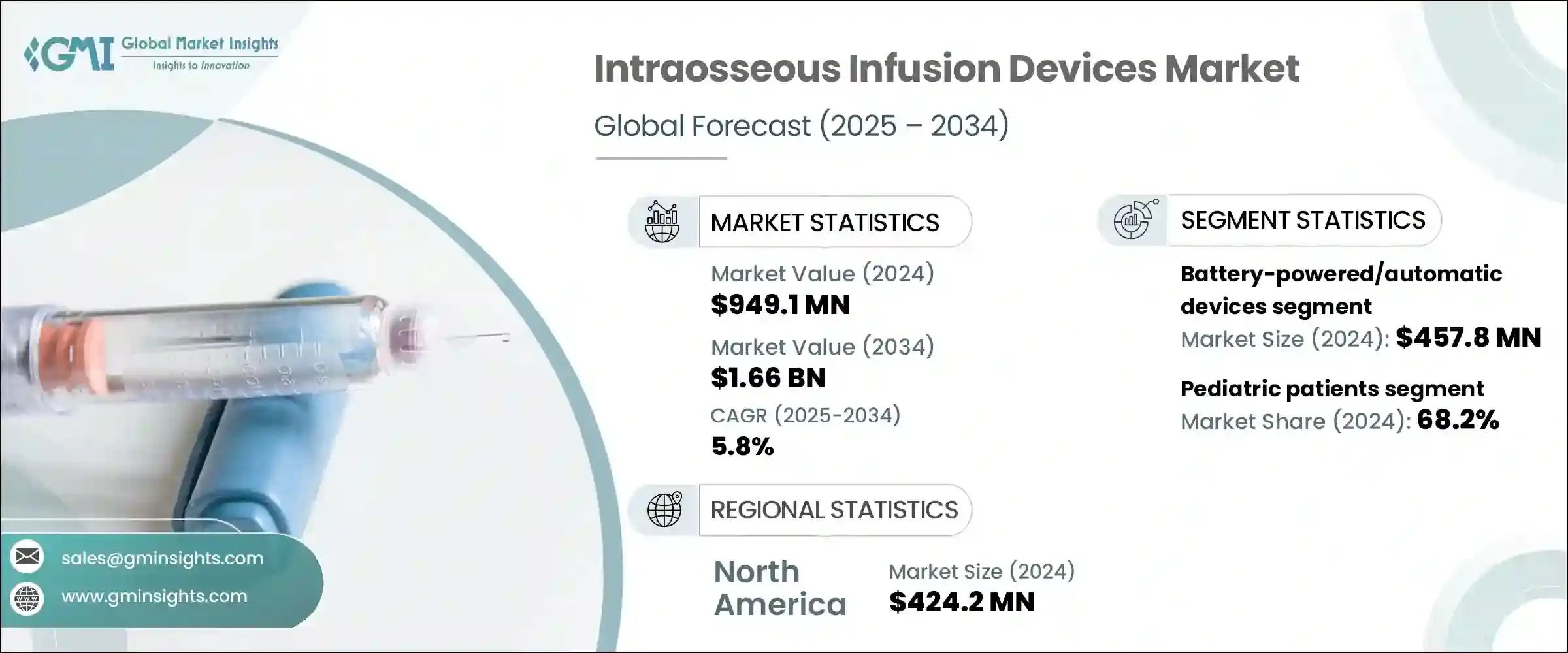

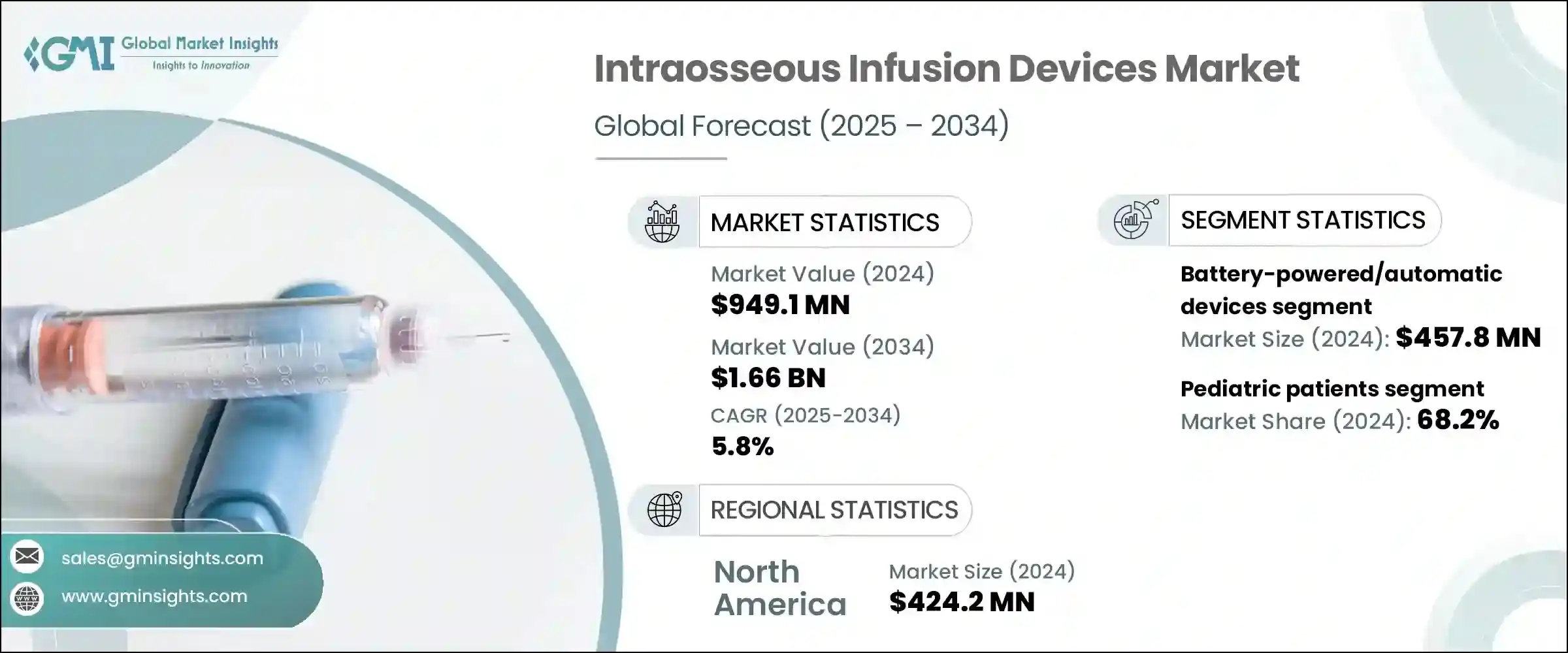

세계의 골내 주입 기기 시장은 2024년에는 9억 4,910만 달러로 평가되었고, CAGR 5.8%로 성장하여 2034년에는 16억 6,000만 달러에 이를 것으로 예측됩니다.

골내 주입 기기는 특히 기존의 정맥 접근이 지연되거나 효과가 없는 것으로 밝혀진 경우, 골수에 직접 주입하여 투약함으로 혈액 제제를 신속하게 투여하도록 설계되어 있습니다.

골내 주입 기기는 신속한 반응과 신뢰성으로 인해 다양한 의료 환경에서 응급 의료 프로토콜에 사용됩니다. 골내 주입 기기는 신속한 개입이 요구되는 긴급 상황에서 널리 사용됩니다. 골내 접근법의 사용 확대도 민간 및 군의 의료 서비스 전반에 걸쳐 훈련 프로그램이나 프로토콜의 통합이 점점 중시되면서 지지되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024 |

| 예측연도 | 2025-2034 |

| 시작금액 | 9억 4,910만 달러 |

| 예측금액 | 16억 6,000만 달러 |

| CAGR | 5.8% |

시장은 제품 유형별로 배터리식, 수동식 IO침, 자동식 기기, 충격 구동식 시스템으로 구분됩니다. 배터리식 및 자동식 기기는 배치 속도와 용이성으로 인해 응급 의료에서 의존하는 솔루션이 되었으며 종종 동등한 수동식 제품보다 효율적이라는 것이 입증되었습니다. 자동식 기기는 긴급 상황에서 기존의 정맥 내 접근법을 선택할 수 없는 경우 신뢰할 수 있는 대안을 제공합니다. 또한 가혹한 상황 하에서의 성능은 세계의 헬스케어 시스템에서의 채용으로 이어지고 있으며, 긴급 대응 능력과 전투 관리 시스템을 강화하기 위한 정부로부터의 투자에 의해 더욱 강화되고 있습니다.

연령대별로 시장은 성인 환자와 소아 환자로 분류됩니다. 소아 환자는 정맥이 작고 취약하기 때문에 정맥을 통한 접근이 어려울 수 있습니다. 그 결과, 집중치료실, 외래 서비스, 응급실 등에서 소아 전용 복강내 기기에 대한 수요가 높아지고 있습니다.

최종 용도의 관점에서 시장은 병원, 클리닉, 외래수술센터(ASC), 기타 환경으로 구분됩니다. 외상, 심정지, 패혈증 및 혈액량 감소 충격과 같은 심각한 병태 증가로 입원 환자와 응급 환자 환경에서 신속하고 신뢰할 수 있는 정맥 접근 솔루션의 필요성이 높아지고 있습니다. 정맥내 주입은 특히 중증 환자나 정맥의 위치를 알기 어려운 환자 등 정맥 접근이 지연되거나 불가능한 경우에 중요한 선택사항이 되고 있습니다.

2024년 세계 시장은 북미가 주도했으며 총 평가액은 4억 2,420만 달러였습니다. 북미 시장의 높은 수요는 특히 정맥내 투여가 불가능한 환자에 대해 즉각적인 혈관 접근을 필요로 하는 폭넓은 긴급 사고에 대응할 필요성으로 인해 발생하고 있습니다.

세계의 경쟁구도는 기존 기업과 신흥 기업이 혼재하고 있습니다. Pyng Medical, Teleflex, Dickinson and Company, PerSys Medical, Becton, Cardinal Health사와 같은 주요 기업은 2024년 세계 수익의 약 70%를 차지하였습니다. 몇몇 지역 및 현지 기업은 비용효율적인 대체 제품을 제공함으로써 시장에 침투하고 있습니다.

The Global Intraosseous Infusion Devices Market was valued at USD 949.1 million in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 1.66 billion by 2034.Intraosseous infusion devices are designed for rapid administration of fluids, medications, and blood products directly into the bone marrow, particularly when conventional intravenous access proves to be delayed or ineffective. These devices are essential in critical medical emergencies, offering dependable vascular access when time is limited or peripheral veins are inaccessible due to physiological constraints or patient conditions.

Their rapid action and reliability make them a cornerstone in emergency medical protocols across various healthcare environments. They are widely used in trauma cases, shock management, and dehydration emergencies where quick intervention can significantly impact patient outcomes. Healthcare professionals in emergency departments, ambulance services, and field medical units rely on these devices for efficient resuscitation and drug delivery, especially in time-sensitive scenarios. The expanding use of intraosseous access has also been supported by increasing emphasis on training programs and protocol integration across both civilian and military medical services. Their compact build, portability, and ease of use have further propelled adoption beyond traditional hospital settings, enabling wider deployment in remote and pre-hospital care.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $949.1 Million |

| Forecast Value | $1.66 Billion |

| CAGR | 5.8% |

The market is segmented by product type into battery-powered, manual IO needles, or automatic devices, and impact-driven systems. In 2024, the battery-powered/automatic devices segment captured the largest revenue share, reaching USD 457.8 million. These devices have become the go-to solution in emergency care due to their speed and ease of deployment, often proving more efficient than their manual counterparts. Automatic intraosseous systems offer a reliable alternative when conventional intravenous routes are not an option, especially under high-pressure circumstances. Their design requires minimal training while still delivering high first-attempt success rates, making them a preferred tool in emergency vehicles, air ambulances, and military operations. Their performance in extreme conditions has boosted adoption across healthcare systems worldwide, further reinforced by investments from governments to enhance emergency readiness and combat care systems.

By age group, the market is categorized into adult and pediatric patients. In 2024, pediatric patients accounted for the majority share, commanding 68.2% of the total market. Establishing vascular access in young patients, especially infants and neonates, often presents unique challenges due to small and fragile veins. Intraosseous infusion offers an effective alternative, allowing medical professionals to administer life-saving treatments quickly and reliably. As a result, the demand for pediatric-specific intraosseous devices has grown across intensive care units, ambulatory services, and emergency departments. Global standards for pediatric emergency response increasingly incorporate intraosseous access as a frontline intervention, which has encouraged healthcare facilities to invest in compatible equipment and comprehensive training programs focused on pediatric care.

In terms of end use, the market is segmented into hospitals and clinics, ambulatory surgical centers, and other settings. The hospitals and clinics segment held the leading position in 2024 and is expected to maintain strong growth over the coming years. Rising cases of trauma, cardiac arrest, and critical conditions such as sepsis and hypovolemic shock have intensified the need for swift and reliable vascular access solutions in inpatient and emergency environments. Intraosseous infusion has become a critical option in scenarios where intravenous access is either delayed or unachievable, especially in patients who are critically ill or whose veins are hard to locate. Major healthcare organizations have integrated intraosseous devices into their emergency care protocols, further accelerating their presence across hospitals and trauma centers globally.

North America led the global market in 2024, with a total valuation of USD 424.2 million. This leadership is supported by advanced healthcare infrastructure and a high volume of emergency procedures across the region. In the United States, the market grew from USD 365.5 million in 2023 to USD 382.9 million in 2024. High demand stems from the need to handle a wide range of emergency cases that require immediate vascular access, especially in patients for whom intravenous methods are not viable. These devices have become a vital component of emergency medical protocols, offering a dependable alternative across a spectrum of clinical use cases.

The global competitive landscape features a mix of well-established players and emerging companies. Key participants such as Pyng Medical, Teleflex, Dickinson and Company, PerSys Medical, Becton, and Cardinal Health collectively accounted for around 70% of global revenue in 2024. These companies are actively expanding through acquisitions, product innovations, and strategic partnerships to reinforce their market share. At the same time, several regional and local manufacturers are penetrating the market by offering cost-effective alternatives. Competitive dynamics are further intensified by a surge in mergers, new product rollouts, and regional expansion initiatives aimed at broadening customer bases and enhancing product accessibility.