034 (USD Billion) (Kilo tons)

7.1 Key trends

7.2 Hot mix asphalt (hma) technology

7.3 Warm mix asphalt (wma) technology

7.4 Cold mix asphalt technology

7.5 Half-warm mix asphalt technology

7.6 Recycling technologies

7.6.1 Hot in-place recycling

7.6.2 Cold in-place recycling

7.6.3 Plant-based recycling

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo tons)