Silicon Battery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1797696

리서치사:Global Market Insights Inc.

발행일:2025년 07월

페이지 정보:영문 190 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

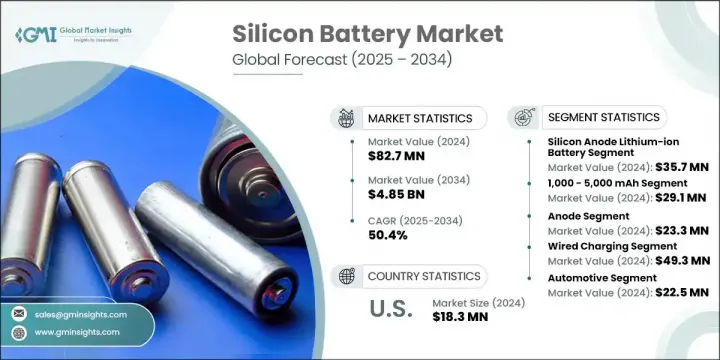

세계의 실리콘 배터리 시장 규모는 2024년에 8,270만 달러가 되고, CAGR 50.4%로 성장할 전망이며 2034년에는 48억 5,000만 달러에 이를 것으로 예측되고 있습니다.

이러한 성장의 주요 촉진요인 중 하나는 에너지 밀도와 배터리 효율이 핵심인 전기자동차(EV)에 대한 수요 증가입니다. 실리콘 음극은 최대 3,600 mAh/g의 성능을 제공할 수 있으며, 이는 372 mAh/g의 표준 흑연 음극 대비 약 10배에 달하는 향상된 수치입니다. 이러한 발전은 주행 거리 확대와 배터리 크기 축소를 가능하게 하여 성능과 차량 설계를 최적화합니다. 전기차 보급 증가와 더불어, 저배출 기준을 시행하는 전 세계 정책 및 제조사 주도의 무게나 비용 증가 없이 배터리 사양을 개선하려는 노력은 실리콘 기반 에너지 솔루션으로 전환을 가속화하고 있습니다. 실리콘 배터리 기술은 전기차부터 휴대용 전자기기까지 다양한 분야의 에너지 저장 방식을 재편할 수 있는 역량으로 점차 주목받고 있습니다. 기존 리튬이온 인프라와의 호환성을 유지하면서 소형 고용량 에너지 솔루션을 제공할 수 있는 이 기술은 향후 에너지 저장 분야의 핵심 발전으로 자리매김하고 있습니다.

음극 부문은 2024년 3,570만 달러 규모를 기록했습니다. 이러한 성장세는 기존 리튬이온 생산 시스템에 원활하게 통합될 수 있다는 점에 기인합니다. 자동차, 소비자 가전, 고정형 에너지 저장 장치 부문의 제조사들은 현재 생산 설비를 방해하지 않으면서 사이클 수명 및 에너지 밀도와 같은 성능 지표를 향상시키기 위해 실리콘 음극으로 전환하고 있습니다. 최근 하이브리드 실리콘-흑연 음극의 발전은 상업적 확장성을 더욱 원활하게 하여 다양한 분야에서의 시장 접근성과 용도 가능성을 확대되다는데 기여하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

8,270만 달러

예측 금액

48억 5,000만 달러

CAGR

50.4%

1,000-5,000mAh의 배터리가 2024년 2,910만 달러로 최대 점유율을 차지했습니다. 이 부문은 스마트폰, 태블릿, 스마트워치 등 소비자 기기에서 경량·소형 전원 솔루션 수요 증가로 지속적인 성장을 이어가고 있습니다. 이 중간 용량 실리콘 배터리는 공간 효율성이 중요한 최근 전자제품에 이상적이며, 세련된 제품 디자인 내에서 신뢰할 수 있는 성능과 뛰어난 휴대성을 제공합니다.

2024년 미국의 실리콘 배터리 시장은 1,830만 달러 규모로 평가되었습니다. 이 지역적 주도권은 지원적인 혁신 생태계, 탄탄한 자금 조달 채널, 그리고 상용화 전 단계의 증가하는 전개 덕분입니다. 현지 제조업체들은 전기 모빌리티 및 소비자 가전 용도에서 에너지 밀도를 높이고 전체 무게를 줄이기 위해 실리콘 배터리 기술을 적극적으로 검토하고 있습니다. 기존 자동차 업체와 신흥 기술 업체들이 배터리 혁신에 막대한 투자를 하면서 향후 실리콘 음극 솔루션으로 전환이 본격화되고 있습니다.

실리콘 배터리 시장에서 사업을 전개하는 주요 업계 기업은 BYD Company Ltd., 히타치 제작소, LG Energy Solution, Maxell Holdings, Ltd., Nanograf Corporation, Nexeon Ltd., Panasonic Holdings Corporation, Samsung SDI, StoreDot Ltd., Solid Power, Inc., Targray Tecnology International Ltd., OneD Battery Sciences, Group14 Technologies, Enovix Corporation, Sila Nanotechnologies, XNRGI, Enevate Corporation 등이 있습니다. 실리콘 배터리 시장에서의 입지를 공고히 하기 위해 기업들은 여러 전략적 계획을 실행하고 있습니다. 많은 기업들이 실리콘 음극 화학 성분을 개선하기 위해 연구개발 투자를 확대하며, 배터리 수명과 충전 유지율 향상에 주력하고 있습니다. 자동차 및 전자제품 제조사와의 파트너십을 통해 시장 침투를 심화하고 장기적인 공급망 통합을 실현하고 있습니다. 또한 기업들은 기존 리튬이온 배터리 시스템과의 호환성을 유지하면서 대량 생산을 위한 생산 라인을 최적화하여 채택을 원활하게 하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 촉진요인

성장 촉진요인

실리콘 음극의 고에너지 밀도

전기자동차(EV) 수요 급증

스타트업 기업과 거대 테크 기업의 상업화

고급 에너지 저장에 대한 정부 인센티브

VR/AR 및 AI 대응 트레이닝 시스템 도입

업계의 잠재적 위험 및 과제

체적 팽창과 사이클 안정성의 문제

높은 제조 비용

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현재의 기술 동향

신흥기술

가격 동향

지역별

제품별

가격 전략

새로운 비즈니스 모델

규정 준수 요건

소비자 감정 분석

특허 및 지적재산 분석

지정학과 무역의 역학

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

시장 집중 분석

주요 기업의 경쟁 벤치마킹

재무실적의 비교

수익

이익률

연구개발

제품 포트폴리오 비교

제품 라인업의 넓이

기술

혁신

지리적 존재의 비교

세계 실적 분석

서비스 네트워크의 범위

지역별 시장 침투율

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전(2021-2024년)

합병과 인수

파트너십 및 협업

기술적 진보

확대 및 투자 전략

디지털 변혁 이니셔티브

신흥기업 및 스타트업기업경쟁 구도

제5장 시장 추계 및 예측, 유형별(2021-2034년)

실리콘 음극 리튬 이온 배터리

실리콘 고체 배터리

실리콘-그래핀 복합 배터리

제6장 시장 추계 및 예측, 용량 범위별(2021-2034년)

1,000mAh 미만

1,000-5,000mAh

5,000-10,000mAh

10,000mAh 이상

제7장 시장 추계 및 예측, 컴포넌트별(2021-2034년)

양극

음극

전해질

분리막

기타

제8장 시장 추계 및 예측, 충전 유형별(2021-2034년)

유선 충전

무선 충전

제9장 시장 추계 및 예측, 최종 이용 산업별(2021-2034년)

자동차

전자

에너지 및 전력

의료

항공우주 및 방위

산업기기

기타

제10장 시장 추계 및 예측, 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

네덜란드

아시아태평양

중국

인도

일본

한국

호주

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제11장 기업 프로파일

BYD Company Ltd.

Enovix Corporation

Enevate Corporation

Group14 Technologies

Hitachi Ltd.

LG Energy Solution

Maxell Holdings Ltd.

Nanograf Corporation

Nexeon Ltd.

Novonix Ltd.

OneD Battery Sciences

Panasonic Holdings Corporation

QuantumScape Corporation

Samsung SDI

Sila Nanotechnologies

Solid Power, Inc.

StoreDot Ltd.

Targray Technology International

Toshiba Corporation

XNRGI

HBR

영문 목차

영문목차

The Global Silicon Battery Market was valued at USD 82.7 million in 2024 and is estimated to grow at a CAGR of 50.4% to reach USD 4.85 billion by 2034. One of the primary forces behind this growth is the increasing demand for electric vehicles (EVs), where energy density and battery efficiency are crucial. Silicon anodes can deliver up to 3,600 mAh/g, a nearly tenfold boost over standard graphite anodes rated at 372 mAh/g. This advancement enables a greater range and reduced battery size, optimizing performance and vehicle design. Alongside rising EV adoption, global policies enforcing low-emission standards and manufacturer-led efforts to improve battery specs without adding weight or cost are accelerating the shift toward silicon-based energy solutions. Silicon battery technology is increasingly recognized for its capacity to reshape energy storage across multiple sectors, from EVs to portable electronics. The technology's ability to offer compact, high-capacity energy solutions while maintaining compatibility with existing lithium-ion infrastructure positions it as a vital advancement in next-generation energy storage.

The anode segment generated USD 35.7 million in 2024. The reason behind this momentum lies in its seamless integration into existing lithium-ion production systems. Manufacturers across automotive, consumer electronics, and stationary energy storage segments are turning to silicon anodes to enhance performance metrics like cycle life and energy density without disrupting current manufacturing setups. Recent developments in hybrid silicon-graphite anodes are also enabling smoother commercial scalability, helping expand market reach and application potential across various sectors.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$82.7 million

Forecast Value

$4.85 billion

CAGR

50.4%

The batteries within the 1,000 to 5,000 mAh range represented the largest share in 2024, generating USD 29.1 million. This segment continues to thrive due to rising demand for lightweight and compact power solutions in consumer devices like smartphones, tablets, and smartwatches. These mid-range silicon batteries are ideal for modern electronics where space efficiency is critical, offering reliable performance and excellent portability within sleek product designs.

United States Silicon Battery Market was valued at USD 18.3 million in 2024. This regional leadership can be attributed to its supportive innovation ecosystem, robust funding channels, and a growing pipeline of pre-commercial deployments. Local manufacturers are actively assessing silicon battery technologies to enhance energy density while reducing overall weight in electric mobility and consumer electronics applications. As legacy automotive players and emerging tech manufacturers invest heavily in battery innovation, the shift toward next-generation silicon anode solutions is gaining serious traction.

Key industry players operating in the Silicon Battery Market include BYD Company Ltd., Hitachi, Ltd., LG Energy Solution, Maxell Holdings, Ltd., Nanograf Corporation, Nexeon Ltd., Panasonic Holdings Corporation, Samsung SDI, StoreDot Ltd., Solid Power, Inc., Targray Technology International, Toshiba Corporation, QuantumScape Corporation, Novonix Ltd., OneD Battery Sciences, Group14 Technologies, Enovix Corporation, Sila Nanotechnologies, XNRGI, and Enevate Corporation. To solidify their position in the Silicon Battery Market, companies are executing several strategic initiatives. Many are ramping up R&D investments to improve silicon anode chemistry, focusing on increasing battery life and charge retention. Partnerships with automotive and electronics manufacturers are enabling deeper market penetration and long-term supply chain integration. In addition, companies are optimizing production lines for mass-scale manufacturing, while maintaining compatibility with existing lithium-ion battery systems to streamline adoption.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Type trends

2.2.2 Capacity range trends

2.2.3 Component trends

2.2.4 Charging type trends

2.2.5 End use trends

2.2.6 Regional trends

2.3 TAM Analysis, 2025-2034 (USD Million)

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 High Energy Density of Silicon Anodes

3.2.1.2 Surging Demand for Electric Vehicles (EVs)

3.2.1.3 Commercialization by Startups and Tech Giants

3.2.1.4 Government Incentives for Advanced Energy Storage

3.2.1.5 Adoption of VR/AR and AI-enabled training systems

3.2.2 Industry pitfalls and challenges

3.2.2.1 Volumetric Expansion and Cycle Stability Issues