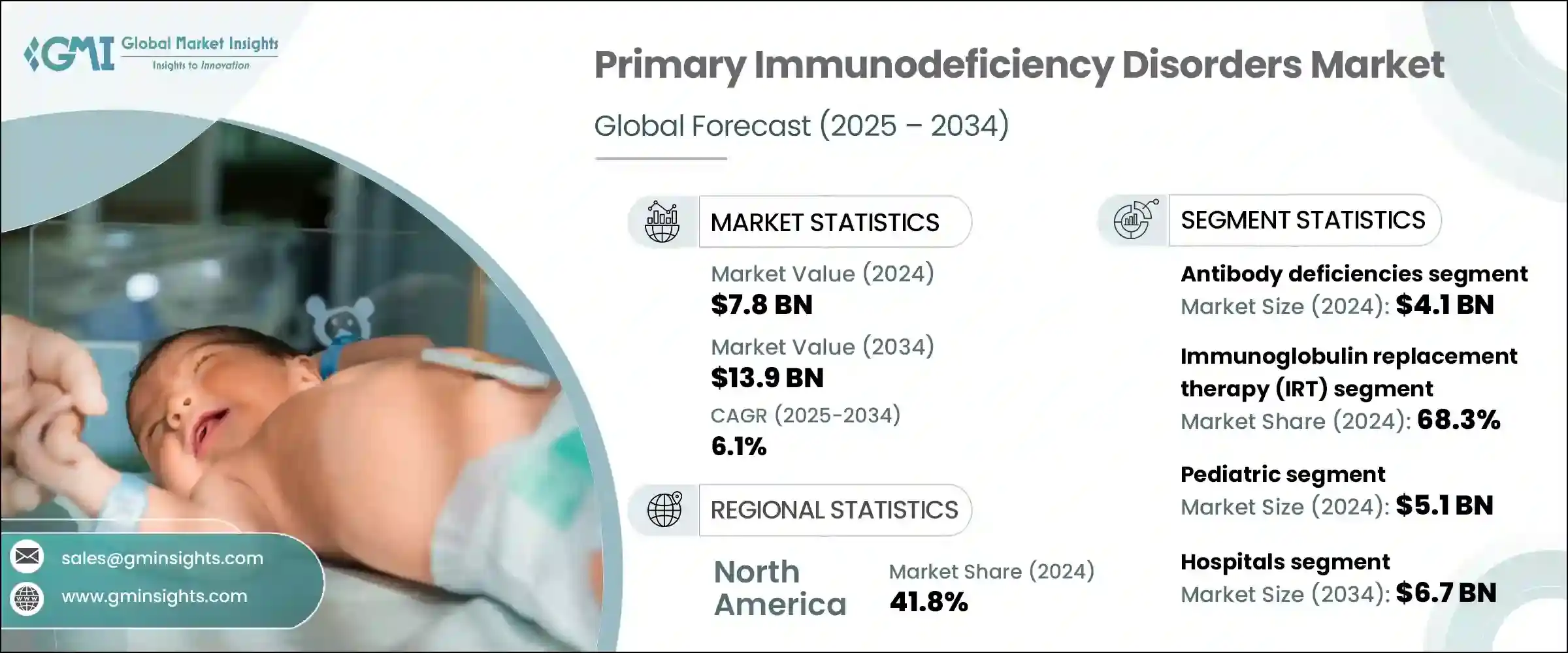

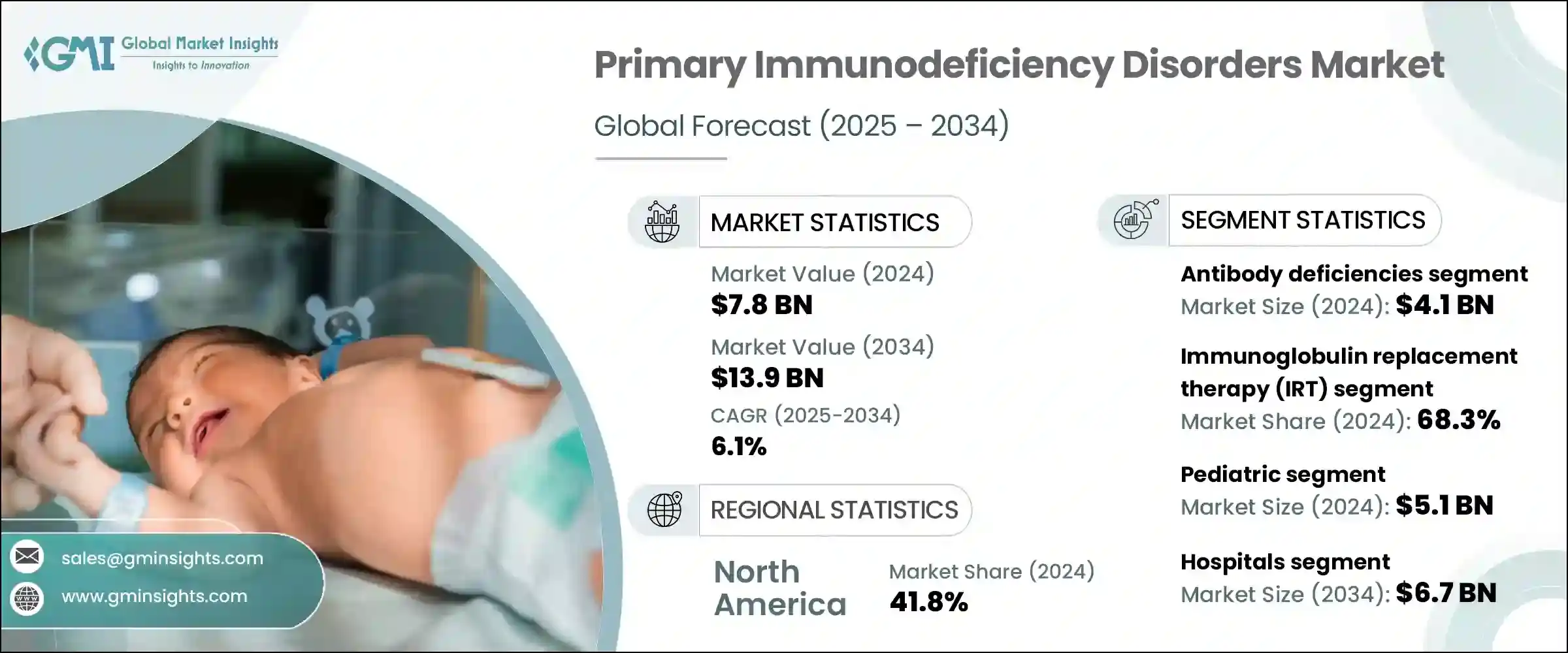

세계의 원발성 면역 부전증 시장은 2024년에는 78억 달러로 평가되며, CAGR 6.1%로 성장하며, 2034년에는 139억 달러에 달할 것으로 예측됩니다.

이러한 성장의 주요 요인은 원발성 면역결핍증(PIDs)의 발생률 증가와 의료진과 환자들 사이에서 이러한 질환에 대한 인식이 높아진 것이 주요 요인으로 작용하고 있습니다. 진단 접근법과 유전자 기반 치료 및 생물제제와 같은 치료 혁신의 발전으로 효과적인 치료 및 관리의 기회가 확대되고 있습니다. 연구개발에 대한 투자가 강화되고 희귀 유전질환에 대한 인식이 높아짐에 따라 정확한 진단과 보다 타겟팅된 치료에 대한 접근성이 향상되고 있습니다. 의료 시스템이 희귀질환을 보다 종합적으로 관리할 수 있도록 진화함에 따라 조기 개입, 맞춤 치료, 지속적인 모니터링을 통해 환자들은 더 나은 치료 결과와 삶의 질 향상이라는 혜택을 누리고 있습니다.

의료진들의 면역학 교육이 지속적으로 향상되고 있으며, 면역 결핍증이 의심되는 환자를 조기에 발견하고 개입할 수 있게 되었습니다. 환자 지원 단체와 커뮤니티 지원 그룹은 환자를 의료 네트워크로 연결하고 의료 정책의 체계적인 변화를 추진하는 데 중요한 역할을 하고 있습니다. 이러한 광범위한 참여는 PID의 발견과 분류를 지원하기 위해 전 세계에서 채택되고 있는 유전자 염기서열 분석 및 유세포분석과 같은 첨단 진단 툴에 대한 접근성을 향상시키는 데 도움이 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024 |

| 예측연도 | 2025-2034 |

| 시작 금액 | 78억 달러 |

| 예측 금액 | 139억 달러 |

| CAGR | 6.1% |

남아공, 브라질, 인도, 중국 등 개발도상국의 가처분 소득 증가와 함께 도시화가 진행되면서 더 나은 의료 서비스를 받을 수 있게 되면서 사람들은 의료 진단을 받고 적절한 치료를 받게 되었습니다. 원발성 면역 결핍증은 감염, 만성질환 및 전반적인 면역 기능 저하로 인한 취약성을 초래하는 유전성 면역계 질환입니다. 치료법의 혁신은 면역력을 향상시키고 증상을 완화하며 질병의 재발을 최소화하는 데 초점을 맞추었습니다.

2024년에는 항체 결핍 분야가 41억 달러 규모로 가장 큰 시장 부문을 차지했습니다. 이러한 우위는 항체 생산 장애와 관련된 면역 질환의 높은 유병률에 기인합니다. 가장 흔한 것은 평생 치료가 필요한 심각한 감염을 자주 유발하는 면역 결핍증입니다. 이러한 환자들은 일반적으로 정맥 또는 피하 주사를 통한 정기적인 면역글로불린 요법이 필요하며, 이는 제품 수요의 지속적 증가에 기여하고 있습니다. 현재 진행 중인 의학의 발전으로 보다 효율적이고 환자 친화적인 투여 시스템이 확보되고 있으며, 이 부문의 성장 잠재력이 확대되고 있습니다.

치료 분야에서는 면역글로불린 대체요법(IRT) 분야가 2024년 68.3%의 점유율을 차지하고 있습니다. 대부분의 항체 관련 면역결핍증에 대한 표준 치료 프로토콜로서 IRT에 대한 의존도가 높아지면서 이 분야 시장 점유율이 증가하고 있습니다. 이러한 치료법은 감염으로부터 장기적으로 보호하며, 이러한 평생 질환을 관리하는 데 필수적입니다. 반감기 연장, 재조합 기술 등 최근 치료제의 개선으로 치료 효과와 환자 편의성이 더욱 향상되고 있습니다. 또한 인식과 지지도가 높아지면서 조기 치료 시작과 치료 순응도가 향상되고 있으며, 이는 이 시장의 성장을 직접적으로 지원하고 있습니다. 의료 서비스 프로바이더들은 이제 IRT를 PID 치료의 기본 치료법으로 인식하고 있으며, IRT가 더 널리 받아들여지고 사용되고 있습니다.

미국 원발성 면역결핍증 시장 규모는 2024년 29억 달러에 달했습니다. 미국은 탄탄한 의료 인프라, 첨단 진단법 보급, 면역결핍증에 대한 높은 국민적 및 임상적 인식으로 세계 시장을 선도하고 있습니다. 면역 프로파일링, 유세포분석, 첨단 유전자 검사 등의 진단 툴은 특히 소아 PID 사례의 확인 및 분류에 널리 사용되고 있습니다. 유전자 편집 기술 및 줄기세포 치료와 같은 최첨단 치료법이 가능해짐에 따라 미국 환자들은 전 세계에서 가장 혁신적인 치료법을 이용할 수 있게 되었습니다. 전문 클리닉, 면역학 전문 병원, 재택치료 제공 모델 등이 시장 성숙에 기여하고 있습니다. 표적 생물제제, 차세대 면역글로불린, 희귀질환에 대한 새로운 치료법에 대한 강력한 연구 투자가 시장의 진화를 주도하고 있습니다.

원발성 면역 부전증 시장의 주요 기업에는 Orchard Therapeutics, Miltenyi Biotec, CSL Behring, Baxter International, Medac, Octapharma, ADMA Biologics, Takeda Pharmaceutical, F. Hoffmann La Roche, Bluebird Bio, Biotest (Grifol Group), Avanos, Leadiant Biosciences. 등이 있습니다. 원발성 면역결핍증 시장에서 사업을 전개하는 기업은 시장에서의 입지를 강화하기 위해 몇 가지 전략을 추구하고 있습니다.

그 중 하나는 표적 생물제제, 유전자 치료제, 생체이용률을 높이고 투여 횟수를 줄이는 차세대 면역글로불린 치료제를 위한 첨단 R&D 파이프라인에 대한 투자입니다. 또한 평생 면역글로불린 대체요법에 대한 수요 증가에 대응하기 위해 생산 능력을 확장하고 있습니다. 학술기관 및 연구센터와의 전략적 제휴를 통해 새로운 기술 및 새로운 적응증에 대한 접근성을 확보하고 있습니다. 특히 진단에 대한 인식이 높아지고 있는 신흥 국가 지역에서 지역적 확장을 통해 시장 침투를 도모하고 있습니다.

The Global Primary Immunodeficiency Disorders Market was valued at USD 7.8 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 13.9 billion by 2034. This growth is primarily driven by the rising incidence of primary immunodeficiency disorders (PIDs) and the increasing recognition of these conditions among medical professionals and patients. Advancements in both diagnostic approaches and therapeutic innovations, such as gene-based therapies and biologics, are creating expanded opportunities for effective treatment and management. Enhanced investment in research and development, coupled with growing awareness of these rare genetic disorders, is improving access to accurate diagnoses and more targeted care. As healthcare systems evolve to address rare conditions more holistically, patients are benefiting from better outcomes and improved quality of life through early intervention, personalized therapies, and continuous monitoring.

Training in immunology continues to improve among healthcare providers, allowing earlier identification and intervention for patients with suspected immunodeficiency disorders. Patient advocacy organizations and community support groups are playing a crucial role in connecting individuals to care networks and pushing for systemic changes in healthcare policy. This broader engagement is helping increase access to advanced diagnostic tools, such as genetic sequencing and flow cytometry, which are being adopted globally to aid in detecting and classifying PIDs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.8 Billion |

| Forecast Value | $13.9 Billion |

| CAGR | 6.1% |

The rise of urbanization and access to better healthcare services, along with increasing disposable incomes in developing regions such as South Africa, Brazil, India, and China, is encouraging people to seek medical evaluations and pursue proper treatment. Primary immunodeficiency disorders are inherited immune system conditions that lead to higher vulnerability to infections, chronic illnesses, and overall weakened immune function. Treatment innovations are focused on improving immunity, alleviating symptoms, and minimizing disease recurrence.

The antibody deficiencies segment represented the largest market segment in 2024, with a valuation of USD 4.1 billion. This dominance stems from the high prevalence of immune disorders linked to impaired antibody production. Among the most common are immunodeficiencies that result in frequent, severe infections requiring lifelong therapy. Patients with these conditions typically need regular immunoglobulin therapy administered through intravenous or subcutaneous methods, which contributes to sustained product demand. Ongoing medical advancements are ensuring more efficient and patient-friendly delivery systems, expanding this segment's growth potential.

In terms of treatment, the immunoglobulin replacement therapy (IRT) segment held a 68.3% share in 2024. The continued reliance on IRT as a standard care protocol for most antibody-related immunodeficiencies reinforces its strong market presence. These therapies offer long-term protection from infections, which is essential in managing these lifelong conditions. Recent improvements in treatment formulations, including options with extended half-lives and recombinant technology, are further increasing therapy effectiveness and patient comfort. Additionally, greater awareness and advocacy support early treatment initiation and improved adherence, which directly supports this market's expansion. Healthcare providers now recognize IRT as a cornerstone therapy in PID treatment, prompting its broader acceptance and usage.

U.S. Primary Immunodeficiency Disorders Market was valued at USD 2.9 billion in 2024. The country leads the global market with a robust healthcare infrastructure, widespread adoption of advanced diagnostics, and strong public and clinical awareness of immunodeficiency disorders. Diagnostic tools, including immune profiling, flow cytometry, and advanced genetic testing, are widely used to confirm and classify PID cases, especially among children. The availability of cutting-edge therapies such as gene editing technologies and stem cell-based interventions is giving U.S. patients access to some of the most innovative treatments globally. Specialized clinics, immunology-focused hospitals, and home-based care delivery models have all contributed to market maturity. Strong research investments in targeted biologics, next-generation immunoglobulins, and novel therapies for rare diseases continue to shape the market's evolution.

Leading companies in the Primary Immunodeficiency Disorders Market include Orchard Therapeutics, Miltenyi Biotec, CSL Behring, Baxter International, Medac, Octapharma, ADMA Biologics, Takeda Pharmaceutical, F. Hoffmann La Roche, Bluebird Bio, Biotest (Grifol Group), Avanos, and Leadiant Biosciences. Companies operating in the primary immunodeficiency disorders market are pursuing several strategies to enhance their market presence.

One major focus is investing in advanced R&D pipelines for targeted biologics, gene therapies, and next-gen immunoglobulin therapies with enhanced bioavailability and reduced administration frequency. Firms are also expanding manufacturing capabilities to meet the growing demand for lifelong immunoglobulin replacement therapies. Strategic collaborations with academic institutions and research centers allow access to emerging technologies and new indications. Companies are increasing market penetration through geographic expansion, especially in developing regions with rising diagnostic awareness.