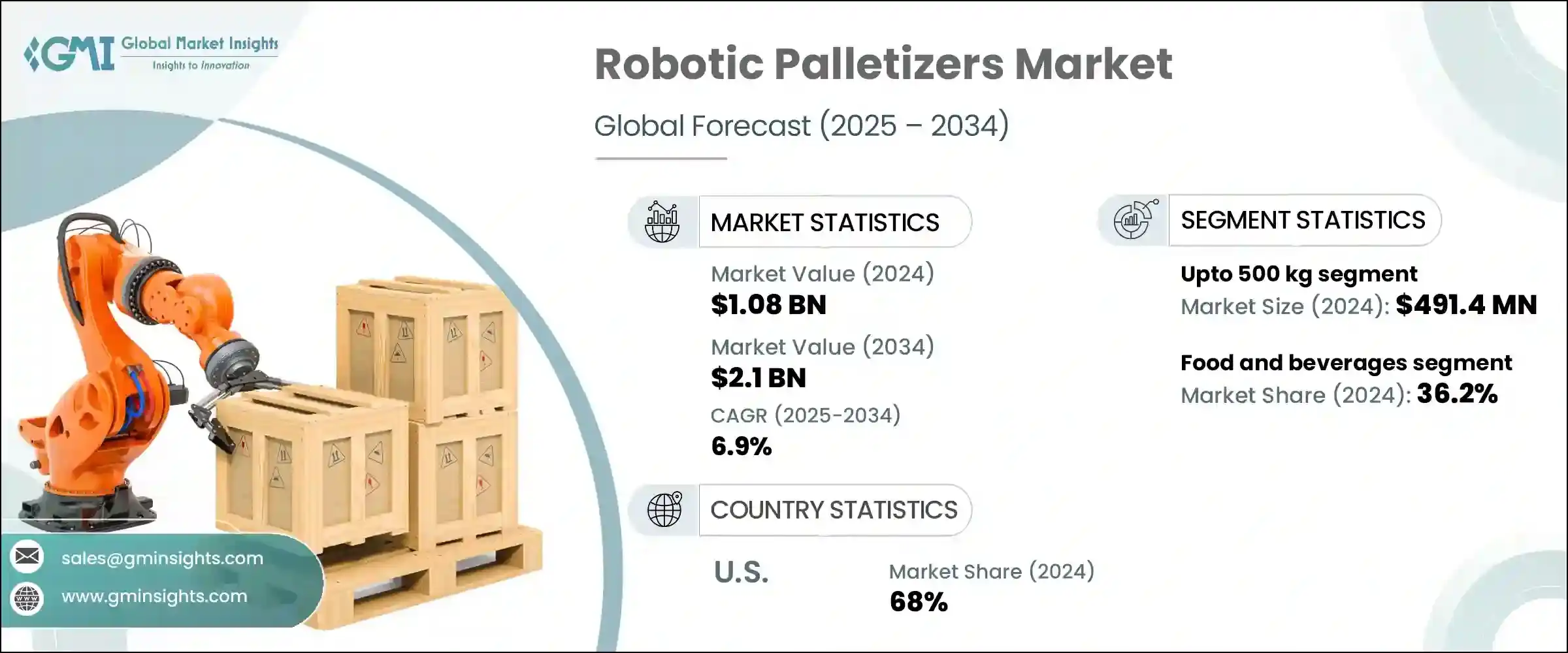

로봇 팔레타이저 세계 시장 규모는 2024년에 10억 8,000만 달러로 평가되었고, CAGR 6.9%로 성장하여 2034년에는 21억 달러에 이를 것으로 예측됩니다.

다양한 분야에서 자동화 수요가 급증하는 것이 이 시장을 이끄는 주요 요인입니다. 로봇 팔레타이저는 팔레 타이 징 및 디 팔레 타이 징 작업을 자동화하도록 설계되어 사이클 시간 단축, 처리량 증가, 설치 공간의 소형화 및 비용 효율성 향상을 가능하게 합니다. 노동력 부족, 임금 상승, 보다 안전하고 효율적인 자재관리를 촉진하는 것이 성장의 주요 요인입니다. 이러한 로봇 시스템은 팔레트에 상품을 쌓는 노동 집약적인 프로세스를 자동화함으로써 수작업에 대한 의존도를 줄이고, 실수를 제한하며, 사고 위험을 최소화하여 작업장 안전을 향상시킵니다.

세계 물류의 복잡성과 전자상거래의 확대는 성장을 더욱 촉진하고 있습니다. 두 가지 모두 신속한 주문 처리를 위해 창고와 물류센터에서 다양한 제품을 고도로 효율적으로 처리할 수 있어야 합니다. 첨단 로봇 팔과 협동 로봇의 도입은 로봇 팔레타이저를 더욱 다재다능하게 만들어 중소기업에 보다 친숙하게 다가갈 수 있도록 했습니다. 이러한 장점에도 불구하고, 높은 초기 비용, 기존 시스템과의 통합의 복잡성, 지속적인 유지보수 및 프로그래밍 비용, 숙련된 인력의 필요성 등의 문제에 직면하고 있습니다. 그럼에도 불구하고, 기술 혁신과 경제적 이점이 로봇 팔레타이저를 자동화된 제조 및 공급망 환경에 도입하는 것을 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 개시 금액 | 10억 8,000만 달러 |

| 예측 금액 | 21억 달러 |

| CAGR | 6.9% |

최대 500kg의 제품을 취급하는 부문은 2024년 4억 9,140만 달러의 매출을 기록했습니다. 이 카테고리의 로봇은 중저중량 패키지를 위해 설계되었으며, 특히 전자상거래 및 소비자 제품 취급의 자동화 증가로 인해 빠르게 성장하고 있습니다. 이 로봇 팔레타이저는 제약, 식음료, 소비재 및 기타 제조 산업에서 선호되고 있습니다. 다양한 크기의 박스, 가방, 케이스 등을 관리할 수 있어 다양한 팔레타이징 용도에 다용도로 사용되며 수요가 높습니다.

2024년 시장 점유율은 식음료가 36.2%로 가장 큰 비중을 차지했습니다. 로봇 팔레타이저는 효율성, 위생, 일관성이 중요한 이 산업에서 필수불가결한 존재가 되고 있습니다. 대량 생산과 빠른 유통에 대한 수요와 더불어 팔레타이징과 같은 반복적인 작업의 지속적인 노동력 부족과 비용 상승으로 인해 기업들은 프로세스 자동화를 추진하고 있습니다. 로봇 시스템은 작업 효율을 향상시킬 뿐만 아니라 사람이 식품에 접촉할 기회를 줄여 오염 위험을 최소화합니다. 또한, 엄격한 위생 기준을 충족하는 식품용 로봇도 개발되어 이 분야에서의 채택을 더욱 촉진하고 있습니다.

2024년 미국 로봇 팔레타이저 시장 점유율은 68%를 보였섭니다. 이러한 성장을 이끄는 요인으로는 공급망의 복잡성 증가와 인건비 상승이 있으며, 로봇 팔레타이저는 운영의 연속성을 유지하기 위한 실용적인 투자가 되고 있습니다. 미국은 또한 제조 기술의 발전과 인더스트리 4.0 이니셔티브의 혜택을 누리고 있으며, 이는 로봇 팔레타이징 솔루션에 대한 수요를 증가시키고 있습니다. 로봇 도입의 선두주자인 이 나라는 여러 제조 공정에서 로봇 밀도를 높이고 있으며, 이는 시장의 모멘텀을 높이고 있습니다.

세계 로봇 팔레타이저 산업에서 경쟁하는 주요 기업으로는 Fanuc Corporation,KUKA AG,ABB,ABB,Honeywell International Inc,Schneider Packaging Equipment Company,Bastian Solutions,Fuji Robotics, Okura LLC, Pasco Systems, Premier Tech, Robotiq, Kawasaki Heavy Industries, KION Group AG, Sidel, Yaskawa Electric Corporation 등이 있습니다. 로봇 팔레타이저 분야의 기업들은 시장에서의 입지를 강화하기 위해 다양한 크기와 무게의 제품을 정확하게 취급할 수 있는 적응력이 뛰어난 로봇 시스템을 개발하고 혁신에 집중하고 있습니다. 자동화 효율성, 통합 용이성, 사용자 친화적 인 인터페이스를 개선하기 위해 연구 개발에 투자하고 있습니다. 포장 및 물류 솔루션 제공업체와의 전략적 제휴를 통해 기존 공급망에 원활하게 통합되는 엔드 투 엔드 자동화 솔루션을 제공할 수 있습니다. 또한 현지 생산, 고객 서비스 네트워크 강화, 고객과의 견고한 관계를 보장하기 위한 애프터서비스 지원을 통해 세계 입지를 확장하고 있습니다.

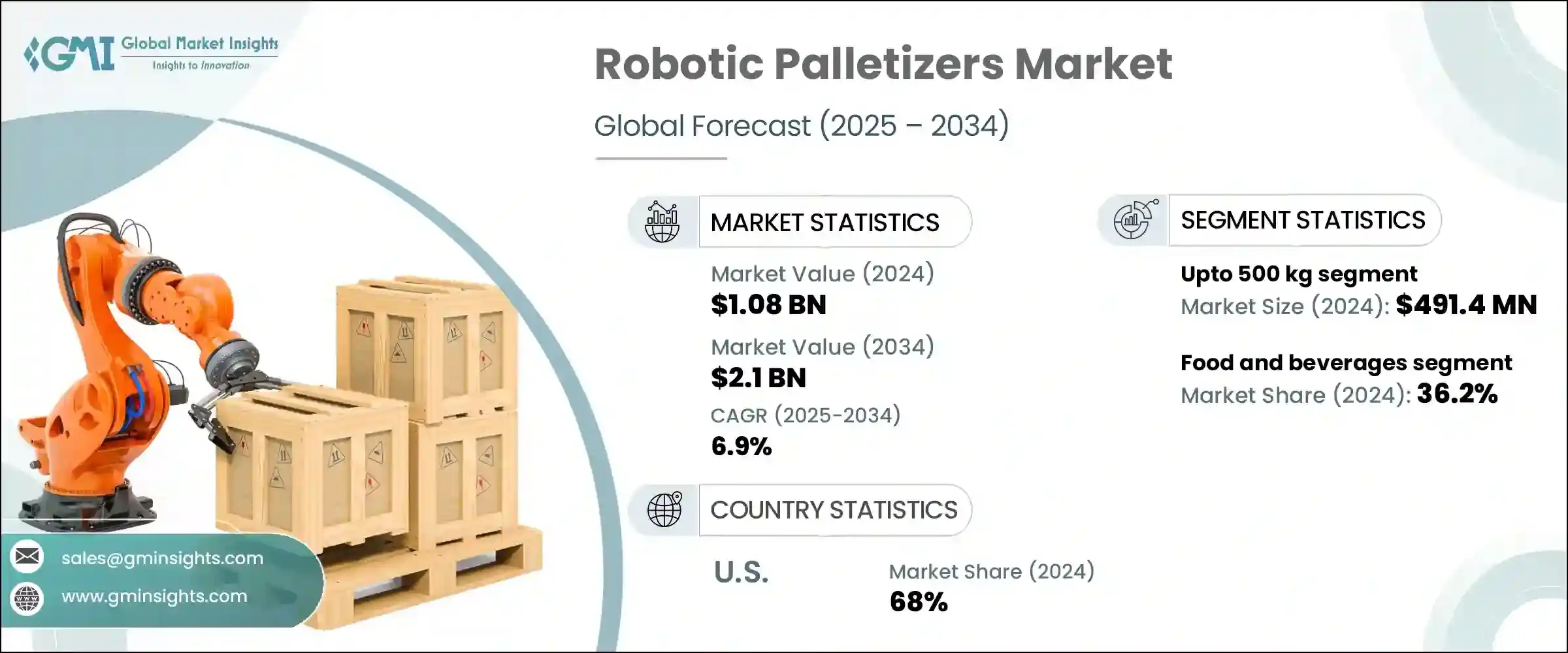

The Global Robotic Palletizers Market was valued at USD 1.08 billion in 2024 and is estimated to grow at a CAGR of 6.9% to reach USD 2.1 billion by 2034. The surge in automation demand across various sectors is a major factor propelling this market. Robotic palletizers are engineered to automate palletizing and depalletizing tasks, enabling faster cycle times, increased throughput, compact footprints, and cost-efficiency. Rising labor shortages, escalating wages, and the drive for safer, more efficient material handling are primary growth drivers. By automating the labor-intensive process of stacking goods onto pallets, these robotic systems reduce the dependency on manual labor, limit errors, and enhance workplace safety by minimizing accident risks.

Growth is further supported by the complexity of global logistics and the expansion of e-commerce, both of which require highly efficient handling of diverse products in warehouses and distribution centers for rapid order processing. Innovations such as advanced robotic arms and the introduction of collaborative robots have made robotic palletizers more versatile and accessible to small and medium-sized businesses alike. Despite their advantages, the market faces challenges due to high upfront costs, integration complexities with existing systems, ongoing maintenance and programming expenses, and the need for skilled personnel. Nevertheless, ongoing technological innovations and economic benefits are driving the adoption of robotic palletizers within automated manufacturing and supply chain environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.08 billion |

| Forecast Value | $2.1 billion |

| CAGR | 6.9% |

The handling products up to 500 kg segment generated USD 491.4 million in 2024. Robots in this category are designed for light to medium-weight packages and are experiencing rapid growth, particularly due to increasing automation in e-commerce and consumer product handling. These robotic palletizers are favored across industries such as pharmaceuticals, food and beverages, consumer goods, and other manufacturing sectors. Their ability to manage varying box sizes, bags, and cases makes them versatile and highly demanded for diverse palletizing applications.

The food & beverages segment held the largest market share in 2024, accounting for 36.2%. Robotic palletizers have become indispensable in this industry where efficiency, hygiene, and consistency are critical. High-volume production and swift distribution demands, combined with persistent labor shortages and rising costs for repetitive tasks like palletizing, push companies to automate processes. Robotic systems not only improve operational efficiency but also reduce human contact with food products, minimizing contamination risks. Additionally, specialized food-grade robots are developed to comply with strict hygiene standards, further driving adoption in this sector.

United States Robotic Palletizers Market held a 68% share in 2024. Factors fueling this growth include increasing supply chain complexity and high labor costs, which make robotic palletizers a practical investment to maintain operational continuity. The U.S. also benefits from advancements in manufacturing technology and Industry 4.0 initiatives, boosting the demand for robotic palletizing solutions. As one of the leaders in robotics adoption, the country exhibits growing robot density across multiple manufacturing processes, enhancing market momentum.

Leading companies competing in the Global Robotic Palletizers Industry include FANUC Corporation, KUKA AG, ABB, Honeywell International Inc, Schneider Packaging Equipment Company, Bastian Solutions, Fuji Robotics, Okura LLC, Pasco Systems, Premier Tech, Robotiq, Kawasaki Heavy Industries Ltd, KION Group AG, Sidel, and Yaskawa Electric Corporation. To strengthen their market presence, companies in the robotic palletizers sector focus on innovation by developing highly adaptable robotic systems capable of handling a wide range of product sizes and weights with precision. They invest in research and development to improve automation efficiency, ease of integration, and user-friendly interfaces. Strategic collaborations with packaging and logistics solution providers allow them to deliver end-to-end automation solutions that fit seamlessly into existing supply chains. Firms also expand their global footprint through localized production, enhanced customer service networks, and tailored after-sales support, ensuring robust client relationships.