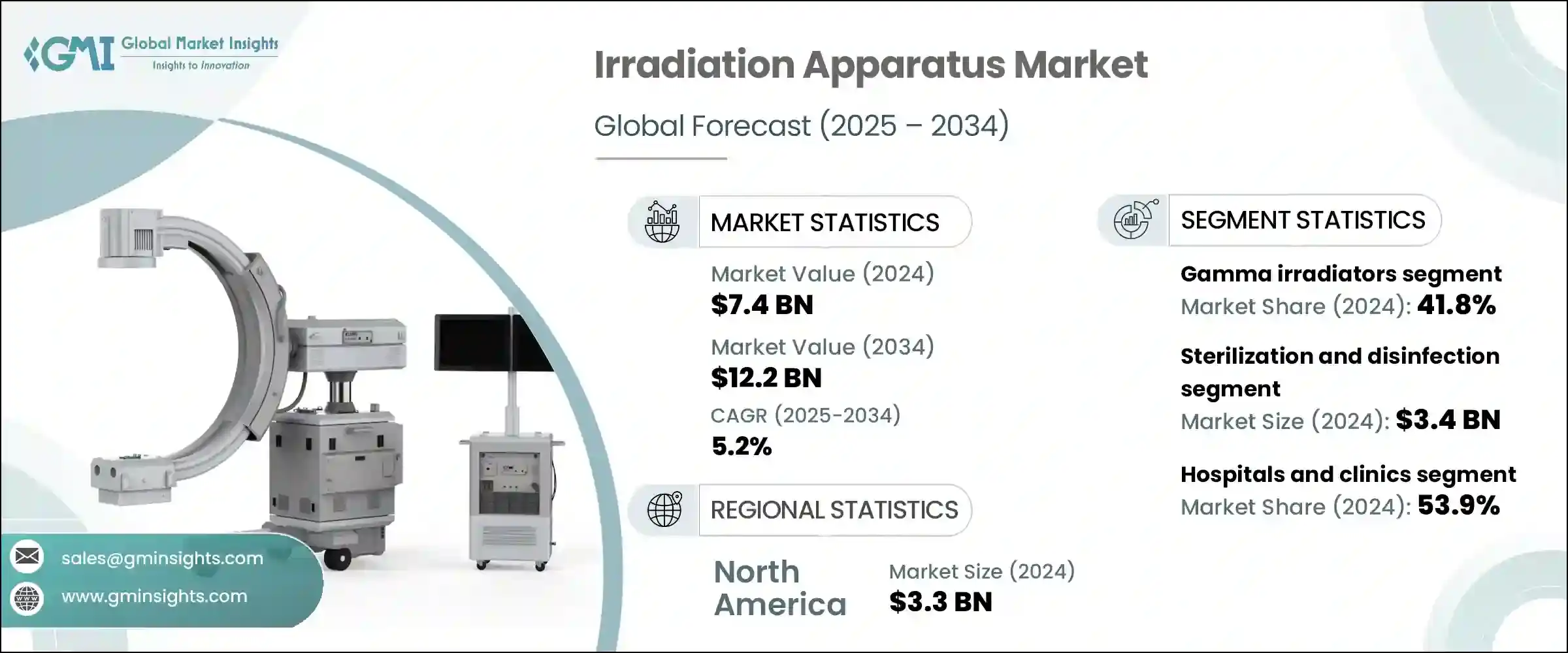

조사 장치 세계 시장은 2024년에는 74억 달러로 평가되었고, CAGR 5.2%로 성장하여 2034년에는 122억 달러에 이를 것으로 추정되고 있습니다.

이러한 성장을 주도하는 것은 의료용과 산업용 모두에서 이온화 방사선과 비이온화 방사선의 이용이 증가하고 있기 때문입니다. 이러한 시스템은 주로 진단, 치료, 멸균, 연구 목적으로 도입되고 있습니다.

암 치료에서 방사선 치료의 채택이 증가하고 있는 것은 시장 성장을 가속하는 중요한 요인입니다. 조기 발견 및 즉각적인 개입에 대한 강력한 추진력으로 인해 방사선 치료 장비 및 리니어락과 같은 장비에 대한 투자가 증가하고 있습니다. 전 세계적으로 종양 클리닉과 전문 의료 센터가 확대됨에 따라 첨단 방사선 조사 시스템의 도입이 지속적으로 증가하고 있으며, 효율적이고 접근하기 쉬운 암 치료 기술에 대한 수요가 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 개시 금액 | 74억 달러 |

| 예측 금액 | 122억 달러 |

| CAGR | 5.2% |

영상 유도 방사선 치료와 AI 지원 시스템의 최신 기술 혁신은 방사선 조사 장치의 전망을 재구성하고 있습니다. 로봇 제어 및 실시간 영상 처리와 통합된 이들 플랫폼은 주변 조직을 보호하면서 종양에 정확한 선량을 조사했습니다. 리니어릭 및 영상 유도 방사선 치료와 같은 기술은 현재 더 높은 정확도와 합병증 위험 감소를 실현하여 의료시설에서 널리 사용되고 있습니다.

치료 결과 개선, 회복 시간 단축, 부작용 최소화는 병원 및 클리닉의 차세대 시스템으로의 전환을 촉진하고 있습니다. 신흥 지역에서는 공공 및 민간 부문의 투자 확대가 의료 인프라 업그레이드를 지원하고 치료 접근성 격차를 해소하는 데 기여하고 있습니다. 치료 및 멸균 분야 모두에서 방사선 기반 솔루션에 대한 수요가 증가함에 따라 세계 시장은 헬스케어 개혁과 기술 주도적 개선으로 활성화되고 있습니다.

2024년에는 감마선 조사기 부문이 41.8%로 가장 큰 시장 점유율을 차지했습니다. 일회용 의료 제품의 소비 확대는 감마선 기반 멸균 시스템의 큰 원동력이 되고 있습니다. 감마선은 열에 약하고 화학적으로 민감한 품목을 효과적으로 멸균할 수 있기 때문에 주사기, 카테터, 수술용 장갑의 멸균에 이 방식을 채택하는 제조업체가 증가하고 있습니다.

감마선을 이용한 멸균 처리는 유해한 잔류물을 남기지 않기 때문에 규제된 의료 환경에서 신뢰할 수 있는 솔루션을 제공합니다. 이러한 시스템은 수혈 후 부작용을 예방하기 위해 혈액 성분을 처리하는 데에도 필수적입니다. 전 세계 규제 기관이 감염 관리와 무균성 보장을 강조하는 가운데 감마선 조사 장치는 중요한 의료기기 및 소모품의 제조 및 가공에 있어 선호되는 솔루션으로 자리매김하고 있습니다.

2024년 시장 점유율은 병원 및 클리닉이 53.9%로 가장 큰 비중을 차지했습니다. 이들 기관은 방사선 조사 장치의 주요 사용자로서 영상 진단 및 치료 중재에 광범위하게 활용하고 있으며, 엑스레이 장비, CT 시스템, 투시 장비와 같은 장비는 환자의 상태를 비침습적으로 평가하는 데 매우 중요한 역할을 하고 있습니다.

또한, 의료 관련 감염과 싸우기 위해 병원은 침습적 의료기기의 방사선 기반 멸균에 주목하여 환자의 안전과 위생 규정 준수를 보장하고 있습니다. 열이나 화학 물질에 의한 멸균에 비해 방사선 조사는 수술 기구 및 기타 재사용 가능한 부품의 멸균에 더 빠르고 신뢰할 수 있는 방법을 제공합니다. 진단 정확도와 감염 예방의 조합으로 인해 방사선 조사 장치는 현대 의료시설에 없어서는 안 될 필수 요소로 자리 잡았습니다.

미국 방사선 조사 장치 시장은 2024년 30억 달러로 평가되었고, 2034년에는 49억 달러에 달할 것으로 예측됩니다. 만성 질환, 특히 암의 확산으로 인해 전국적으로 첨단 방사선 치료 솔루션에 대한 수요가 증가하고 있습니다. 동시에 외래수술센터(ASC) 및 외래 진료소와 같은 분산형 치료 환경을 중시하는 미국 헬스케어 업계에서는 작고 효율적인 멸균 시스템에 대한 요구가 가속화되고 있습니다.

이러한 소규모 시설에서는 높은 처리량과 공간 절약형 솔루션이 요구되고 있으며, 모듈식 방사선 조사 시스템은 속도, 신뢰성 및 장비 무결성 유지 능력으로 인해 매우 매력적입니다. 이러한 비용 효율적인 분산형 헬스케어 모델로의 전환으로 조사 기술은 도시와 농촌 지역 모두에서 강력한 성장세를 유지할 것으로 예측됩니다.

방사선 조사 장치 분야의 주요 기업들은 첨단 영상 유도 시스템 및 AI 통합형 방사선 시스템을 통해 제품 포트폴리오를 확장하는 데 주력하고 있습니다. 많은 기업들이 치료의 정확성을 높이고, 워크플로우를 자동화하고, 안전성을 높이기 위해 연구개발에 많은 투자를 하고 있습니다. 암 치료 센터 및 의료 기관과의 협업은 진화하는 임상적 요구에 맞는 맞춤형 솔루션을 제공하는 데 도움이 되고 있습니다. 전 세계 수요, 특히 서비스가 부족한 지역 수요에 대응하기 위해, 기업들은 설치의 복잡성을 줄여주는 모듈식, 비용 효율적인 시스템을 개발하고 있습니다.

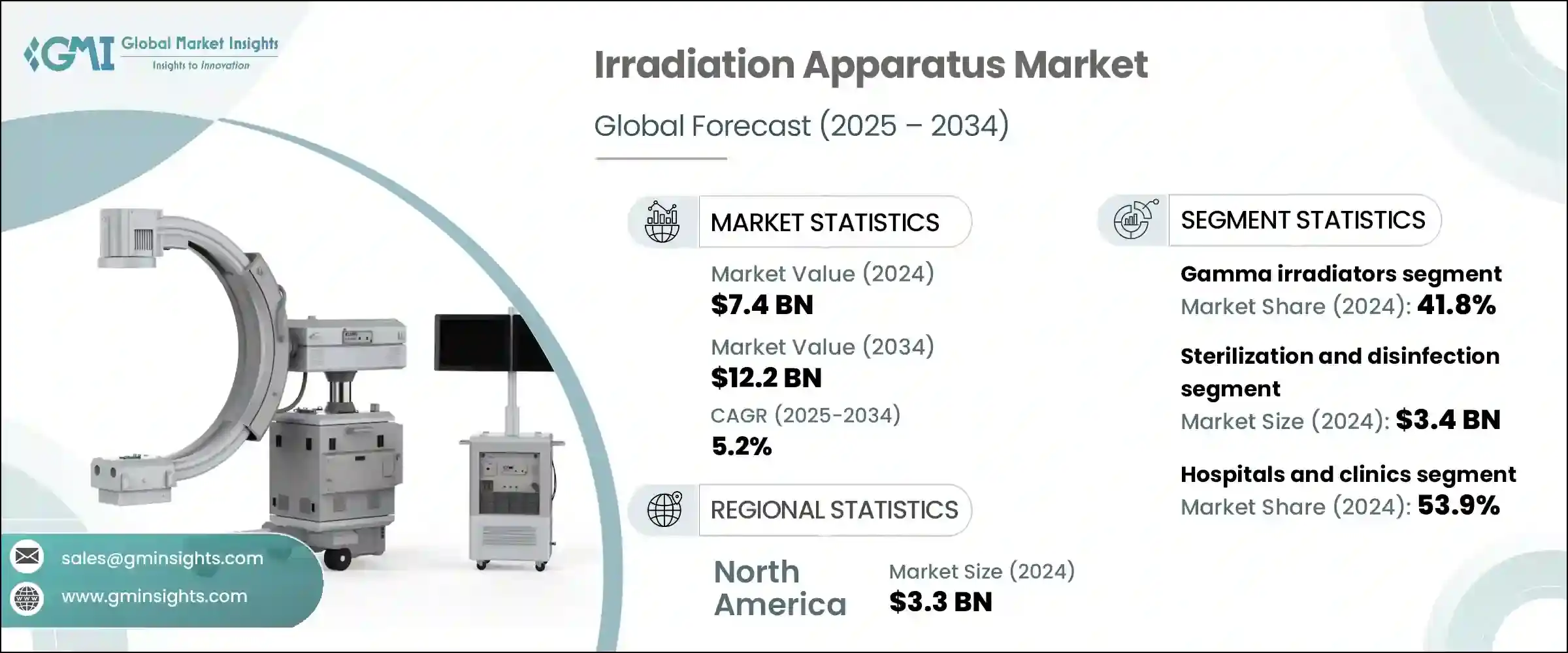

The Global Irradiation Apparatus Market was valued at USD 7.4 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 12.2 billion by 2034. This growth is driven by the increasing utilization of ionizing and non-ionizing radiation across both medical and industrial applications. These systems are primarily deployed for diagnostics, therapeutic use, sterilization, and research purposes.

The rising adoption of radiotherapy in cancer care is a significant factor propelling the market growth, as precision-targeted irradiation systems improve both outcomes and patient experiences. A strong push toward early detection and immediate intervention is increasing investments in devices such as brachytherapy equipment and linear accelerators. With oncology clinics and specialized medical centers expanding globally, the adoption of advanced irradiation systems continues to rise, underscoring the demand for efficient and accessible cancer treatment technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.4 Billion |

| Forecast Value | $12.2 Billion |

| CAGR | 5.2% |

Modern innovations in image-guided radiation therapy and AI-enabled systems are reshaping the landscape of irradiation apparatus. Integrated with robotic control and real-time imaging, these platforms provide accurate dose delivery to tumors while safeguarding surrounding tissues. Technologies such as linear accelerators and image-guided radiotherapy are now delivering higher levels of precision and lower complication risks, leading to widespread adoption across healthcare facilities.

Enhanced therapeutic outcomes, reduced recovery times, and minimized side effects are encouraging hospitals and clinics to transition to next-generation systems. In emerging regions, increased investments from both public and private sectors are supporting healthcare infrastructure upgrades, helping close treatment accessibility gaps. As demand grows for radiation-based solutions in both treatment and sterilization, the global market is being fueled by healthcare reforms and technology-driven improvements.

In 2024, the gamma irradiator segment accounted for the largest market share at 41.8%. The growing consumption of disposable medical products has been a major driver for gamma-based sterilization systems. As gamma radiation enables effective sterilization of heat-sensitive and chemically delicate items, manufacturers are increasingly relying on this method for syringes, catheters, and surgical gloves.

Sterilization processes using gamma rays leave no harmful residue, offering a reliable solution in regulated medical environments. These systems are also essential in treating blood components to prevent adverse post-transfusion reactions. With infection control and sterility assurance gaining focus across global regulatory bodies, gamma irradiators continue to be a preferred solution in the manufacture and processing of critical healthcare equipment and supplies.

The hospitals and clinics segment led the market in 2024 with a share of 53.9%. These facilities are primary users of irradiation apparatus, utilizing them extensively for diagnostic imaging and therapeutic interventions. Equipment like X-ray units, CT systems, and fluoroscopy machines play a pivotal role in evaluating patient conditions non-invasively.

Moreover, to combat healthcare-associated infections, hospitals are turning to irradiation-based sterilization for invasive medical tools, ensuring both patient safety and compliance with hygiene regulations. Compared to heat or chemical alternatives, irradiation offers a faster and more dependable method for sterilizing surgical instruments and other reusable components. The combination of diagnostic accuracy and infection prevention is making irradiation apparatus indispensable across modern healthcare facilities.

U.S. Irradiation Apparatus Market was valued at USD 3 billion in 2024 and is estimated to reach USD 4.9 billion by 2034. A growing prevalence of chronic illnesses-particularly cancer-is pushing demand for advanced radiation therapy solutions across the country. In tandem, the U.S. healthcare industry's emphasis on decentralized treatment settings like ambulatory surgical centers and outpatient clinics is accelerating the need for compact, efficient sterilization systems.

As these smaller facilities look for high-throughput and space-saving solutions, modular irradiation systems have become highly attractive due to their speed, reliability, and ability to preserve equipment integrity. This shift toward cost-effective and distributed healthcare models is expected to sustain robust growth for irradiation technologies across both urban and rural settings.

Key industry participants shaping the competitive landscape of the Irradiation Apparatus Market include GE HealthCare, Elekta, Siemens Healthineers, Mindray, Canon Medical Systems, NPB Ion Beam Technology, Neusoft Medical Systems, Accuray, ViewRay, Hitachi, Sumitomo Heavy Industries, Shinva Medical, Koninklijke Philips, Mevion Medical Systems, and Panacea Medical Technologies. These companies continue to set benchmarks through product innovation and strategic expansion.

Leading players in the irradiation apparatus space are focusing on product portfolio expansion through advanced imaging-guided and AI-integrated radiation systems. Many companies are heavily investing in R&D to boost treatment accuracy, automate workflows, and enhance safety. Collaborations with cancer treatment centers and healthcare institutions are helping tailor solutions that match evolving clinical needs. To address global demand, especially in underserved regions, firms are developing modular and cost-effective systems that reduce installation complexity.