Modified Bitumen Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1773462

리서치사:Global Market Insights Inc.

발행일:2025년 06월

페이지 정보:영문 220 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

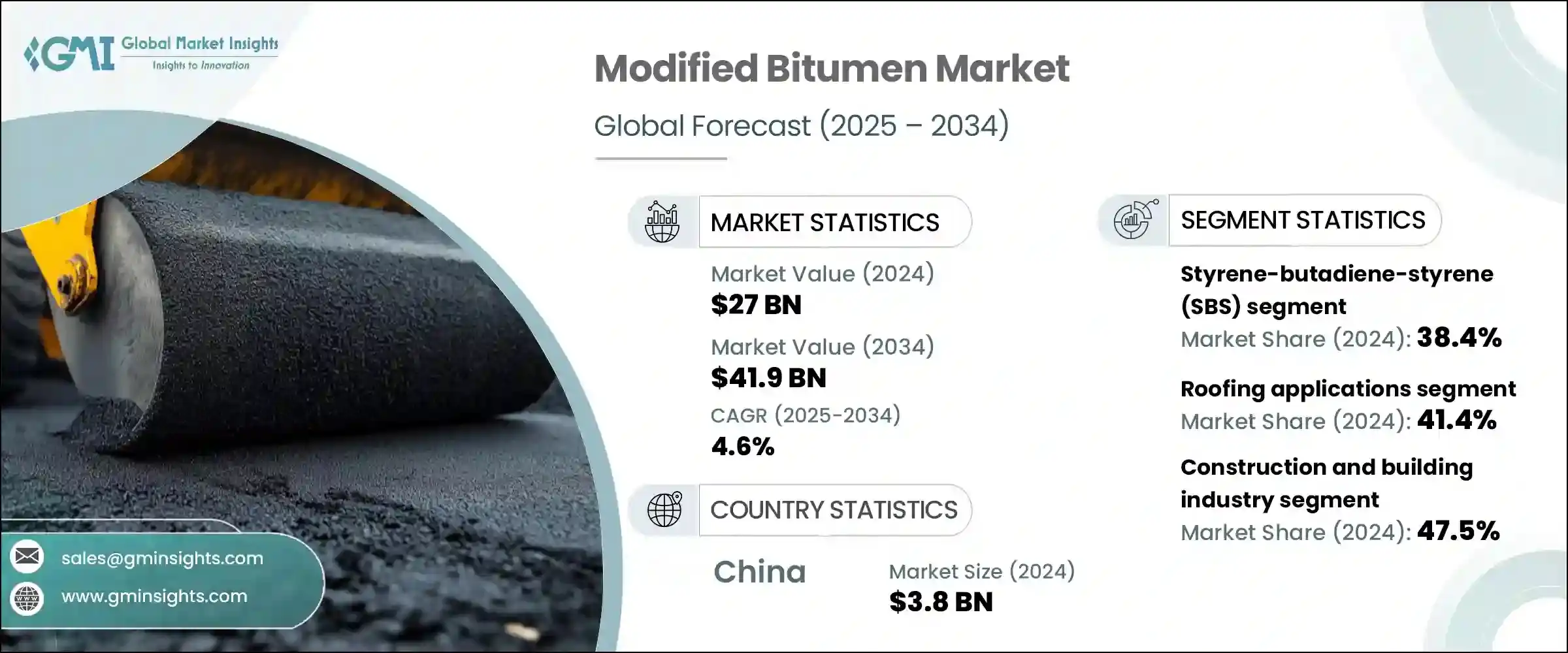

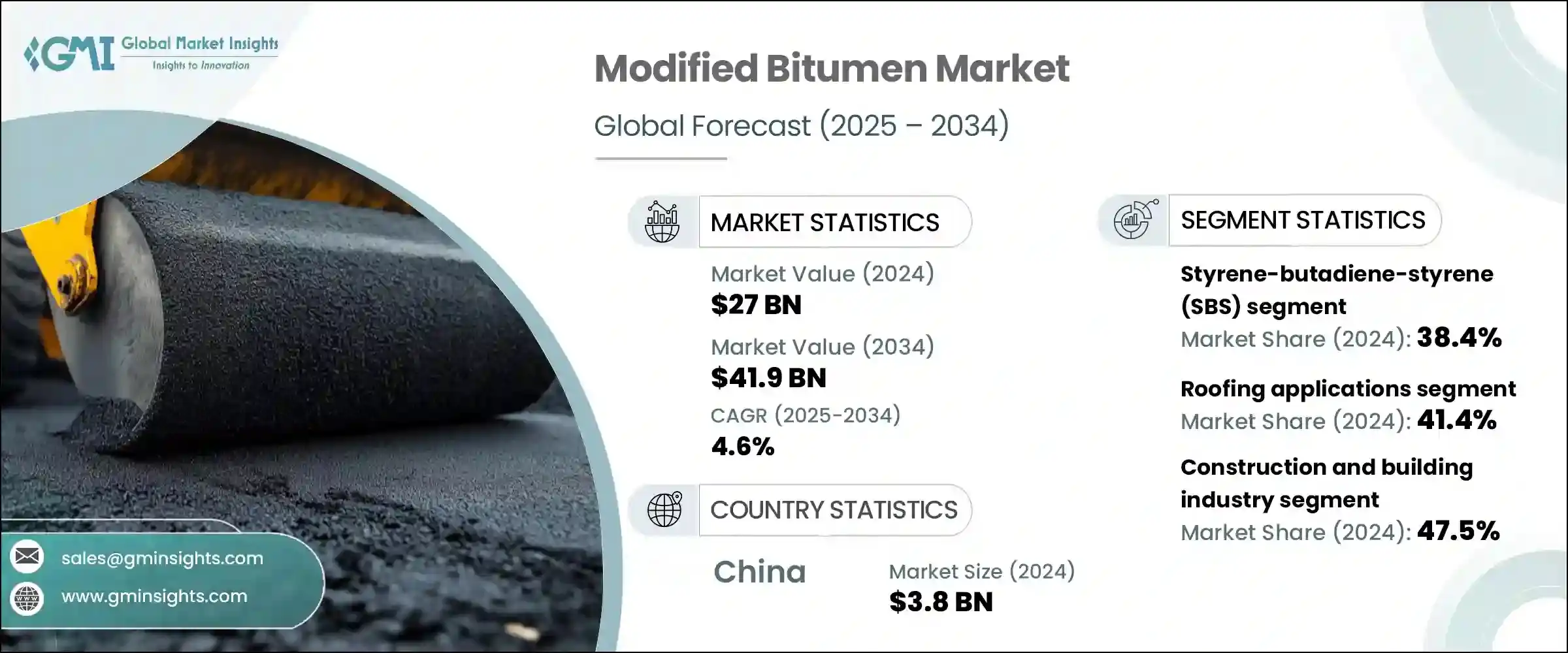

세계의 개질 아스팔트 시장은 2024년에 270억 달러로 평가되며, CAGR 4.6%로 성장하며, 2034년에는 419억 달러에 달할 것으로 추정되고 있습니다.

세계 건설 부문이 지붕과 포장재 모두에서 고성능, 오래 지속되는 재료에 중점을 두면서 강화 아스팔트 배합에 대한 수요가 꾸준히 증가하고 있습니다. 가혹한 환경 조건을 견딜 수 있는 도로 및 인프라에 대한 필요성이 증가함에 따라 탄력성과 내구성을 향상시킨 개질 바인더의 채택이 가속화되고 있습니다. 또한 기후에 대한 적응성이 강조되면서 열변동, 균열, 산화에 대한 저항성이 뛰어난 아스팔트 사용을 촉진하고 있습니다. 업계 사업자들은 교통량이 많은 곳이나 혹독한 기상 조건에서 성능 요건을 충족하기 위해 폴리머 개질제를 선택하게 되었습니다. 또한 지속가능한 인프라 개발에 대한 인식이 높아짐에 따라 제조업체들은 환경 기준을 충족하고 건설 활동으로 인한 탄소 배출량을 줄이는 재료를 생산하도록 유도하고 있습니다.

세계 각국 정부가 인프라 구축에 대한 야심찬 목표를 설정함에 따라 정유업체와 아스팔트 제조업체는 고성능 등급의 생산 능력을 확대해야 할 필요성이 대두되고 있습니다. 공공 및 민간 부문 프로젝트에서 재료 선택은 점점 더 기후 변화를 고려한 엔지니어링 기준과 수명주기 비용 평가에 따라 결정되고 있습니다. 개질 아스팔트는 가혹한 조건에서도 성능을 유지할 수 있으므로 장기적인 가치와 유지보수 감소를 원하는 프로젝트에서 선호되는 선택이 되고 있습니다. 바인더 화학의 혁신은 향상된 탄성, 우수한 온도 안정성, 높은 자외선 저항성을 나타내는 폴리머 배합의 개발에 기여하고 있습니다. 이러한 특성은 포장과 지붕의 수명을 연장하고 인프라 투자의 전반적인 비용 효율성에 기여합니다. 그 결과, 이 소재는 현대적이고 지속가능한 건설 방식에 대한 투자 증가에 힘입어 장기적인 교통 및 도시 개발 계획에 필수적인 요소로 자리 잡고 있습니다.

시장 범위

시작연도

2024

예측연도

2025-2034

시작 금액

270억 달러

예측 금액

419억 달러

CAGR

4.6%

이 시장의 성장을 지원하는 것은 배출량 감소와 건설 투입물의 순환성을 촉진하기 위한 엄격한 규제 변화도 한 몫을 하고 있습니다. 개질 아스팔트 재생 고무 및 저배출 폴리머와 같은 친환경 재료를 배합한 블렌드는 정부가 그린 빌딩 인증을 시행하고 기후 변화에 강한 도시화를 장려하면서 지지를 받고 있습니다. 특히 폴리머를 개질한 제품은 성능과 지속가능성 목표의 균형을 맞춘 대안에 대한 수요가 급증하고 있습니다. 혼합 적합성, 저온 포장 솔루션, 탄소 저감 첨가제에 초점을 맞춘 연구 노력이 계속되고 있으며, 이는 모두 재료 선택에 있으며, 환경적 고려가 점점 더 큰 영향을 미치고 있음을 반영하고 있습니다. 이러한 진화하는 상황 속에서 제조업체들은 고성능의 친환경 배합을 재구성하여 지속가능성 프레임워크를 준수하면서 보다 광범위한 인프라의 요구를 충족시킬 수 있도록 대응하고 있습니다.

시장에서 사용되는 다양한 개질제 중 스티렌-부타디엔-스티렌(SBS)은 탄성, 내피로성, 내열성 및 내열성을 향상시키는 능력으로 인해 계속해서 우위를 차지하고 있습니다. 이러한 특성으로 인해 SBS 개질 바인더는 잦은 온도 변화와 차량 하중이 큰 열악한 환경에 특히 적합하며, SBS 개질 바인더는 변형과 균열을 줄여 표면의 내구성을 크게 향상시켜 궁극적으로 도로 및 지붕 시스템의 수명을 연장시킵니다. 신축 및 개보수 프로젝트에서 선호되는 선택이 되고 있으며, 다양한 지역 시장에서 SBS의 존재감을 높이고 있습니다.

개질 아스팔트는 용도별로 도로 건설 및 포장, 지붕재, 방수 및 실링, 산업 및 특수 용도로 구분됩니다. 지붕재 용도는 내후성과 에너지 효율이 우수한 건축자재에 대한 수요 증가에 힘입어 2024년 세계 시장 점유율의 41.4%를 차지했습니다. SBS와 공격적 폴리프로필렌(APP)을 지붕 막에 사용하면 유연성과 자외선 열화에 대한 내성이 강화되어 현대 도시 건축에 이상적입니다. 특히 도시화가 빠르게 진행되는 지역에서는 상업 및 주택 건설이 꾸준히 증가함에 따라 지붕재가 이러한 첨단 소재로 전환되고 있습니다. 향상된 단열 특성과 엄격한 건축법 준수에 따라 개질 루핑 필름은 선진국과 신흥 경제국에서 인기가 높아지고 있습니다.

제조 기술도 제품의 품질과 적응성에 영향을 미칩니다. 특히 점도 및 탄성과 같은 특정 성능 기준을 충족해야하는 맞춤형 수량 및 배합의 경우, 배치 공정은 여전히 폴리머 개질 아스팔트 생산에 널리 사용되고 있습니다. 이 방법을 통해 생산자는 다양한 지역의 요구와 특수 프로젝트의 요구에 보다 유연하게 대응할 수 있습니다. 특히 연구개발 용도 및 배합 조정이 필요한 소량 생산 프로젝트에 특히 유용합니다.

아시아태평양은 세계 개질 아스팔트 시장에서 선도적인 위치를 차지하고 있으며, 그 원동력은 견고한 건설 활동, 교통에 대한 투자 확대, 도시 확장의 진전에 기인하고 있습니다. 이 지역 국가들은 인프라 개보수 및 신규 개발에 많은 투자를 하고 있으며, 이는 성능개질 표면처리재에 대한 안정적인 수요를 견인하고 있습니다. 이 지역 시장 상승 모멘텀은 정부 지원과 대규모 교통 및 주택 프로젝트 증가로 인해 강화되고 있으며, 이 모든 것은 고품질의 탄력적인 투입물에 의존하고 있습니다.

세계 시장의 주요 기업에는 Shell Global, TotalEnergies SE, ExxonMobil Corporation, Nynas AB, Kraton Corporation이 포함됩니다. 이들 기업은 다양한 환경 및 교통 조건에 맞게 설계된 SBS, APP 및 하이브리드 변성 제품의 광범위한 포트폴리오를 통해 강력한 입지를 유지하고 있습니다. 제품 배합, 기술 지원 및 공급 안정성에 대한 전문성을 바탕으로 대규모 인프라 및 산업 프로젝트에서 선호되는 공급업체로 자리매김하고 있습니다. 또한 이들 기업은 환경에 미치는 영향을 줄이기 위한 바이오 개질제, 재생 재료 호환성 및 차세대 바인더를 개발하여 지속가능성으로의 전환을 주도하고 있습니다. 지속적인 연구개발과 저탄소 혁신에 대한 노력을 통해 이들 기업은 내구성이 뛰어나고 기후 변화에 강한 재료에 대한 세계 수요를 충족시키면서 개질 아스팔트 기술의 미래를 만들어가고 있습니다.

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

에코시스템 분석

공급업체의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 미치는 요인

파괴적 변화

업계에 대한 영향요인

촉진요인

인프라 개발과 도시화의 진전

기후 레질리언스와 이상 기상에 대한 적응

지속가능성 의무와 환경 규제

퍼포먼스의 향상과 수명주기 비용 최적화

업계의 잠재적 리스크 & 과제

높은 초기 비용과 경제적 장벽(60- 70% 프리미엄)

보관 안정성과 취급 복잡성

숙련 설치 작업원이 한정되어 있다.

원재료 가격의 변동과 공급망 의존성

시장 기회

신흥 시장과 인프라 투자 프로그램

바이오 기반과 재활용 폴리머 통합

스마트 인프라와 IoT 통합

재해에 강한 건설 요건

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter의 산업 분석

PESTEL 분석

가격 동향

지역별

제품별

향후 시장 동향

테크놀러지와 혁신의 상황

현재 기술 동향

신규 기술

특허 상황

무역통계(HS 코드)(주 : 무역통계는 주요 국가만 제공)

주요 수입국

주요 수출국

지속가능성과 환경 측면

지속가능 실천

폐기물 삭감 전략

생산에서의 에너지 효율

친환경 구상

탄소발자국 고려

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카 항공

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병과 인수

파트너십과 협업

신제품 발매

확장 계획

제5장 시장 추산·예측 : 폴리머 개질제의 유형별, 2021-2034

주요 동향

스티렌-부타디엔-스티렌(SBS) 개질 아스팔트

SBS 폴리머 등급과 사양

APP(Atactic polypropylene) 개질 아스팔트

에틸렌초산비닐(EVA) 개질 아스팔트

열가소성 엘라스토머(TPE) 및 기타 개질제

바이오 기반 및 재활용 폴리머 개질제

하이브리드 및 멀티 폴리머 시스템

SBS-APP 복합 제품

폴리머 고무 하이브리드 개질

제6장 시장 추산·예측 : 용도별, 2021-2034

주요 동향

지붕재 용도

저구배 및 평지붕 시스템

상업 및 산업용 건물에 대한 응용

다층 시스템 구성과 퍼포먼스

급경사 지붕에 대한 적용

주택 지붕

기초재와 ICE 댐 보호

싱글과 타일 통합 시스템

도로 건설과 포장

고속도로 및 주간 고속도로 애플리케이션

도시 및 지방자치단체 도로 시스템

시가지 도로 및 간선도로에 대한 응용

교차점 및 고응력 존 솔루션

정비 및 재활 프로젝트

공항 및 산업용 포장

방수 및 실링 용도

지하 방수 시스템

파운데이션 및 지하실 애플리케이션

터널 및 지하 구조물 보호

교량상판 및 인프라 방수

지상 방수 솔루션

플라자 데크와 발코니 시스템

초록 지붕과 정원 애플리케이션

주차장 구조와 포디움 데크 보호

산업 및 특수용도

접착제와 실란트

코팅과 보호 시스템

파이프 코팅과 부식 방지

제7장 시장 추산·예측 : 최종 용도 산업별, 2021-2034

주요 동향

건설·건축업계

주택 건설 시장

단독주택과 집합주택

개수·개축 프로젝트

에너지 효율과 그린 빌딩 요건

상업 건설 부문

오피스 빌딩과 소매 센터

헬스케어·교육 시설

접객(Hoapitality)과 엔터테인먼트 회장

산업 건설 애플리케이션

제조 및 가공 시설

창고 및 배송센터

데이터센터와 테크놀러지 인프라

교통 인프라

고속도로와 도로 인프라

주 사이 고속도로 시스템의 유지보수

주 및 지방 도로망

교량·고가 건설

공항 인프라 개발

활주로 및 터미널 확장 프로젝트

화물 시설 개발

항만·해양 인프라

컨테이너 터미널 및 부두 건설

연안 보호 및 방파제 프로젝트

에너지 및 유틸리티 부문

발전시설

태양광발전소와 풍력에너지 인프라

기존 발전소 정비

석유 및 가스 인프라

정제 및 처리 시설 애플리케이션

파이프라인과 저장탱크의 보호

수처리 및 폐수 처리

치료 시설 인프라

저수지 및 저장 시설 방수

정부와 공공 인프라

연방정부 및 주 정부의 프로젝트

시읍면 및 지방자치단체용 애플리케이션

군 및 방위 인프라

프라이빗 시장과 전문 시장

스포츠·레크리에이션 시설

농업 및 농촌 인프라

광업 및 채굴 산업

제8장 시장 추산·예측 : 지역별, 2021-2034

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽 지역

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

기타 라틴아메리카 지역

중동 및 아프리카

사우디아라비아

남아프리카공화국

아랍에미리트

기타 중동 및 아프리카 지역

제9장 기업 개요

CertainTeed Corporation

Colas Group

Dynasol Group

Ergon Inc.

ExxonMobil Corporation

Johns Manville

Kraton Corporation

LG Chem Ltd

MBTechnology

Nynas AB

Polyglass U.S.A., Inc

Shell Global

Siplast(Icopal Group)

TotalEnergies SE

Versalis S.p.A

KSA

영문 목차

영문목차

The Global Modified Bitumen Market was valued at USD 27 billion in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 41.9 billion by 2034. The demand for enhanced bitumen formulations is steadily rising as the construction sector worldwide shifts focus toward high-performance, long-lasting materials for both roofing and paving. The increasing necessity for roads and infrastructure that can withstand harsh environmental conditions has fueled the adoption of modified binders with improved resilience and durability. A growing emphasis on climate adaptability has also prompted the use of bitumen variants that offer better resistance to thermal fluctuations, cracking, and oxidation. Industry operators are increasingly selecting polymer-modified alternatives to meet the performance requirements of high-traffic areas and challenging weather zones. In addition, growing awareness around sustainable infrastructure development is motivating manufacturers to produce materials that align with environmental standards and reduce the carbon impact of construction activities.

Governments in many parts of the world are pursuing ambitious infrastructure goals, prompting refiners and bitumen producers to expand their capacity for high-performance grades. Material choices in public and private sector projects are increasingly guided by climate-conscious engineering standards and lifecycle cost assessments. Modified bitumen's capacity to retain performance under extreme conditions has made it a preferred option for projects demanding long-term value and lower maintenance. Innovations in binder chemistry have contributed to the development of polymer formulations that exhibit improved elasticity, superior temperature stability, and higher UV resistance. These characteristics extend the life of pavements and roofing systems and contribute to the overall cost-efficiency of infrastructure investments. As a result, the material is becoming integral to long-term transportation and urban development plans, supported by rising investment in modern, sustainable construction practices.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$27 Billion

Forecast Value

$41.9 Billion

CAGR

4.6%

The market's growth is also supported by stringent regulatory shifts aimed at reducing emissions and promoting circularity in construction inputs. Modified bitumen blends incorporating eco-conscious materials-such as recycled rubber or low-emission polymers-are gaining traction as governments enforce green building certifications and encourage climate-resilient urbanization. Polymer-modified variants are especially prominent, with demand surging for options that balance performance with sustainability goals. Research efforts continue to focus on blending compatibility, low-temperature paving solutions, and carbon-reducing additives, all of which reflect the growing influence of environmental considerations on material selection. In this evolving landscape, manufacturers are responding by reengineering formulations that are both high performing and eco-friendly, allowing them to cater to a broader range of infrastructure needs while complying with sustainability frameworks.

Among the various modifiers used in the market, Styrene-Butadiene-Styrene (SBS) continues to dominate due to its ability to enhance elasticity, fatigue resistance, and temperature tolerance. These properties make SBS-modified binders particularly suitable for demanding environments with frequent temperature changes or heavy vehicular load. SBS modifications significantly improve surface durability by reducing deformation and cracking, ultimately extending the service life of roads and roofing systems. Its mechanical performance makes it a preferred choice in both new construction and rehabilitation projects, which helps explain its strong presence across diverse regional markets.

Modified bitumen is segmented by application into road construction and paving, roofing, waterproofing and sealing, and industrial and specialty uses. Roofing applications accounted for 41.4% of the global market share in 2024, driven by increasing demand for weather-resistant and energy-efficient building materials. The use of SBS and Atactic Polypropylene (APP) in roofing membranes enhances flexibility and resistance to UV degradation, making them ideal for modern urban buildings. The steady rise in commercial and residential construction, especially in regions undergoing rapid urbanization, has supported the shift toward these advanced materials in roofing systems. Enhanced insulation properties and compliance with stricter building codes have made modified roofing membranes increasingly popular in both developed and developing economies.

Manufacturing techniques also influence product quality and adaptability. The batch process remains widely used for producing polymer-modified bitumen, particularly for customized volumes or formulations where specific performance criteria-such as viscosity or elasticity-must be met. This method allows producers to respond to varying regional requirements and specialty project demands with more flexibility. It is especially beneficial for R&D applications or lower-volume projects where formulation adjustments are necessary.

Asia Pacific continues to hold a leading position in the global modified bitumen market, driven by robust construction activity, growing investments in transportation, and rising urban expansion. Countries across the region are investing heavily in infrastructure upgrades and new development, driving consistent demand for performance-modified surfacing materials. The market's upward momentum in the region is reinforced by government-backed initiatives and a growing number of large-scale transport and housing projects, all of which rely on high-quality, resilient inputs.

Key players in the global market include Shell Global, TotalEnergies SE, ExxonMobil Corporation, Nynas AB, and Kraton Corporation. These companies maintain a strong presence through a wide-ranging portfolio of SBS, APP, and hybrid-modified products designed for varying environmental and traffic conditions. Their expertise in product formulation, technical support, and supply reliability positions them as preferred suppliers for large infrastructure and industrial projects. These firms are also leading the shift toward sustainability by developing bio-based modifiers, recycled content compatibility, and next-generation binders aimed at reducing environmental impact. Through ongoing R&D and a focus on low-carbon innovations, these companies continue to shape the future of modified bitumen technologies while meeting global demand for durable, climate-resilient materials.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Polymer modified type

2.2.3 Application

2.2.4 End use industry

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Infrastructure development and urbanization growth

3.2.1.2 Climate resilience and extreme weather adaptation

3.2.1.3 Sustainability mandates and environmental regulations

3.2.1.4 Performance enhancement and lifecycle cost optimization

3.2.2 Industry pitfalls and challenges

3.2.2.1 High initial costs and economic barriers (60-70% premium)

3.2.2.2 Storage stability and handling complexities

3.2.2.3 Limited skilled installation workforce

3.2.2.4 Raw material price volatility and supply chain dependencies

3.2.3 Market opportunities

3.2.3.1 Emerging markets and infrastructure investment programs

3.2.3.2 Bio-based and recycled polymer integration

3.2.3.3 Smart infrastructure and IoT integration

3.2.3.4 Disaster-resilient construction requirements

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.6.1 Technology and Innovation Landscape

3.6.2 Current technological trends

3.6.3 Emerging technologies

3.7 Price trends

3.7.1 By region

3.7.2 By product

3.8 Future market trends

3.9 Technology and Innovation Landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and Environmental Aspects

3.12.1 Sustainable Practices

3.12.2 Waste Reduction Strategies

3.12.3 Energy Efficiency in Production

3.12.4 Eco-friendly Initiatives

3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New Product Launches

4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Polymer Modifier Type, 2021 - 2034 (USD Billion) (Kilo Tons)