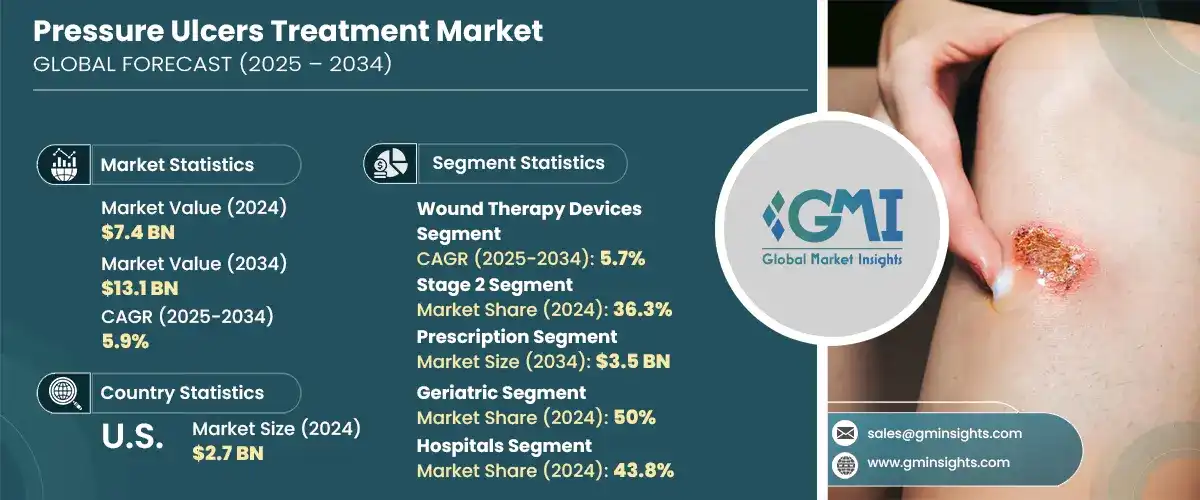

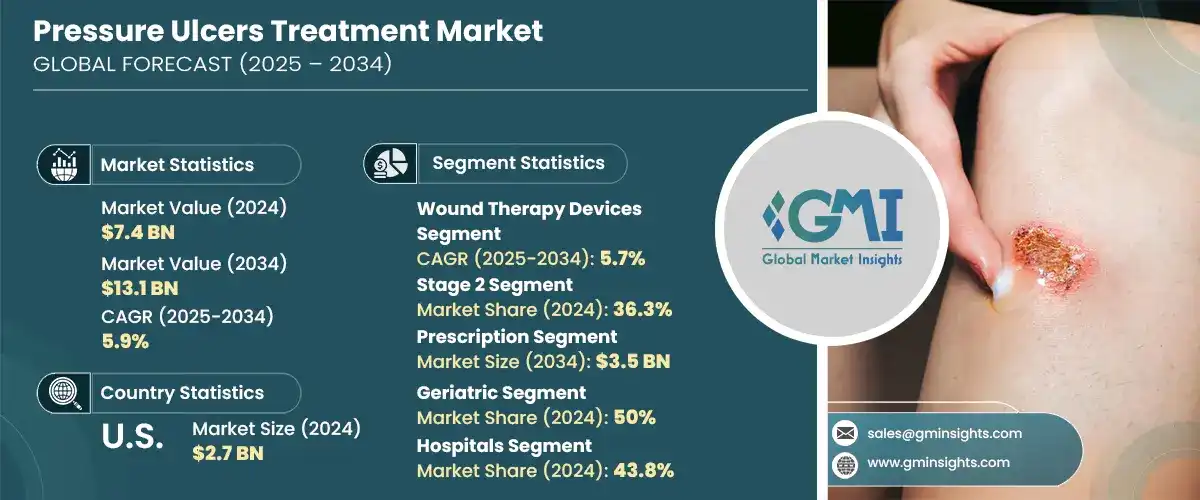

세계의 욕창 치료 시장 규모는 2024년에 74억 달러를 달성하였고, CAGR 5.9%로 성장하여, 2034년에는 131억 달러에 달할 것으로 예측되고 있습니다.

이 성장의 주된 요인은 특히 선진국에서의 인구의 고령화이며, 고령화에 의해 이동이 제한되어 장시간 움직일 수 없는 상태가 계속되면 욕창의 리스크가 높아지고, 고령이 되면 움직임을 방해하는 증상이 나타나기 쉬워져 욕창의 발생으로 이어집니다. 비만과 당뇨병 등 생활습관병이 만연하고 있는 것도 효과적인 상처치료에 대한 수요를 더욱 높이고 있습니다.

시장은 또한 상처 케어 솔루션의 지속적인 기술 개발로부터 혜택을 받고 있습니다. 스마트 상처 드레싱, 생물학적 활성제제, 최신 치료 시스템 등의 기술 혁신은 치유 시간을 단축해 환자의 쾌적성을 향상시킴으로써 욕창 관리에 혁명을 가져오고 있습니다. 또한 조기 개입이나 예방 전략의 이점에 대한 인식이 높아지면서 보다 많은 환자나 의료 제공업체가 선진적인 제품을 선택하고 있습니다. 특히 북미와 유럽에서는 정부의 헬스케어 프로그램에 의한 지원도 채용을 추진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024 |

| 예측연도 | 2025-2034 |

| 시작금액 | 74억 달러 |

| 예측금액 | 131억 달러 |

| CAGR | 5.9% |

욕창 치료에는 체압에 의한 피부 손상의 예방과 치유를 목적으로 하는 다양한 의료 솔루션이 포함됩니다. 욕창은 압박궤양으로도 불리며 일반적으로 이동이 제한된 환자에서 발생합니다. 치료의 목적은 압박을 완화하고 조직 회복을 촉진하며 감염을 예방하여 환자의 건강 상태를 전반적으로 개선하는 것입니다. 치료 옵션으로는 상처 케어를 위해 설계된 특수 드레싱 재료, 생물학적 제제, 치료장비, 약물 등이 있습니다. 임상적 관심이 치료 성적 개선으로 이동함에 따라 여러 치료법을 결합한 통합 치료법이 시장에 침투하고 있습니다.

주요 제품 카테고리 중 상처 치료기구는 2024년에 33억 달러의 평가액으로 최고 점유율을 달성하였으며, 2034년에는 CAGR 5.7%를 보이며 57억 달러로 성장할 것으로 예측되고 있습니다. 이 장비에는 치유를 가속화하고 감염 위험을 줄이며 환자의 불편함을 최소화하는 기술이 포함되어 있습니다. 병원이나 외래에서의 사용이 증가하고 있는 것은 복잡한 상처를 보다 효율적으로 관리하기 위한 첨단 기술에의 의존이 높아지고 있다는 점을 시사하고 있습니다. 최근의 체압 관리 시스템과 자동 상처 모니터링의 개선으로 이 부문의 기능이 더욱 향상되고 임상 채용이 확산되고 있습니다.

유형별로 2024년에는 처방약 분야가 선도하였고 2034년에는 35억 달러에 이를 것으로 추정되고 있습니다. 이 분야의 제품은 보다 복잡하고 만성적인 상처에 처방되는 고급 국소 제제와 전신 요법을 포함하고 있습니다.

최종 용도별로는 병원이 2024년에 43.8%로 최대의 점유율을 차지하였고 2034년에는 55억 달러의 매출이 될 것으로 예측되고 있습니다. 이동이 어려운 환자나 건강상의 문제를 안고 있는 환자는 통합적 접근을 효과적으로 전개할 수 있는 병원에서의 치료를 요구하는 경향이 강합니다. 또한, 외과적 개입이나 집중 치료가 필요한 환자가 최초로 접촉하는 곳은 병원인 경우가 많습니다.

지역별로는 북미가 2024년에 29억 달러의 수익을 올리면서 세계 시장을 선도하였고, 2034년에는 CAGR 5.5%의 성장률로 50억 달러에 이를 것으로 예상되고 있습니다. 이 지역에서는 고령자 수가 증가하고 비만과 당뇨병 등의 합병증의 유병률이 높기 때문에 고급 치료 솔루션이 필요합니다.

주요 기업은 광범위한 제품 포트폴리오, 전략적 R&D 투자, 세계적인 비즈니스 전개를 통해 지위를 지속적으로 강화하고 있습니다. 대기업은 선진적인 상처 관리 솔루션을 적극적으로 개발하여 신흥 경제 국가에서의 존재를 확대하고 있습니다. 합병, 라이선싱 계약, 제품 출시 등의 전략은 경쟁구도 형성에 중요한 역할을 합니다. 신흥기업과 소규모기업도 특수 생물제제와 맞춤형 케어 옵션에 주력함으로써 틈새 시장을 개척해 업계 내 혁신의 속도를 높이고 있습니다.

The Global Pressure Ulcers Treatment Market was valued at USD 7.4 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 13.1 billion by 2034. A major contributor to this growth is the aging population, particularly in developed nations, where limited mobility and prolonged immobility increase the risk of pressure ulcers. As individuals age, they are more likely to develop conditions that hinder movement, leading to the development of pressure sores. Additionally, the rising prevalence of lifestyle-related diseases such as obesity and diabetes-both of which are known to slow wound healing-further drives demand for effective wound care therapies. The growing incidence of chronic illnesses is translating into increased clinical cases of non-healing wounds, spurring the demand for sophisticated treatment approaches that improve patient outcomes.

The market is also benefiting from ongoing technological developments in wound care solutions. Innovations such as smart wound dressings, biologically active products, and modern therapy systems are revolutionizing pressure ulcer management by reducing healing time and improving comfort for patients. These solutions are increasingly adopted across both hospital settings and homecare environments due to their effectiveness in managing complex wounds. Greater awareness about early intervention and the benefits of preventive strategies is encouraging more patients and healthcare providers to opt for advanced products. Support from government healthcare programs, particularly in North America and Europe, is also bolstering adoption. Reimbursement schemes and clinical guidelines are reinforcing the preference for evidence-based wound care methods.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.4 Billion |

| Forecast Value | $13.1 Billion |

| CAGR | 5.9% |

Pressure ulcer treatment encompasses a range of medical solutions aimed at preventing and healing pressure-induced skin injuries. These ulcers, also referred to as bedsores or decubitus ulcers, generally occur in patients with limited mobility. The goal of treatment is to relieve pressure, promote tissue recovery, prevent infection, and enhance overall patient health. Therapeutic options include specialized dressings, biologics, therapy devices, and pharmaceutical agents designed for wound care. As clinical attention shifts toward improving healing outcomes, integrated treatment approaches that combine multiple therapies are gaining ground in the market.

Among the key product categories, wound therapy devices emerged as the top-performing segment in 2024 with a valuation of USD 3.3 billion and are projected to grow to USD 5.7 billion by 2034, registering a CAGR of 5.7%. These devices include technologies that support faster healing, reduce infection risk, and minimize patient discomfort. Their increasing use in hospitals and outpatient settings highlights the growing reliance on advanced technology to manage complex wounds more efficiently. Recent improvements in pressure management systems and automated wound monitoring are further enhancing the capabilities of this segment, leading to broader clinical adoption.

In terms of type, the prescription segment led in 2024 and is estimated to reach USD 3.5 billion by 2034. This dominance can be attributed to the higher efficacy of prescription therapies and the medical necessity for regulated interventions in treating severe cases. Products in this category include advanced topical formulations and systemic therapies that are prescribed for more complex or chronic wounds. As healthcare providers increasingly favor personalized treatment plans based on patient needs, the prescription category is expected to maintain its lead over the coming years.

By end use, hospitals represented the largest share of the market in 2024, accounting for 43.8%, and are projected to generate USD 5.5 billion in revenue by 2034. Hospitals remain the primary centers for treating pressure ulcers, particularly in advanced stages, owing to their comprehensive infrastructure, availability of skilled medical staff, and specialized departments for wound care. Patients with limited mobility or underlying health issues are more likely to seek hospital-based care where multidisciplinary approaches can be deployed effectively. Additionally, hospitals are often the first point of contact for patients requiring surgical intervention or intensive care.

Regionally, North America led the global market with a revenue of USD 2.9 billion in 2024 and is expected to reach USD 5 billion by 2034, growing at a CAGR of 5.5%. This leadership is supported by a well-established healthcare framework, early adoption of cutting-edge wound care technologies, and substantial investment in clinical research and development. The rising number of elderly individuals and the high prevalence of comorbid conditions such as obesity and diabetes in the region make advanced treatment solutions a necessity. Furthermore, favorable reimbursement scenarios and strong regulatory oversight have enabled a structured rollout of innovative therapies.

Leading companies continue to strengthen their positions through extensive product portfolios, strategic R&D investment, and global reach. Major participants are actively developing advanced wound management solutions and expanding their presence in emerging economies. Competitive strategies such as mergers, licensing agreements, and product launches are playing a vital role in shaping the landscape. Startups and smaller firms are also carving out a niche by focusing on specialized biologics and customizable care options, intensifying the pace of innovation within the industry.