상온 혼합 아스팔트 시장(2025-2034년) : 기회, 성장 촉진요인, 산업 동향 분석, 예측

Cold Mix Asphalt Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1773412

리서치사:Global Market Insights Inc.

발행일:2025년 06월

페이지 정보:영문 220 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

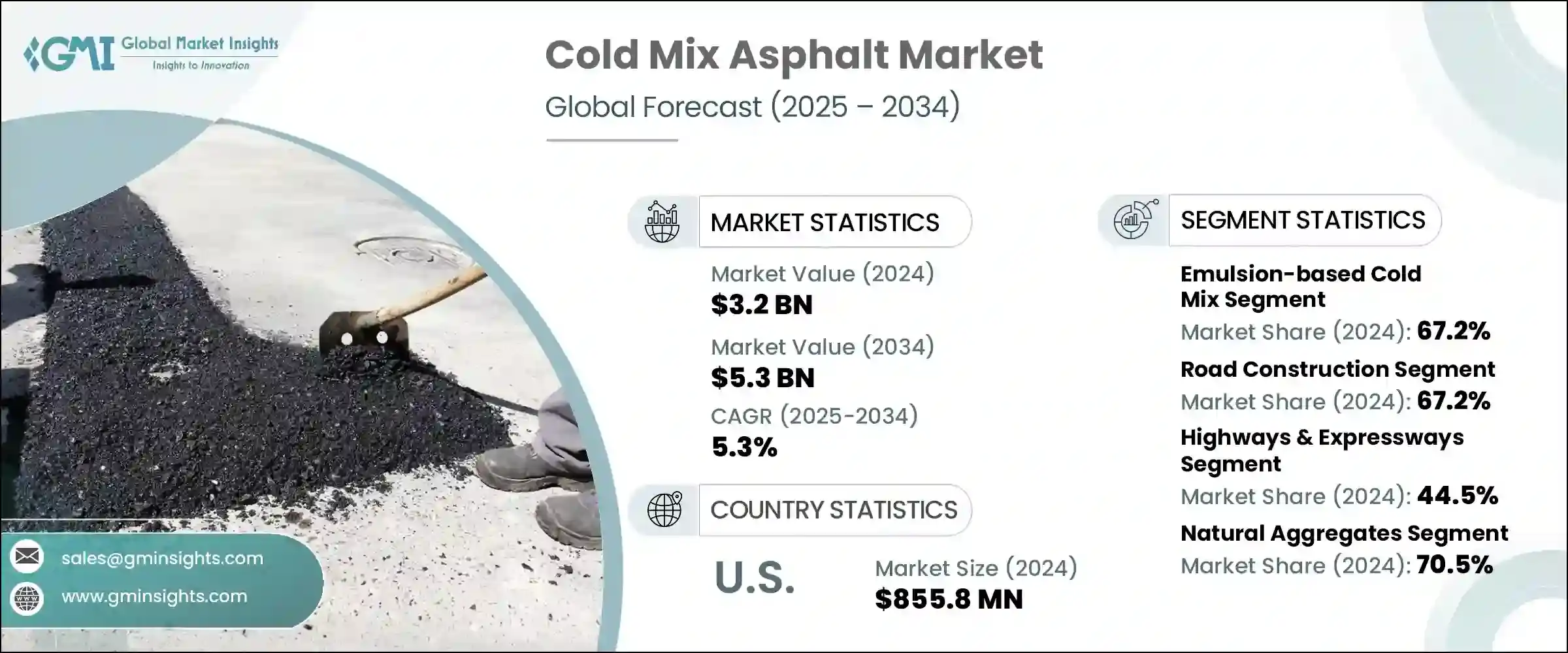

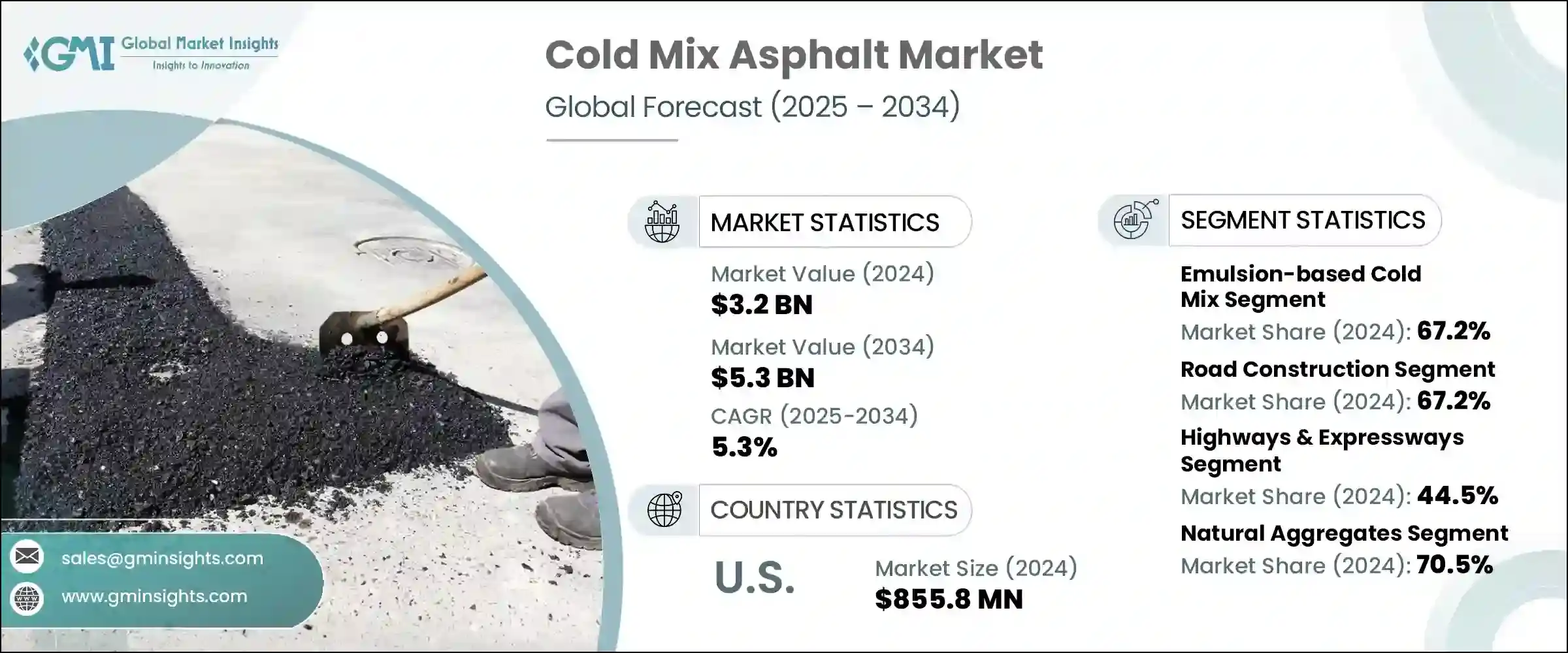

세계의 상온 혼합 아스팔트 시장 규모는 2024년에 32억 달러에 달하였고, CAGR 5.3%로 성장하여 2034년에는 53억 달러에 이를 것으로 예측됩니다.

이 성장의 원동력이 되고 있는 것은 지속적인 인프라 투자, 저배출 건설자재 수요 증가, 세계의 도로 유지 및 복구 프로젝트에 대한 주목의 고조입니다. 개발도상지역과 선진지역의 정부는 특히 가열 혼합 공장에 대한 액세스가 제한되고 있거나 존재하지 않는 지역에서 도로의 연결 및 보수 프로그램을 추진하고 있습니다.

이 아스팔트 유형은 온실가스 배출량을 줄이기 위해 지속 가능한 인프라 정비를 선호하는 규제 상황에서 매력적인 선택입니다. 도로의 복구 및 교통량이 적은 도로의 유지관리에서 상온 혼합 아스팔트의 사용은 비용에 민감하고 물류적으로 어려운 시나리오에서 필수적인 요소가 되고 있습니다. 또한 배합 기술의 진보에 의해 신뢰성, 보존성, 최신의 포장 기준 준수성이 향상되고 있으며 따라서 분산형 건설과 긴급보수에 최적의 솔루션이 되고 있습니다.

시장 범위

시작연도

2024

예측연도

2025-2034

시작금액

32억 달러

예측금액

53억 달러

CAGR

5.3%

제품 부문별로는 에멀젼계 상온 혼합 부문이 2024년 전체 시장의 67.2%를 차지하면서 시장을 독점했습니다. 에멀젼계 혼합물은 다양한 골재와의 적합성이 높고 패치워크나 일반적인 노면 유지에 적합하기 때문에 널리 사용되고 있습니다.

도로 건설 분야는 2024년에 67.2% 시장 점유율을 차지했습니다. 교외 및 농촌에서의 도로 개발 프로젝트에서는 효율적이고 비용 효율적인 솔루션이 중시되고 있으며 이는 계속해서 상온 혼합 아스팔트 수요를 끌어올리고 있습니다. 이 재료는 운송이 용이하고 현장에서의 가열이 불필요한 물류상의 이점으로 인해 연결 도로나 샛길, 교통량이 적은 도로의 건설에 최적입니다.

최종 이용 산업의 관점에서 보면 2024년 시장 점유율의 44.5%는 고속도로와 자동차전용도로가 차지했습니다. 상온 혼합 아스팔트는 특히 지속적인 수리, 갓길 보강, 노면 안정화가 필요한 지역에서 이러한 요구사항을 충족합니다.

2024년 세계의 상온 혼합 아스팔트 시장은 미국이 8억 5,580만 달러의 평가액으로 주도했습니다. 상온 혼합은 긴급 보수나 계절적인 보수, 날씨의 변동이 심한 지역에서의 장기적인 노면 보수에 적합하며 높은 범용성으로 인해 정부나 지자체의 도로 보수 작업에서 상온 혼합의 채용이 증가하고 있습니다.

경쟁구도를 형성하는 주요 기업으로는 All States Materials Group, Martin Marietta Materials, Lakeside Industries, UNIQUE Paving Materials, Cargill 등이 있습니다. 이러한 기업은 지역 전문가와 고급 연구개발 능력을 활용하여 다양한 지역의 요구에 맞는 고성능 제품을 제공합니다. 각사는 제품을 지속적으로 개선하고 있으며, 폴리머 개질 상온 패치 솔루션과 고객 중심의 지원 시스템을 중시하는 브랜드도 현대의 인프라 우선순위에 맞춰 즉시 사용할 수 있는 사계절 포장 솔루션에 대한 소비자의 기호의 고조에 따라 그 세력을 확대하고 있습니다.

목차

제1장 조사방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

인프라 개발 확대

비용 효과 및 에너지 효율

환경 지속 가능성에 중점

도포 및 보관 용이성

업계의 잠재적 위험 및 과제

품질 일관성 문제

개발도상지역에서의 낮은 인식

가열 혼합 아스팔트와의 경쟁

표준화의 과제

시장 기회

신흥시장의 인프라 성장

기술적 진보

지속 가능한 건설 동향

원격지 용도

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

제품별

장래 시장 동향

기술과 혁신의 상황

현재의 기술 동향

신흥기술

특허 상황

무역 통계(HS코드)(주 : 무역 통계는 주요 국가에서만 제공됨)

주요 수입국

주요 수출국

지속 가능성과 환경 측면

지속 가능한 관행

폐기물 감축 전략

생산에서의 에너지 효율

환경친화적인 노력

탄소발자국의 고려

제4장 경쟁구도

소개

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병과 인수

파트너십 및 협업

신제품 발매

확장 계획

제5장 시장 추계 및 예측 : 유형별(2021-2034년)

주요 동향

에멀젼계 상온 혼합

양이온 에멀젼 상온 혼합

음이온 에멀젼 상온 혼합

비이온 에멀젼 상온 혼합

컷백 아스팔트

급속경화(RC) 컷백

중속경화(MC) 컷백

저속경화(SC) 컷백

발포 아스팔트

상온 혼합 재생

상온 재생

상온 플랜트 재생

기타 유형

폴리머 개질 상온 혼합

섬유 강화 상온 혼합

첨가제 강화 상온 혼합

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

도로 건설

신규 도로 건설

도로 확대

가설도로

도로의 유지보수 및 수리

도로 구멍 보수

균열 봉합

표면처리

긴급 수리

포장의 개수

전층 재생

상온 현장 재생

노반 안정화

기타 용도

갓길 공사

유틸리티 설비 작업

자전거 도로와 인도

제7장 시장 추계 및 예측 : 최종 이용 산업별(2021-2034년)

주요 동향

고속도로

주간고속도로

주 고속도로

자동차전용도로

행정구역 도로

도시 도로

교외 도로

농촌 도로

공항

활주로

유도로

주기장

주차장

상업용 주차장

주택 주차장

공업용 주차장

기타

항만

공업지역

레크리에이션 지역

제8장 시장 추계 및 예측 : 골재 유형별(2021-2034년)

주요 동향

천연 골재

쇄석

자갈

모래

재생 골재

재생 아스팔트 포장(RAP)

재생 콘크리트 골재(RCA)

기타 재생 재료

합성 골재

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제10장 기업 프로파일

ExxonMobil Corporation

BASF

Total Energies SE

All States Materials Group.

Martin Marietta Materials

Asphalt Materials

UNIQUE Paving Materials

Arkema Group

Kao Corporation

Ingevity Corporation

Colas SA

Aggregate Industries

Cargill

HEI-Way Premium Asphalt

Simon Team

Heidelberg Materials AG

Reeves Construction Company

Tarmac(CRH Company)

Lakeside Industries

CSM

영문 목차

영문목차

The Global Cold Mix Asphalt Market was valued at USD 3.2 billion in 2024 and is estimated to grow at a CAGR of 5.3% to reach USD 5.3 billion by 2034. This growth is being driven by ongoing infrastructure investments, a rising demand for low-emission construction materials, and increasing attention toward road maintenance and rehabilitation projects worldwide. Cold mix asphalt is steadily gaining traction as an alternative to traditional hot mix due to its ease of use, minimal equipment requirements, and ability to be applied in virtually any weather condition. Governments across developing and developed regions are pushing for road connectivity and preservation programs, especially in areas where access to hot mix plants is limited or non-existent. As a result, the cold mix alternative is becoming integral to rural road development and spot repair projects.

This asphalt type also contributes to lower greenhouse gas emissions, making it an attractive option in a regulatory landscape that favors sustainable infrastructure practices. Its use in temporary repairs, utility cut reinstatements, and maintenance of low-traffic roads has made it indispensable in cost-sensitive and logistically challenged scenarios. Furthermore, national policy support and technological advancements in formulation have enhanced its reliability, shelf life, and adherence to modern paving standards. Cold mix asphalt not only reduces labor and energy costs but also enables longer storage, making it a go-to solution for decentralized construction and emergency repairs. This convenience, coupled with its performance efficiency, ensures that cold mix continues to gain preference among public works departments and private contractors alike.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$3.2 Billion

Forecast Value

$5.3 Billion

CAGR

5.3%

In terms of product segmentation, emulsion-based cold mix dominated the market in 2024, accounting for 67.2% of the total revenue share. This dominance stems from its lower energy consumption during production and safer handling during application, which aligns well with global safety and sustainability goals. Emulsion-based mixes are widely used due to their compatibility with various aggregates and suitability for patchwork and general road surface maintenance. The rising adoption of this formulation is also supported by its ability to be applied in damp conditions, further enhancing its practicality in a range of climates and environments.

The road construction segment represented the largest application area in 2024, holding a market share of 67.2%. The increasing emphasis on efficient, cost-effective solutions for road development projects, particularly in semi-urban and rural regions, continues to boost demand for cold mix asphalt. This material offers logistical advantages, such as easier transport and no need for onsite heating, making it ideal for building access roads, byways, and low-volume traffic corridors. Its capacity to be deployed quickly with minimal resources has also made it a preferred material for initial surface treatments and paving in infrastructure expansion projects.

From an end-use industry perspective, highways and expressways contributed to 44.5% of the market share in 2024. As investments in national and regional roadways intensify, there is a growing need for quick-setting and weather-resistant materials that can withstand frequent vehicle loads while minimizing traffic disruptions. Cold mix asphalt fulfills this requirement well, particularly in areas where continuous repairs, shoulder reinforcement, and surface stabilization are needed. Its rapid deployability ensures minimal downtime, which is critical for busy routes and high-traffic expressways.

The United States led the global cold mix asphalt market in 2024, with a valuation of USD 855.8 million. Federal funding focused on infrastructure modernization, along with a broader shift toward environmentally conscious materials, has played a pivotal role in supporting market growth. The adoption of cold mix in road preservation efforts across state and municipal agencies is increasing, particularly due to its versatility and suitability for emergency repairs, seasonal patching, and long-term surface treatments in areas with extreme weather fluctuations.

Key players shaping the competitive landscape include All States Materials Group, Martin Marietta Materials, Lakeside Industries, UNIQUE Paving Materials, and Cargill. These companies leverage regional expertise and advanced R&D capabilities to offer high-performance products tailored to diverse geographic needs. With a strong focus on reliability, durability, and eco-efficiency, they continue to refine their offerings to support the evolving demands of sustainable road construction. Brands that emphasize polymer-modified cold patch solutions and customer-centric support systems are also expanding their footprint, driven by increasing consumer preference for ready-to-use, all-season pavement solutions that align with modern infrastructure priorities.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Type

2.2.3 Application

2.2.4 End use industry

2.2.5 Manufacturing process

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Growing infrastructure development

3.2.1.2 Cost-effectiveness & energy efficiency

3.2.1.3 Environmental sustainability focus

3.2.1.4 Ease of application & storage

3.2.2 Industry pitfalls and challenges

3.2.2.1 Quality consistency issues

3.2.2.2 Limited awareness in developing regions

3.2.2.3 Competition from hot mix asphalt

3.2.2.4 Standardization challenges

3.2.3 Market opportunities

3.2.3.1 Emerging markets infrastructure growth

3.2.3.2 Technological advancements

3.2.3.3 Sustainable construction trends

3.2.3.4 Remote area applications

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.6.1 Technology and innovation landscape

3.6.2 Current technological trends

3.6.3 Emerging technologies

3.7 Price trends

3.7.1 By region

3.7.2 By product

3.8 Future market trends

3.9 Technology and innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent landscape

3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion) (Kilo Tons)

5.1 Key trends

5.2 Emulsion-based cold mix

5.2.1 Cationic emulsion cold mix

5.2.2 Anionic emulsion cold mix

5.2.3 Non-ionic emulsion cold mix

5.3 Cutback asphalt

5.3.1 Rapid curing (RC) cutback

5.3.2 Medium curing (mc) cutback

5.3.3 Slow curing (SC) cutback

5.4 Foamed asphalt

5.5 Cold recycled mix

5.5.1 Place cold recycling

5.5.2 Central plant cold recycling

5.6 Other types

5.6.1 Polymer modified cold mix

5.6.2 Fiber reinforced cold mix

5.6.3 Additive enhanced cold mix

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

6.1 Key trends

6.2 Road construction

6.2.1 New road construction

6.2.2 Road widening

6.2.3 Temporary roads

6.3 Road maintenance & repair

6.3.1 Pothole patching

6.3.2 Crack sealing

6.3.3 Surface treatment

6.3.4 Emergency repairs

6.4 Pavement rehabilitation

6.4.1 Full depth reclamation

6.4.2 Cold in-place recycling

6.4.3 Base course stabilization

6.5 Other applications

6.5.1 Shoulder construction

6.5.2 Utility cuts restoration

6.5.3 Bike paths & walkways

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

7.1 Key trends

7.2 Highways & expressways

7.2.1 Interstate highways

7.2.2 State highways

7.2.3 Expressways

7.3 Municipal roads

7.3.1 Urban roads

7.3.2 Suburban roads

7.3.3 Rural roads

7.4 Airports

7.4.1 Runways

7.4.2 Taxiways

7.4.3 Aprons

7.5 Parking areas

7.5.1 Commercial parking lots

7.5.2 Residential parking

7.5.3 Industrial parking

7.6 Others

7.6.1 Ports & harbors

7.6.2 Industrial areas

7.6.3 Recreational areas

Chapter 8 Market Estimates and Forecast, By Aggregate Type, 2021 - 2034 (USD Billion) (Kilo Tons)

8.1 Key trends

8.2 Natural aggregates

8.2.1 Crushed stone

8.2.2 Gravel

8.2.3 Sand

8.3 Recycled aggregates

8.3.1 Reclaimed asphalt pavement (RAP)

8.3.2 Recycled concrete aggregate (RCA)

8.3.3 Other recycled materials

8.4 Synthetic aggregates

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)