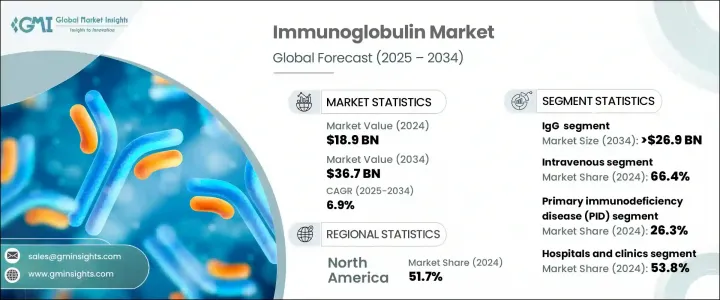

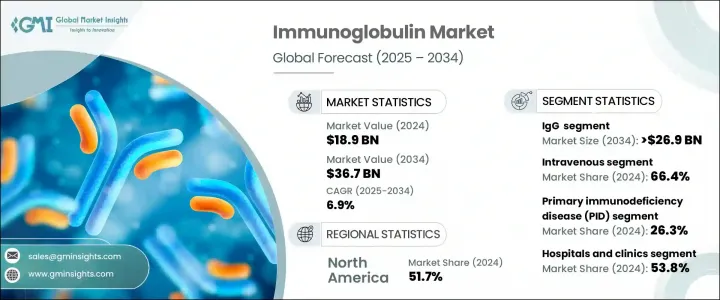

세계의 면역글로불린 시장은 2024년에는 189억 달러로 평가되었고, CAGR 6.9%로 성장할 전망이며, 2034년에는 367억 달러에 이를 것으로 추정됩니다.

이 시장 확대의 주요 요인은 다양한 연령층에서 1차성과 2차성 모두 면역 결핍증이 증가하고 있다는 것입니다. 진단 방법의 지속적인 진보와 헬스케어 제공업체의 의식이 증가함에 따라 만성 염증성 탈수성 다발성 신경염과 다소성 운동 신경병증과 같은 복잡한 질병의 발견률이 꾸준히 증가하고 있습니다.

이러한 질병은 종종 증상의 조절과 감염의 예방에 중요한 역할을 하는 면역글로불린 요법을 포함한 평생 치료가 필요하며 일관된 제품 수요에 박차를 가하고 있습니다. 면역글로불린은 면역계에 필수적인 성분이며 바이러스, 세균, 독소 등의 유해한 병원체를 인식하고 중화하는 항체로서 기능합니다. B세포에 의해 자연적으로 생산되는 이들 당단백질은 면역계에 추가적인 지원 및 조절이 필요한 환자에게 정맥내 또는 피하 투여됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 189억 달러 |

| 예측 금액 | 367억 달러 |

| CAGR | 6.9% |

자가면역질환과 면역 결핍 사례에서 면역글로불린 기반 치료에 대한 신뢰가 높아지면서 지속적으로 시장 전망을 강화하고 있습니다. 이러한 요법은 항체 결손을 수정하고 면역 활성을 조정하는 데 사용되며 환자에게 실행 가능한 장기적 해결책을 제공합니다. 세계 만성질환 이환율 상승과 맞물려 평균수명이 증가하고 면역지원을 필요로 하는 환자층이 확대되고 있어 수요도 확대되고 있습니다. 면역학 연구가 진행되고 제품에 대한 접근성이 향상됨에 따라 신경학, 혈액학, 내과학 등 많은 의료 분야에서 면역요법의 이용이 확산되고 있습니다. 지속적인 기술혁신, 신흥국 시장에서의 유리한 상환 시나리오, 혈장 채취 네트워크에 대한 전략적 투자로 시장 성장은 더욱 가속화될 것으로 예상됩니다.

다른 면역글로불린 클래스 중에서 IgG는 계속 지배적인 지위를 차지하고 있습니다. 2024년 IgG 부문은 74.1%의 시장 점유율을 차지하였고, 2034년에는 CAGR 6.8%로 269억 달러를 넘어설 것으로 예측됩니다. IgG의 우위성은 광범위한 임상 사용과 폭넓은 질환에 대한 유효성 확립에 기인하고 있습니다. IgG는 순환항체 중 가장 높은 비중을 차지하고 있어 병원체 중화, 수동면역 제공, 면역 관련 질환 관리에 필수적입니다. IgG는 그 안정적인 치료 성능과 폭넓은 적용 범위로 인해 헬스케어의 모든 상황에서 즐겨 사용되고 있습니다. 한편, IgA 부문은 가장 급성장하고 있는 부문의 하나로서 부상하고 있으며, 2034년까지의 CAGR 7.7%로 성장이 예측되고 있습니다. 점막 면역에서 IgA의 역할과 그 잠재적인 치료 용도에 대한 인식이 높아지는 것이 이 추세의 증가에 기여하고 있습니다.

용도의 관점에서 시장은 만성 염증성 탈수성 다발성 신경염, 다소성 운동 신경병증, 원발성 및 이차성 면역 결핍증, 길란 밸리 증후군, 면역성 혈소판 감소성 자반병 및 기타 틈새 질환을 포함한 다양한 질병으로 분류됩니다. 원발성 면역결핍증(PID) 분야는 2024년 26.3%의 점유율로 시장을 선도하고 CAGR 7.1%로 확대될 것으로 예측됩니다. 이 분야의 수요를 견인하고 있는 것은 면역기능을 충분히 유지하기 위해 일관된 치료가 필요한 평생에 걸친 질환이라는 것입니다. PID 환자는 기능적인 항체를 생산할 능력이 없고 잦은 감염병에 매우 취약하기 때문에 면역글로불린 투여는 질환 관리의 중요한 요소가 되고 있습니다. 감염병의 위험을 경감하고, 입원을 제한하고, 전체적인 환자의 전귀를 향상시키는 데 중요한 역할을 담당하고 있습니다.

최종 용도별로는 병원 및 진료소가 2024년 시장 점유율 53.8%로 세계 시장을 독점했습니다. 이러한 환경은 면역글로불린 요법, 특히 의학적 감독과 특수한 기기를 필요로 하는 링거 요법을 받는 환자의 주요 케어 포인트로 기능하고 있습니다. 병원의 관리된 환경은 안전한 링거 시행을 보장하며 부작용이 발생할 경우 즉시 개입할 수 있습니다. 반복 투여나 장기 투여가 필요하기 때문에 환자는 일관되고 안전한 투여를 병원이나 진료소에 의존하는 경우가 많습니다.

지역별로는 북미가 2024년에 51.7%의 점유율을 차지하여 최대 시장으로 부상했습니다. 이 지역은 선진적인 헬스케어 시스템, 견고한 상환 정책, 혈장 채취를 위한 확립된 인프라 등의 혜택을 받고 있습니다. 면역 관련 질환의 유병률이 높고 임상 기술 혁신이 진행되고 있는 것도 이 지역을 선도하는 요인이 되고 있습니다. 고령자 인구의 증가와 진단 능력의 향상도, 이 지역의 시장 확대에 크게 기여하고 있습니다.

시장 진출 기업은 강력한 공급망, 지속적인 제품 혁신, 전략적 파트너십을 통해 리더십을 유지하고 있습니다. 혈장분획의 전문지식 및 치료상 일관성을 중시하는 자세가 경쟁력을 높이고 있습니다. 각사는 또, 새로운 수요를 개발해, 종래의 제조 기술에의 의존을 줄이기 위해서 신흥 시장에 투자하고 있어, 보다 광범위한 세계 시장 침투에 대한 길을 열고 있습니다.

The Global Immunoglobulin Market was valued at USD 18.9 billion in 2024 and is estimated to grow at a CAGR of 6.9% to reach USD 36.7 billion by 2034. This expansion is largely attributed to the rising occurrence of immunodeficiency disorders, both primary and secondary, across various age groups. With continued advancements in diagnostics and greater awareness among healthcare providers, detection rates of complex conditions like chronic inflammatory demyelinating polyneuropathy and multifocal motor neuropathy are steadily increasing.

These conditions often require lifelong treatment involving immunoglobulin therapies, which play a key role in controlling symptoms and preventing infections, thereby fueling consistent product demand. Immunoglobulins are essential components of the immune system, functioning as antibodies that recognize and neutralize harmful pathogens such as viruses, bacteria, and toxins. Produced naturally by B cells, these glycoproteins are administered either intravenously or subcutaneously to patients whose immune systems require additional support or modulation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.9 Billion |

| Forecast Value | $36.7 Billion |

| CAGR | 6.9% |

The growing reliance on immunoglobulin-based therapies in autoimmune and immune deficiency cases continues to strengthen the market outlook. These therapies are used to correct antibody deficiencies and regulate immune activity, offering patients a viable long-term solution. Increasing life expectancy, coupled with a rise in chronic disease incidence globally, is creating a broader patient base that requires immune support, thereby adding to the demand pool. As immunology research progresses and product accessibility improves, the use of immunoglobulin therapy is gaining traction across numerous medical disciplines, including neurology, hematology, and internal medicine. Continuous innovation, favorable reimbursement scenarios in developed regions, and strategic investments in plasma collection networks are expected to further accelerate market growth.

Among the different immunoglobulin classes, IgG continues to hold the dominant position. In 2024, the IgG segment captured a market share of 74.1% and is anticipated to surpass USD 26.9 billion by 2034, with a CAGR of 6.8%. Its dominance stems from broad clinical usage and well-established efficacy in a wide range of conditions. IgG represents the highest proportion of circulating antibodies and is essential for neutralizing pathogens, offering passive immunity, and managing immune-related conditions. Its consistent therapeutic performance and wide application range make it the preferred choice across healthcare settings. Meanwhile, the IgA segment is emerging as one of the fastest-growing, projected to grow at a CAGR of 7.7% through 2034. Growing recognition of its role in mucosal immunity and its potential therapeutic applications is contributing to this increased momentum.

From an application perspective, the market is segmented into various conditions such as chronic inflammatory demyelinating polyneuropathy, multifocal motor neuropathy, primary and secondary immunodeficiency diseases, Guillain-Barre syndrome, immune thrombocytopenic purpura, and other niche disorders. The primary immunodeficiency disease (PID) segment led the market in 2024 with a share of 26.3% and is forecasted to expand at a CAGR of 7.1%. The demand in this segment is driven by the lifelong nature of the condition, which requires consistent immunoglobulin therapy to maintain adequate immune function. Patients with PID lack the ability to produce functional antibodies and are highly vulnerable to frequent infections, making immunoglobulin administration a vital component of disease management. It plays a critical role in reducing infection risks, limiting hospital admissions, and enhancing overall patient outcomes.

In terms of end use, the hospital and clinic segment dominated the global market with a market share of 53.8% in 2024. These settings serve as the primary point of care for patients receiving immunoglobulin therapy, particularly intravenous forms that demand medical supervision and specialized equipment. The controlled environment of hospitals ensures safe infusion practices and allows immediate intervention in case of adverse reactions. Given the requirement for repeated and long-term dosing, patients often rely on hospitals and clinics for consistent and secure administration.

Regionally, North America emerged as the largest market, commanding a share of 51.7% in 2024. The region benefits from advanced healthcare systems, robust reimbursement policies, and a well-established infrastructure for plasma collection. The high prevalence of immune-related disorders and ongoing clinical innovation further contribute to its leading position. The expanding elderly population and improved diagnostic capabilities are also key contributors to the region's market strength.

Market players are maintaining their leadership through strong supply chains, continuous product innovation, and strategic partnerships. Their expertise in plasma fractionation and focus on therapeutic consistency give them a competitive edge. Companies are also investing in emerging markets to tap into new demand and reduce dependence on traditional manufacturing techniques, paving the way for broader global market penetration.