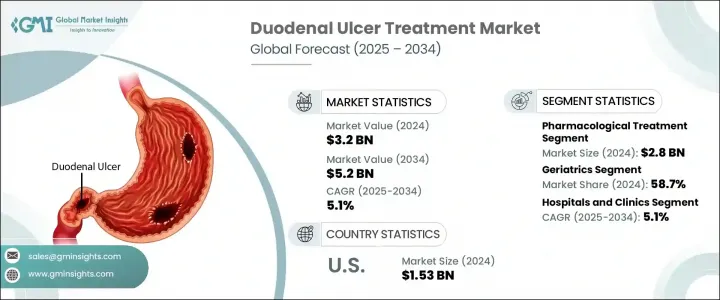

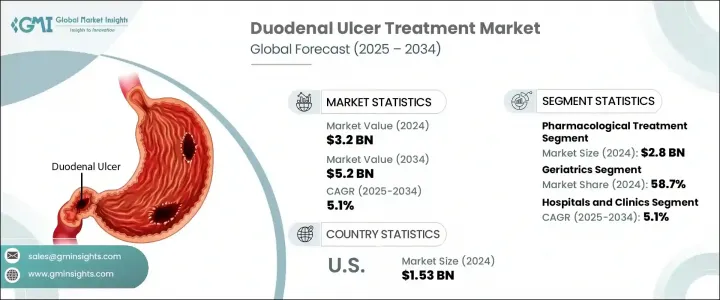

세계의 십이지장궤양 치료 시장은 2024년에는 32억 달러로 평가되었고, CAGR 5.1%로 성장할 전망이며, 2034년에는 52억 달러에 이를 것으로 추정됩니다.

이 성장에는 세계의 십이지장궤양 환자 증가가 크게 기여하고 있으며, 종종 영양 불량, 알코올 섭취, 흡연 습관이 관련되어 있습니다. 고령자는 소화관 합병증에 걸리기 쉽기 때문에 고령화도 치료 솔루션의 수요 증가에 기여하고 있습니다. H2 수용체 길항제나 양성자 펌프 저해제(PPI) 등의 약제는 그 확실한 산 억제 능력 및 양호한 안전성 프로파일로 사용량이 증가하고 있습니다.

많은 치료 계획에서 십이지장궤양의 주요 원인인 헬리코박터 파일로리 감염을 표적으로 하는 항생제와 함께 사용됩니다. 또한 수크랄파트나 미소프로스톨과 같은 약제는 위 점막의 보호 작용으로 인기를 끌고 있습니다. AI 진단, 모바일 헬스 도구, 원격 의료의 통합은 접근성과 환자 중심의 치료에 초점을 맞추어 궤양 치료 제공 방법을 재구축하고 있습니다. 디지털 헬스 모델 및 예방 전략을 채택하는 헬스케어 시스템이 늘어나면서 신뢰성 높은 십이지장궤양 치료에 대한 수요는 모든 지역에서 계속 확대되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 32억 달러 |

| 예측 금액 | 52억 달러 |

| CAGR | 5.1% |

약리 요법 부문은 2024년에 28억 달러를 창출했습니다. 이 우위성은 PPI나 H2 블로커와 같은 약제 클래스별이 신속한 증상완화와 일관된 산 컨트롤에 효과적인 것에 기인합니다. 이러한 약제는 사용 편의성, 경구 투여, 전체적인 편리성 때문에 널리 선호되고 있으며, 재택 케어나 환자의 장기적인 애드히어런스를 지탱하고 있습니다. 침습적인 처치 없이 효과적으로 증상을 관리할 수 있는 것으로부터, 헬스케어 프로바이더 및 환자 양쪽 모두에게 있어서 첫번째 선택이 되어, 이 치료 카테고리의 성장을 뒷받침하고 있습니다.

노년 의료 분야는 2024년에 58.7%의 점유율을 차지했습니다. 노화에 따른 소화관 보호 기능의 저하는 노인의 궤양 형성에 대한 취약성을 증대시키고 노인을 치료 옵션의 주요 소비자 그룹으로 하고 있습니다. 게다가 다른 노화 관련 질환의 치료를 위해 비스테로이드성 항염증제(NSAIDs)를 만성적으로 사용하는 것은 이 층에서 십이지장궤양의 위험을 현저히 높입니다. 이와 같이 궤양 형성의 유인에 지속적으로 노출됨에 따라 고령 환자에 맞춘 장기적이고 예방적인 케어 접근이 요구되고 있습니다.

미국의 십이지장궤양 치료 2025년 시장 규모는 15억 3,000만 달러로 추정됩니다. 미국 시장은 헬리코박터 파일로리 감염의 유병률 증가, 비스테로이드성 항염증제(NSAID)의 빈번한 사용, 식생활의 위험 인자에 의해 성장을 계속하고 있습니다. 이 나라에서는 조기 발견이 중시되어, 제대로 된 치료 프로토콜이 시기적절한 진단과 개입을 지지하고 있습니다. 헬스케어 제공의 강력한 인프라스트럭처는 광범위한 계발 캠페인과 최첨단 진단 서비스에 대한 액세스와 함께 높은 치료 보급률을 보장하고 있습니다. 치료 연구와 기술 혁신에 대한 지속적인 투자도 세계 정세를 형성하는 데 있어 이 나라의 역할을 강화하고 있습니다.

이 시장의 주요 업계 기업은 Takeda Pharmaceutical, Abbott Laboratories, Boehringer Ingelheim, Cipla, Eisai, GlaxoSmithKline, Pfizer, Merck, Lupin, Novartis, Ferozsons Laboratories, Sun Pharma, Sanofi 및 AstraZeneca 등이 있습니다. 시장 포지션을 강화하기 위해 십이지장궤양 치료 영역에서 사업을 전개하는 기업은 다양한 전략적 이니셔티브를 실시했습니다. 대증요법과 헬리코박터 파일로리균과 같은 근본 원인을 모두 타깃으로 한 선진적인 의약품 개발에 대한 투자는 중요한 초점이 되고 있습니다.

많은 기업들은 파트너십, 현지 제조 및 지역 마케팅 전략을 통해 세계 전개를 강화하고 있습니다. 스마트 모니터링 및 원격 의료 대응 치료와 같은 디지털 건강 통합은 환자 참여와 어드히어런스를 높이기 위해 검토되고 있습니다. 또한 기업은 효율성과 컴플라이언스를 향상시키기 위해 병용 요법을 포함한 포트폴리오의 다양화를 추진하고 있습니다. 전략적 가격 설정, 환자 지원 프로그램 및 의사의 교육 캠페인도 보다 광범위한 시장 침투를 지원합니다.

The Global Duodenal Ulcer Treatment Market was valued at USD 3.2 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 5.2 billion by 2034. This growth is largely fueled by rising cases of duodenal ulcers worldwide, often linked to poor nutrition, alcohol intake, and smoking habits. An aging population also contributes to increased demand for treatment solutions, as older individuals are more susceptible to gastrointestinal complications. Medications such as H2 receptor blockers and proton pump inhibitors (PPIs) are seeing heightened usage due to their reliable acid-suppressing abilities and favorable safety profiles.

In many treatment plans, these are now used in conjunction with antibiotics that target Helicobacter pylori infections- a leading cause of duodenal ulcers. Additionally, agents like sucralfate and misoprostol are gaining traction for their protective effects on the gastric lining. The integration of AI diagnostics, mobile health tools, and telemedicine is reshaping how ulcer care is delivered, with a focus on accessibility and patient-centered treatment. As more healthcare systems adopt digital health models and preventive strategies, the demand for reliable duodenal ulcer treatments continues to grow across all regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 Billion |

| Forecast Value | $5.2 Billion |

| CAGR | 5.1% |

The pharmacological therapies segment generated USD 2.8 billion in 2024. This dominance stems from the effectiveness of drug classes like PPIs and H2 blockers in providing quick symptom relief and consistent acid control. These medications are widely preferred for their ease of use, oral delivery, and overall convenience, which support home-based care and long-term patient adherence. Their ability to manage symptoms effectively without invasive procedures makes them the first choice for both healthcare providers and patients, pushing growth in this treatment category.

The geriatrics segment held a 58.7% share in 2024. Age-related declines in gastrointestinal protection increase vulnerability to ulcer formation among older adults, making them the primary consumer group for treatment options. Additionally, chronic use of non-steroidal anti-inflammatory drugs (NSAIDs) to manage other age-related conditions significantly raises the risk of duodenal ulcers in this demographic. This persistent exposure to ulcerogenic triggers calls for long-term and preventive care approaches tailored to senior patients.

United States Duodenal Ulcer Treatment Market was valued at USD 1.53 billion in 2025. The American market continues to grow due to the increasing prevalence of Helicobacter pylori infections, frequent NSAID use, and dietary risk factors. The country's emphasis on early detection and robust treatment protocols supports timely diagnosis and intervention. Strong infrastructure in healthcare delivery, along with extensive awareness campaigns and access to cutting-edge diagnostic services, ensures high treatment adoption. Ongoing investments in therapeutic research and innovation also bolster the country's role in shaping the global duodenal ulcer treatment landscape.

Key industry players in this market include Takeda Pharmaceutical, Abbott Laboratories, Boehringer Ingelheim, Cipla, Eisai, GlaxoSmithKline, Pfizer, Merck, Lupin, Novartis, Ferozsons Laboratories, Sun Pharma, Sanofi, and AstraZeneca. To strengthen their market position, companies operating in the duodenal ulcer treatment space are embracing various strategic initiatives. Investment in advanced drug development targeting both symptom management and root causes, such as Helicobacter pylori, is a key focus.

Many firms are enhancing their global reach through partnerships, local manufacturing, and regional marketing strategies. Digital health integration, such as smart monitoring and telehealth-enabled treatment, is being explored to boost patient engagement and adherence. Additionally, firms are diversifying portfolios to include combination therapies, aiming to improve efficacy and compliance. Strategic pricing, patient assistance programs, and physician education campaigns also support broader market penetration.