섬유 금속 적층재 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)

Fiber-Metal Laminates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1773446

리서치사:Global Market Insights Inc.

발행일:2025년 06월

페이지 정보:영문 235 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

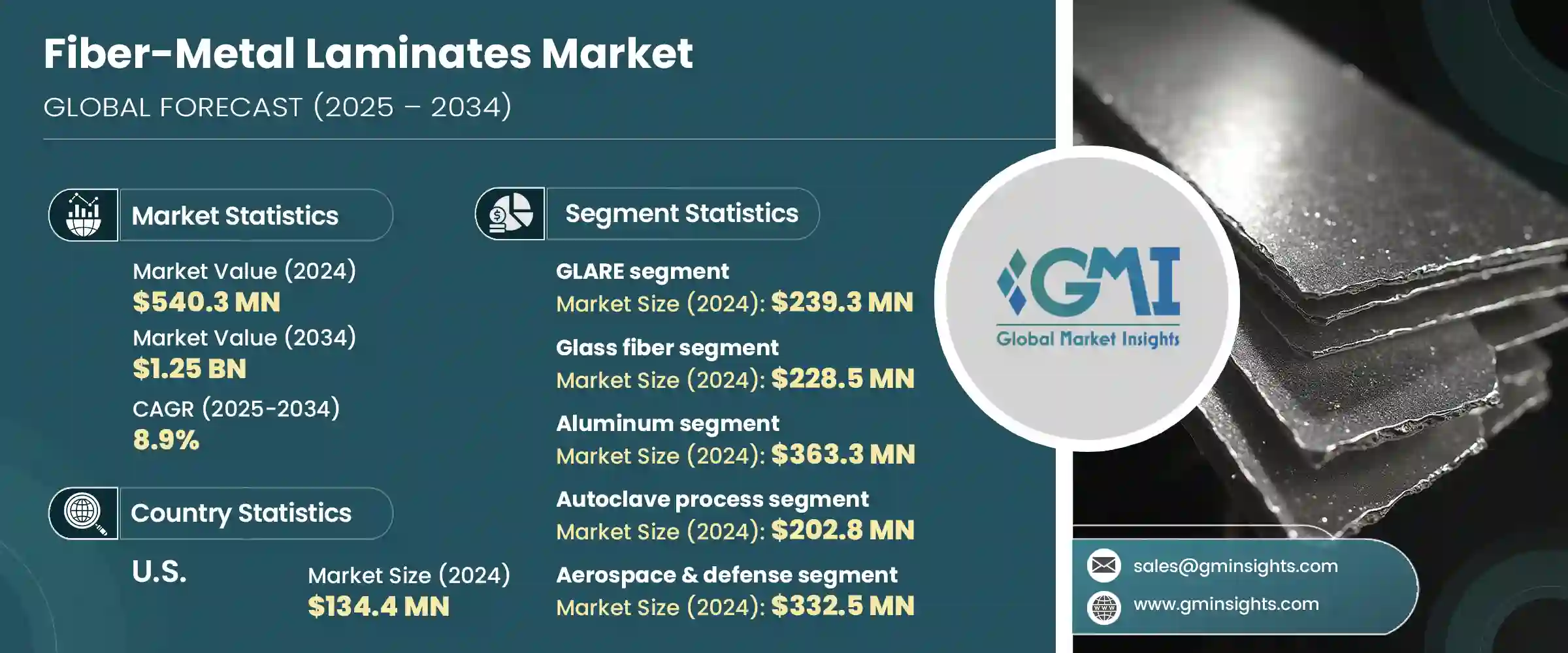

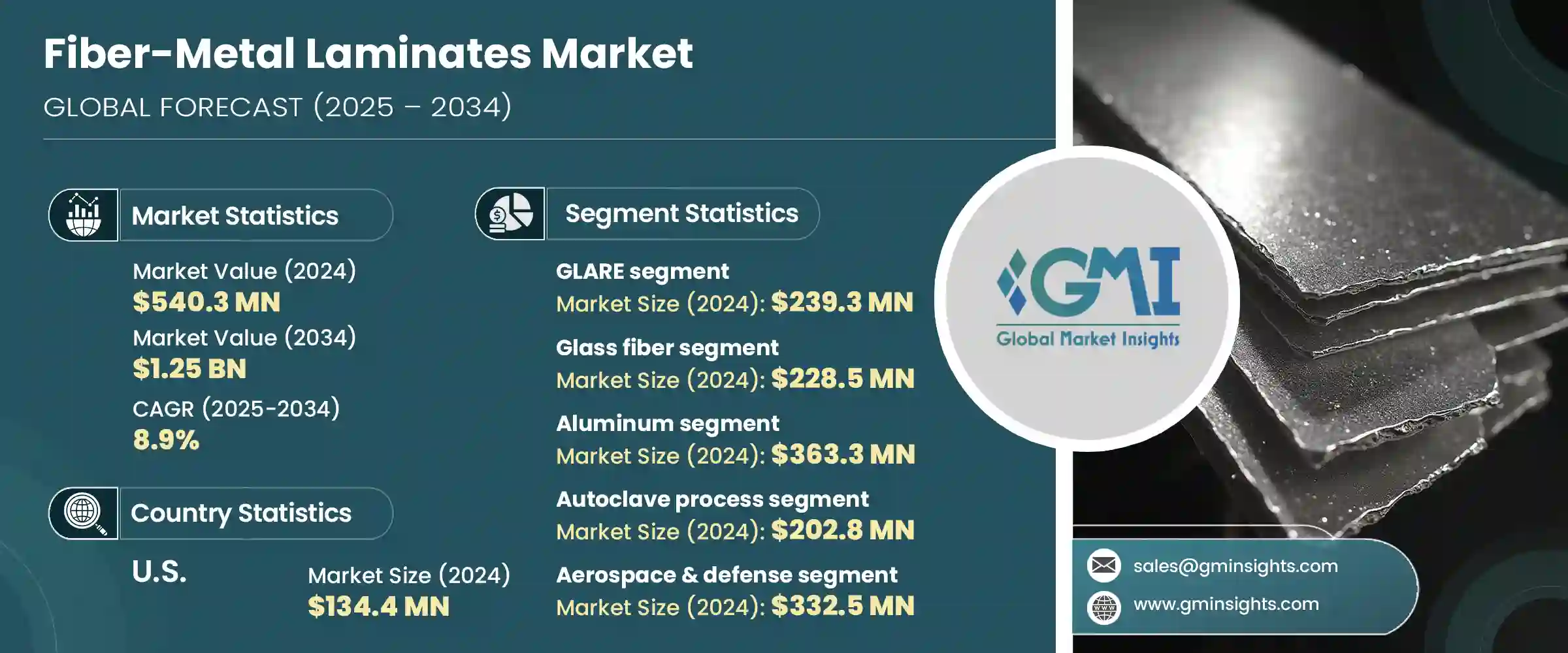

섬유 금속 적층재 세계 시장은 2024년에는 5억 4,030만 달러로 평가되었고, CAGR 8.9%로 성장하여 2034년에는 12억 5,000만 달러에 이를 것으로 예측됩니다.

특히 항공우주 분야에서 경량화 재료에 대한 요구가 높아지면서 이 시장의 확대에 박차를 가하고 있습니다. 항공기 경량화, 연료 효율 향상, 적재량 증가를 위해 FML을 채택하는 제조업체가 증가하고 있습니다. 동체 패널, 날개 및 기타 고응력 부품과 같은 항공기 구조에 FML을 통합하는 것은 뛰어난 피로 저항성과 최소한의 유지보수 요구 사항으로 인해 지속적으로 증가하고 있습니다. 기존 금속과 달리 FML은 내구성과 피로 저항성이 향상되어 수리 횟수가 줄어들고 수명이 길어집니다. 전 세계적으로 지속가능성에 대한 노력이 강화되고 환경 규제가 강화됨에 따라 저연비 재료의 역할이 더욱 중요해짐에 따라 주요 분야에서 섬유 금속 적층 재료의 채택을 더욱 촉진하고 있습니다.

최근 제조 기술의 발전은 FML 제조의 정밀도와 확장성을 크게 향상시켰습니다. 오토클레이브, 진공포장기, 디지털 금형 등의 기술 혁신으로 품질을 유지하면서 대규모 생산이 가능해졌습니다. 이러한 공정의 발전과 함께 FML의 용도는 자동차, 해양, 풍력에너지 분야로 확대되고 있습니다. 이러한 변화는 복합재료와 금속을 결합하여 엄격한 중량, 강도 및 적응성 기준을 충족하는 하이브리드 재료 통합 증가 추세에 힘입은 바 큽니다. 이러한 하이브리드화로 인해 FML은 다양한 산업, 특히 중량 대비 성능이 최우선적으로 고려되는 모빌리티 및 인프라 분야에서 구조 설계에 선호되는 재료로 각광받고 있습니다.

시장 범위

개시 연도

2024년

예측 연도

2025-2034년

개시 금액

5억 4,030만 달러

예측 금액

12억 5,000만 달러

CAGR

8.9%

GLARE 부문은 2024년에 2억 3,930만 달러에 달했으며, 2025년부터 2034년까지 연평균 8.3%의 성장률을 보일 것으로 예측됩니다. 유리섬유와 알루미늄을 사용한 이 섬유금속 라미네이트는 피로와 부식에 강하고 전체 무게가 가벼워 항공우주 분야에서 널리 사용되고 있습니다. GLARE와 함께 ARALL 및 CARALL과 같은 다른 변형은 더 높은 내충격성과 강성을 필요로 하는 응용 분야에서 인기를 얻고 있습니다. 이러한 대안은 특히 경량화와 구조적 무결성을 동시에 충족해야 하는 경우, 보다 광범위한 엔지니어링 솔루션에 기여합니다.

유리섬유 기반 라미네이트 부문은 2024년 2억 2,850만 달러에 달했으며, 예측 기간 동안 8.3%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 유리 섬유는 비용 효율성, 강도 및 내식성이 뛰어나기 때문에 여전히 이 시장의 핵심 소재입니다. 자동차 및 항공우주와 같은 산업에서 유리섬유 라미네이트는 균형 잡힌 성능과 저렴한 가격으로 인해 선호되고 있습니다. 주요 기업들이 구축한 신뢰할 수 있는 공급망을 유지함으로써 원자재에 대한 안정적인 접근이 보장되어 이 부문의 성장과 안정성을 뒷받침하고 있습니다.

미국의 섬유 금속 적층재 2024년 시장 규모는 1억 3,440만 달러로 평가되었고, 2034년까지 연평균 8.6%를 보일 것으로 예측됩니다. 방위 및 항공우주 산업의 빠른 발전 속도가 이 지역 성장의 주요 원동력이 되고 있습니다. 주요 항공기 제조업체를 포함한 생태계와 국방 및 R&D에 대한 정부의 적극적인 투자로 미국은 FML 혁신과 배치의 최전선에 서 있습니다. 또한, 전기자동차 생산에 대한 관심이 높아지고 제조 방식이 강화됨에 따라, 특히 경량화가 주요 설계 목표가 되면서 FML에 대한 새로운 수요를 창출하고 있습니다.

세계 섬유 금속 적층재 업계에서 경쟁하는 유명 기업으로는 에어버스 SE, 록히드마틴, 도레이, 보잉, 헥셀 등이 있습니다. 이들 기업은 고도로 기술적이고 경쟁이 치열한 분야에서 우위를 점하기 위해 차세대 FML 솔루션에 적극적으로 투자하고 있습니다. 섬유 금속 라미네이트 분야에서 경쟁하는 기업들은 세계 입지를 확대하기 위해 지속적인 혁신, 전략적 제휴, 생산 확장성에 중점을 두고 있습니다. 주요 업체들은 신흥 응용 분야를 위해 내피로성, 내식성, 열 특성을 개선한 FML을 개발하기 위해 연구개발에 많은 투자를 하고 있습니다. 많은 기업들이 항공우주 및 자동차 OEM과 파트너십을 맺고 고성능 응용 분야에 맞는 소재를 공동 개발하고 있습니다. 또 다른 일반적인 접근 방식은 생산 공정의 자동화와 스마트 제조의 통합을 통해 사이클 타임과 비용을 절감하는 것입니다.

목차

제1장 조사 방법

시장 범위와 정의

조사 디자인

조사 접근

데이터 수집 방법

데이터 마이닝 소스

세계

지역/국

기본 추정과 계산

기준연도 계산

시장 예측 주요 동향

1차 조사와 검증

1차 정보

예측 모델

조사 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 미치는 요인

파괴적 변화

업계에 대한 영향요인

성장 촉진요인

업계의 잠재적 리스크&과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

제품별

향후 시장 동향

기술 및 혁신 상황

현재 기술 동향

신기술

특허 상황

무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

주요 수입국

주요 수출국

지속가능성과 환경 측면

지속가능한 관행

폐기물 감축 전략

생산 에너지 효율

친환경 대처

탄소발자국 고려

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

인수합병(M&A)

파트너십 및 협업

신제품 발매

확장 계획

제5장 시장 추산·예측 : 유형별, 2021년-2034년

주요 동향

GLARE(유리 라미네이트 알루미늄 강화 에폭시)

그레아 1

그레아 2

그레아 3

그레아 4

그레아 5

그레아 6

ARALL(아라미드 강화 알루미늄 라미네이트)

ARALL 1

ARALL 2

ARALL 3

ARALL 4

CARALL(카본 강화 알루미늄 라미네이트)

TICARALL(티타늄 카본 강화 알루미늄 라미네이트)

기타 FML 유형

제6장 시장 추산·예측 : 섬유 유형별, 2021년-2034년

주요 동향

유리섬유

E유리

S유리

기타 유리 유형

탄소섬유

고강도 탄소섬유

고탄성 탄소섬유

초고탄성 탄소섬유

아라미드 섬유

케브라

노멕스

기타 아라미드타입

천연섬유

하이브리드 섬유

제7장 시장 추산·예측 : 금속 유형별, 2021년-2034년

주요 동향

알루미늄

2024 알루미늄 합금

7075 알루미늄 합금

기타 알루미늄 합금

티타늄

Ti-6Al-4V

기타 티타늄 합금

강철

스테인리스 스틸

탄소강

마그네슘

기타 금속

제8장 시장 추산·예측 : 제조 공정별, 2021년-2034년

주요 동향

오토클레이브 처리

프레스 경화

진공 백 성형

필라멘트 와인딩

Pultrusion

기타 제조 공정

제9장 시장 추산·예측 : 용도별, 2021년-2034년

주요 동향

항공우주

기체

날개

뒷날개

조종익면

기타 항공우주 용도

자동차

보디 패널

구조 부품

크래쉬 박스

기타 자동차 용도

해양

선체 구조

데크 구조

기타 해양 용도

풍력에너지

터빈 블레이드

나셀 부품

기타 풍력에너지 용도

스포츠 및 레크리에이션

기타

제10장 시장 추산·예측 : 최종 이용 산업별, 2021년-2034년

주요 동향

항공우주 및 방위

상용 항공

군용 항공

우주 용도

방위 용도

자동차

승용차

상용차

전기자동차

해양

상용 선박

해군 함정

레크리에이션 보트

에너지

풍력에너지

기타 에너지 용도

기타

제11장 시장 추산·예측 : 지역별, 2021년-2034년

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카공화국

아랍에미리트(UAE)

기타 중동 및 아프리카

제12장 기업 개요

Premium AEROTEC GmbH(Airbus Group)

Fokker Technologies

Cytec Solvay Group

Alcoa Corporation

3A Composites

Comtek Advanced Structures Ltd.

Bombardier Inc.

Embraer S.A.

Boeing Company

Airbus SE

Lockheed Martin Corporation

Northrop Grumman Corporation

Saab AB

Leonardo S.p.A.

Mitsubishi Heavy Industries Ltd.

Kawasaki Heavy Industries Ltd.

Toray Industries, Inc.

Hexcel Corporation

Teijin Limited

SGL Carbon SE

LSH

영문 목차

영문목차

The Global Fiber-Metal Laminates Market was valued at USD 540.3 million in 2024 and is estimated to grow at a CAGR of 8.9% to reach USD 1.25 billion by 2034. The rising need for lightweight materials, especially in aerospace, is a key factor fueling this market's expansion. Manufacturers are increasingly turning to FMLs to cut down aircraft weight, enhance fuel efficiency, and increase payload capacity. Their integration in aircraft structures like fuselage panels, wings, and other high-stress components continues to rise due to exceptional fatigue resistance and minimal maintenance requirements. Unlike conventional metals, FMLs offer improved durability and fatigue tolerance, leading to fewer repairs and longer service life. As global sustainability efforts intensify, along with stricter environmental regulations, the role of fuel-efficient materials becomes even more vital, further boosting the adoption of fiber-metal laminates across major sectors.

Recent advancements in manufacturing technology have significantly improved the precision and scalability of FML production. Innovations in autoclaving, vacuum bagging, and digital tooling now enable large-scale manufacturing while maintaining quality. As these processes evolve, applications for FMLs are expanding into the automotive, marine, and wind energy sectors. This shift is supported by the growing trend of hybrid material integration, where composites and metals are combined to meet stringent weight, strength, and adaptability criteria. Such hybridization is pushing FMLs into the spotlight as a preferred material in structural design across diverse industries, especially in mobility and infrastructure, where the performance-to-weight ratio is a primary consideration.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$540.3 million

Forecast Value

$1.25 billion

CAGR

8.9%

The GLARE segment generated USD 239.3 million in 2024 and is expected to grow at a CAGR of 8.3% from 2025 to 2034. This fiber-metal laminate, made using glass fibers and aluminum, is widely used in aerospace due to its resistance to fatigue and corrosion, along with its low overall weight. Its reliability in both defense and commercial aviation continues to sustain demand. Alongside GLARE, other variants like ARALL and CARALL are gaining traction for applications that require higher impact resistance and stiffness. These alternatives contribute to a broader range of engineering solutions, especially where weight reduction and structural integrity must go hand in hand.

The glass fiber-based laminates segment accounted for USD 228.5 million in 2024 and is projected to grow at a CAGR of 8.3% during the forecast period. Glass fiber remains a cornerstone material in this market because of its cost-effectiveness, strength, and corrosion resistance. Industries such as automotive and aerospace prefer glass fiber laminates for their balanced performance and affordability. The established and dependable supply chains maintained by major corporations help ensure consistent access to raw materials, supporting growth and stability within the segment.

United States Fiber-Metal Laminates Market generated USD 134.4 million in 2024 and is anticipated to grow at a CAGR of 8.6% through 2034. The rapid pace of development in the defense and aerospace industries is a major driver for regional growth. With an ecosystem that includes leading aircraft producers and robust government investment in defense and R&D, the U.S. remains at the forefront of FML innovation and deployment. Additionally, increased focus on electric vehicle production and enhancements in manufacturing practices are creating new demand streams for FMLs, particularly as lightweight becomes a primary design objective.

Some of the prominent names competing in the Global Fiber-Metal Laminates Industry include Airbus SE, Lockheed Martin Corporation, Toray Industries, Inc., Boeing Company, and Hexcel Corporation. These companies are actively investing in next-generation FML solutions to stay ahead in a highly technical and competitive field. Companies competing in the fiber-metal laminates space are emphasizing continuous innovation, strategic collaborations, and production scalability to expand their global presence. Key players are investing heavily in R&D to develop FMLs with enhanced fatigue resistance, corrosion protection, and improved thermal properties for emerging applications. Many firms are forming partnerships with aerospace and automotive OEMs to co-engineer materials tailored for high-performance use. Another common approach includes automating production processes and integrating smart manufacturing to reduce cycle time and costs.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Type

2.2.3 Fiber type

2.2.4 Metal type

2.2.5 Manufacturing process

2.2.6 Application

2.2.7 End use industry

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.2 Industry pitfalls and challenges

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.6.1 Technology and Innovation landscape

3.6.2 Current technological trends

3.6.3 Emerging technologies

3.7 Price trends

3.7.1 By region

3.7.2 By product

3.8 Future market trends

3.9 Technology and Innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent landscape

3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)