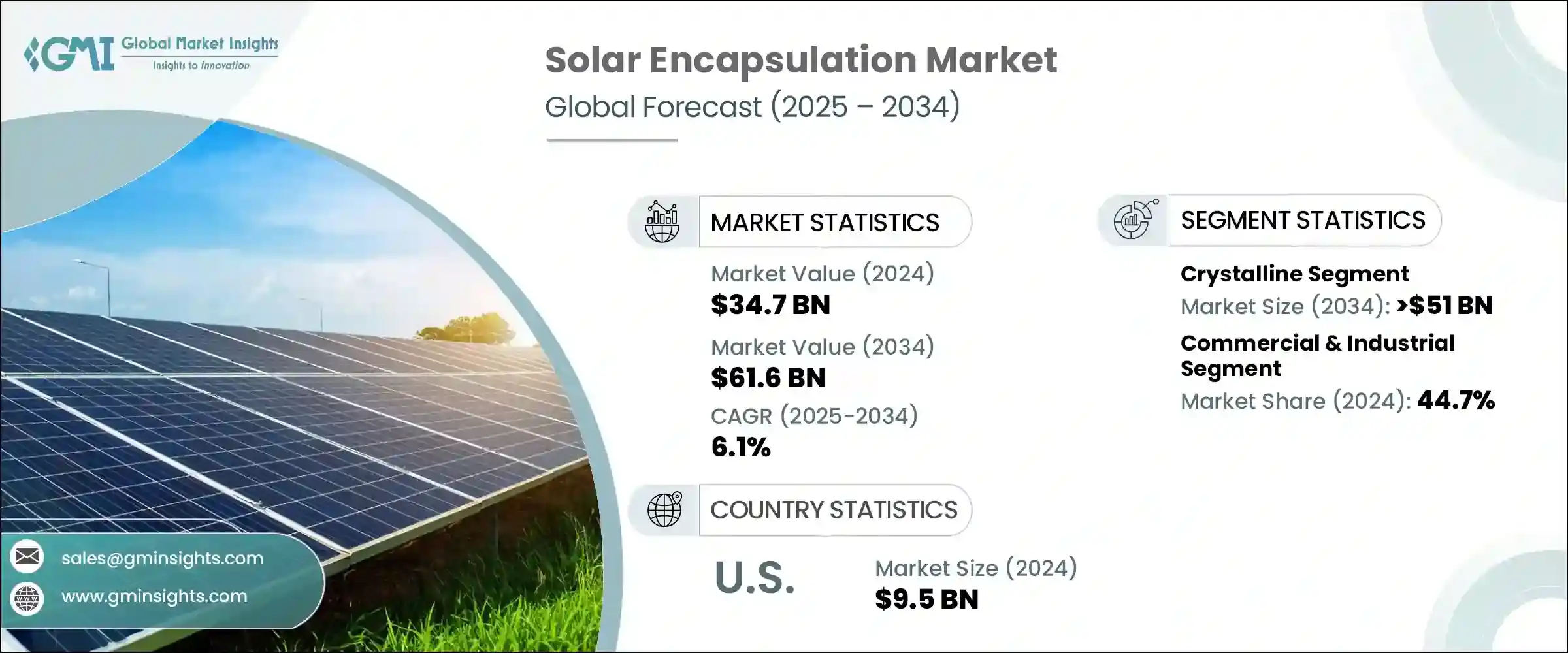

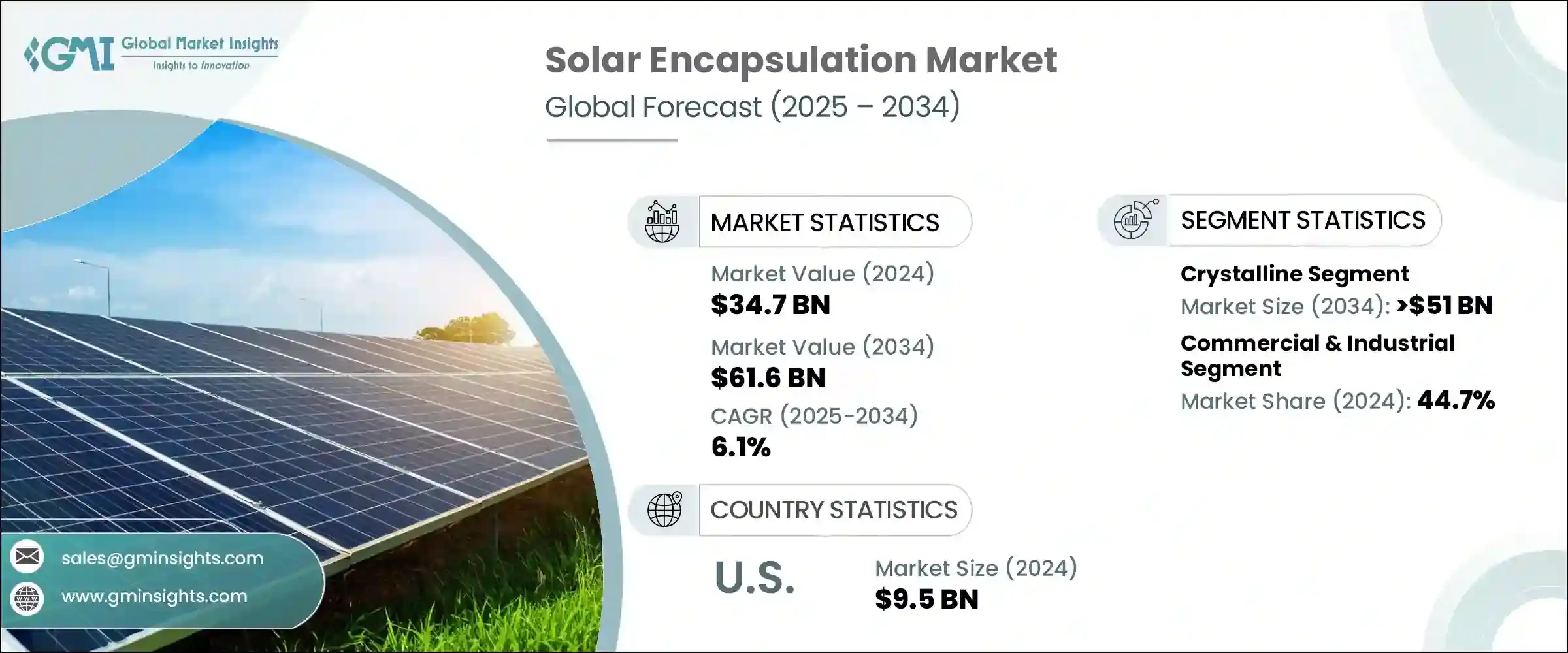

세계의 태앙전지용 봉지재 시장은 2024년에 347억 달러로 평가되었고, CAGR 6.1%로 성장하여 2034년에는 616억 달러에 이를 것으로 추정되고 있습니다.

이러한 상승 추세는 정부의 우호적인 정책에 힘입어 국내 태양광 제조에 대한 세계 각국의 적극적인 지원에 힘입은 바가 큽니다. 세계 각국은 수입 태양광 부품에 대한 의존도를 줄이기 위해 인센티브 기반 프레임워크를 도입하여 봉지재와 같은 핵심 재료의 국내 생산을 강화하고 있습니다. 이러한 재료는 태양전지를 환경 노출로부터 보호하고, 패널의 수명을 연장하고, 전반적인 성능을 향상시키는 데 중요한 역할을 합니다. 주거용, 상업용, 공공시설 규모의 프로젝트에서 태양광 발전의 도입이 증가함에 따라 기존 태양광 경제권 및 신흥 경제권에서 신뢰할 수 있는 고품질 봉지재에 대한 필요성이 점점 더 커지고 있습니다.

특히 태양광 모듈 생산이 급성장하고 있는 시장에서는 급증하는 수요에 대응하기 위해 업체들이 사업을 확장하고 있습니다. 선진국과 신흥국 모두 공급망 간소화에 중점을 두면서 태양광 모듈의 현지 생산을 지원하는 인프라에 많은 투자를 하고 있습니다. 이러한 변화는 모듈의 장기적인 효율성과 내구성을 보장하는 데 핵심적인 봉지 재료의 소비를 크게 증가시키고 있습니다. 이러한 추세는 대규모 생산을 위해 봉지재에 대한 안정적인 접근을 필요로 하는 수직 통합형 태양광 기업들이 증가하면서 더욱 강화되고 있습니다. 이러한 기업들이 원자재 조달 및 모듈 조립을 포함한 가치사슬 관리를 강화함에 따라 안정적이고 일관된 봉지재 공급에 대한 수요가 증가하여 향후 몇 년 동안 시장 역학에 긍정적인 영향을 미칠 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 개시 금액 | 347억 달러 |

| 예측 금액 | 616억 달러 |

| CAGR | 6.1% |

결정질 패널 부문은 2034년까지 510억 달러 이상의 매출을 기록할 것으로 예측됩니다. 이러한 패널은 비용 효율성과 표준 봉지 기술과의 호환성으로 인해 계속해서 시장을 지배하고 있습니다. 결정질 모듈은 일반적으로 EVA 기반 봉지재와 결합되어 저렴한 가격으로 충분한 자외선 차단 및 내열성을 제공합니다. 구조가 비교적 간단하고 다양한 태양전지 응용 분야에서 주류로 자리 잡았기 때문에 기존 라미네이트 재료에 이상적으로 적합하여 봉지재 시장의 성장을 더욱 촉진하고 있습니다.

용도별로는 상업 및 산업 분야가 2024년 태양광 발전용 봉지재 세계 시장 점유율의 44.7%를 차지했습니다. 이 분야가 두드러지는 이유는 특히 대규모 설치에서 고성능 태양광 모듈의 도입이 증가하고 있기 때문입니다. 이러한 프로젝트에는 가혹한 사용 조건을 견디면서 장기간 우수한 효율을 달성할 수 있는 고도의 밀봉 시스템이 요구되는 경우가 많습니다. 상업용 태양광 발전 설비가 엄격한 성능 기준에 직면하면서 신뢰성, 열 제어 및 열화 저항성을 강화한 혁신적인 밀봉재에 대한 수요가 증가하고 있습니다.

지역별로는 북미 시장이 2024년 29.8%의 점유율을 차지했으며, 미국이 압도적인 역할을 했습니다. 미국의 태양광 발전용 봉지재 시장 규모는 2022년 47억 달러, 2023년 76억 달러, 2024년 95억 달러에 달했습니다. 이러한 성장을 뒷받침하는 주요 요인은 봉지재 제조에 중점을 둔 견고한 국내 태양전지 공급망 개발에 대한 연방 정부의 이니셔티브에 기인합니다. 실리콘 기반 기술과 박막 기술 모두에서 태양전지 부품 생산을 강화하기 위한 국가적 이니셔티브는 고성능 봉지재의 폭넓은 채택에 기여하고 있습니다. 이러한 시장 개척은 봉지재 분야의 기존 기업과 신규 진출기업 모두에게 큰 시장 기회를 제공할 것으로 예측됩니다.

이 분야에서 사업을 전개하는 주요 기업들은 시장 지위를 확보하기 위해 다양한 전략을 구사하고 있습니다. 생산 능력을 확장하고, EVA 필름 및 POE 필름의 자체 생산에 투자하고, 최고 수준의 태양전지 모듈 제조업체와 강력한 파트너십을 맺고 있습니다. 또한 지역 시장에 맞게 제품을 조정하고, 폴리머 공급업체와 후방 통합하고, 재료의 내구성과 자외선 저항성을 향상시키기 위한 연구개발을 강화하는 데 주력하고 있습니다. 이를 통해 비용 경쟁력을 유지하면서 진화하는 성능 기준을 충족하는 밀봉재를 확보할 수 있습니다.

주요 봉지재 제조업체들은 모듈 효율을 높이기 위해 투명성 및 PID 저항과 같은 재료 특성의 혁신을 우선순위에 두고 있습니다. 동시에 물류 개선과 리드 타임 단축을 위해 현지에 제조 거점을 구축하고 있습니다. 수직 통합 모듈 제조업체와의 전략적 제휴는 이들 기업이 시장에서의 입지를 강화하고 공급망의 안정성을 향상시키는 데 도움이 되고 있습니다. 그들의 노력은 필름 압출 성형 능력 확대, 라미네이션 기술 최적화, IEC 및 BIS와 같은 국제 인증 표준을 준수하는 데까지 확대되고 있으며, 이는 모두 세계 경쟁 환경에서 장기적인 경쟁력을 유지하는 데 필수적인 요소입니다.

The Global Solar Encapsulation Market was valued at USD 34.7 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 61.6 billion by 2034. This upward trend is largely driven by the global pivot toward domestic solar manufacturing, supported by favorable government policies. Countries across the globe are introducing incentive-based frameworks to reduce dependency on imported photovoltaic components, thereby bolstering local production of critical materials such as encapsulants. These materials play a vital role in safeguarding solar cells from environmental exposure, prolonging panel life, and enhancing overall performance. As solar adoption continues to gain ground in residential, commercial, and utility-scale projects, the need for reliable, high-quality encapsulation materials is becoming increasingly essential across both established and emerging solar economies.

Manufacturers are scaling up their operations to meet the surging demand, particularly in markets where solar module production is expanding rapidly. Both developed and developing countries are investing heavily in infrastructure that supports the local manufacturing of solar modules, with a strong focus on streamlining the supply chain. This shift is encouraging significant growth in the consumption of encapsulation materials, which are key to ensuring long-term module efficiency and durability. The trend is further reinforced by the growing number of vertically integrated solar companies that require dependable access to encapsulants for large-scale production. As these companies consolidate control over the value chain, including raw material sourcing and module assembly, their demand for stable and consistent encapsulation supply is expected to grow, positively influencing market dynamics over the coming years.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $34.7 Billion |

| Forecast Value | $61.6 Billion |

| CAGR | 6.1% |

The crystalline panel segment is anticipated to generate over USD 51 billion in revenue by 2034. These panels continue to dominate the market due to their cost-effectiveness and compatibility with standard encapsulation techniques. Crystalline modules are commonly paired with EVA-based encapsulants, which offer adequate UV protection and thermal resistance at affordable rates. Their relatively simple structure and mainstream adoption across various solar applications make them an ideal fit for conventional lamination materials, further supporting encapsulant market growth.

Within the application landscape, the commercial and industrial sector accounted for 44.7% of the global solar encapsulation market share in 2024. The segment's prominence is attributed to the rising deployment of high-performance solar modules, particularly in large-scale installations. These projects often require advanced encapsulation systems capable of withstanding harsh operating conditions while delivering superior efficiency over time. As commercial solar installations face rigorous performance standards, demand is growing for innovative encapsulants that offer enhanced reliability, thermal control, and resistance to degradation.

In regional terms, the North American market held a 29.8% share in 2024, with the U.S. playing a dominant role. The solar encapsulation market in the United States was valued at USD 4.7 billion in 2022, USD 7.6 billion in 2023, and USD 9.5 billion in 2024. A key factor supporting this growth is the federal commitment to developing a robust domestic solar supply chain, with specific emphasis on encapsulant manufacturing. National initiatives aimed at strengthening the production of solar components across both silicon-based and thin-film technologies are contributing to the broader adoption of high-performance encapsulation materials. These developments are expected to create strong market opportunities for both established players and new entrants in the encapsulant space.

Major companies operating in this sector are leveraging a combination of strategies to secure their market position. They are expanding their production capacities, investing in in-house manufacturing of EVA and POE films, and forming strong partnerships with top-tier solar module producers. Many are also focusing on tailoring products for regional markets, integrating backward with polymer suppliers, and intensifying their research and development efforts to improve material durability and UV resistance. This helps ensure their encapsulants meet evolving performance standards while remaining cost-competitive.

Leading encapsulant producers are also prioritizing innovation in material properties such as transparency and PID resistance to enhance module efficiency. At the same time, they are building localized manufacturing hubs to improve logistics and reduce lead times. Strategic agreements with vertically integrated module manufacturers are helping these companies boost their market presence and improve supply chain stability. Their efforts also extend to scaling up film extrusion capabilities, optimizing lamination technologies, and ensuring compliance with international certification standards such as IEC and BIS, all of which are instrumental in maintaining long-term competitiveness in the global solar encapsulation landscape.