신에너지차 스태빌라이저 시장(2025-2034년) : 기회, 성장 촉진요인, 산업 동향 분석, 예측

New Energy Vehicle Stabilizer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1773335

리서치사:Global Market Insights Inc.

발행일:2025년 06월

페이지 정보:영문 190 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

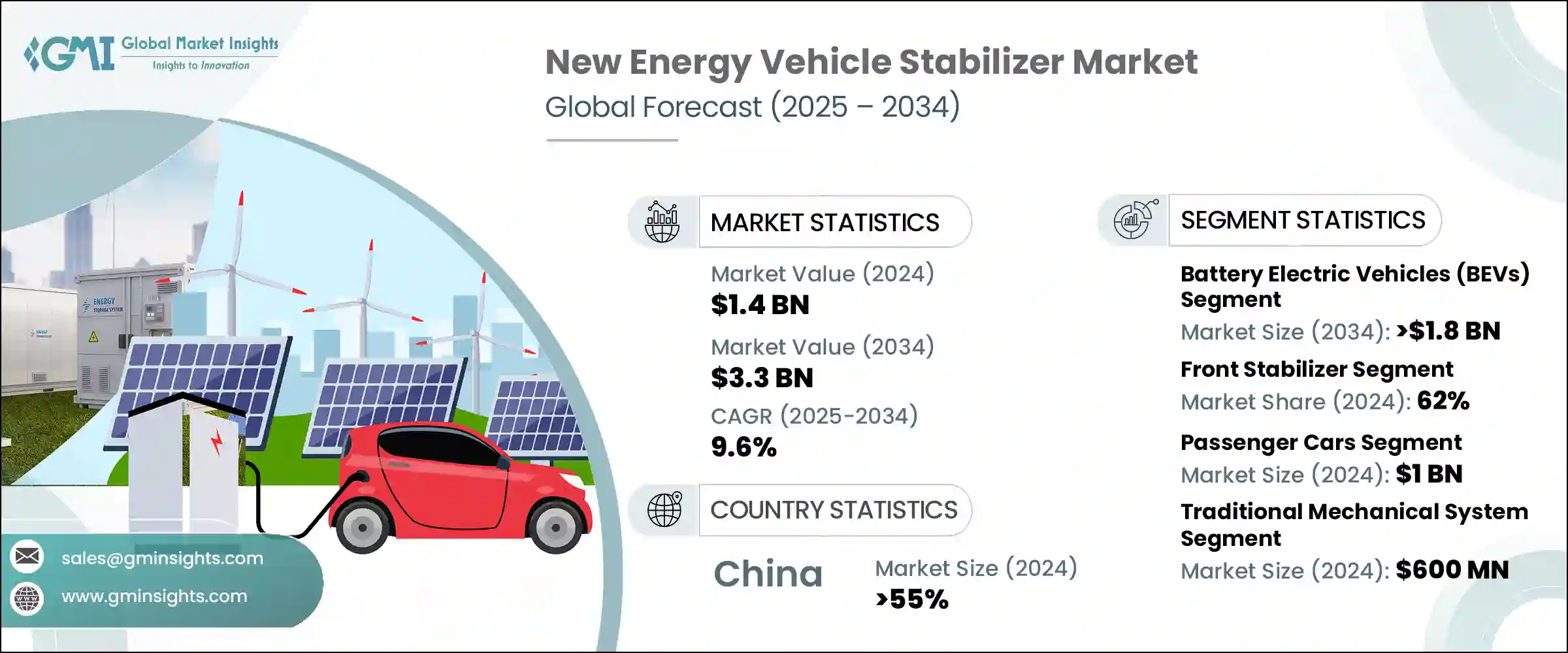

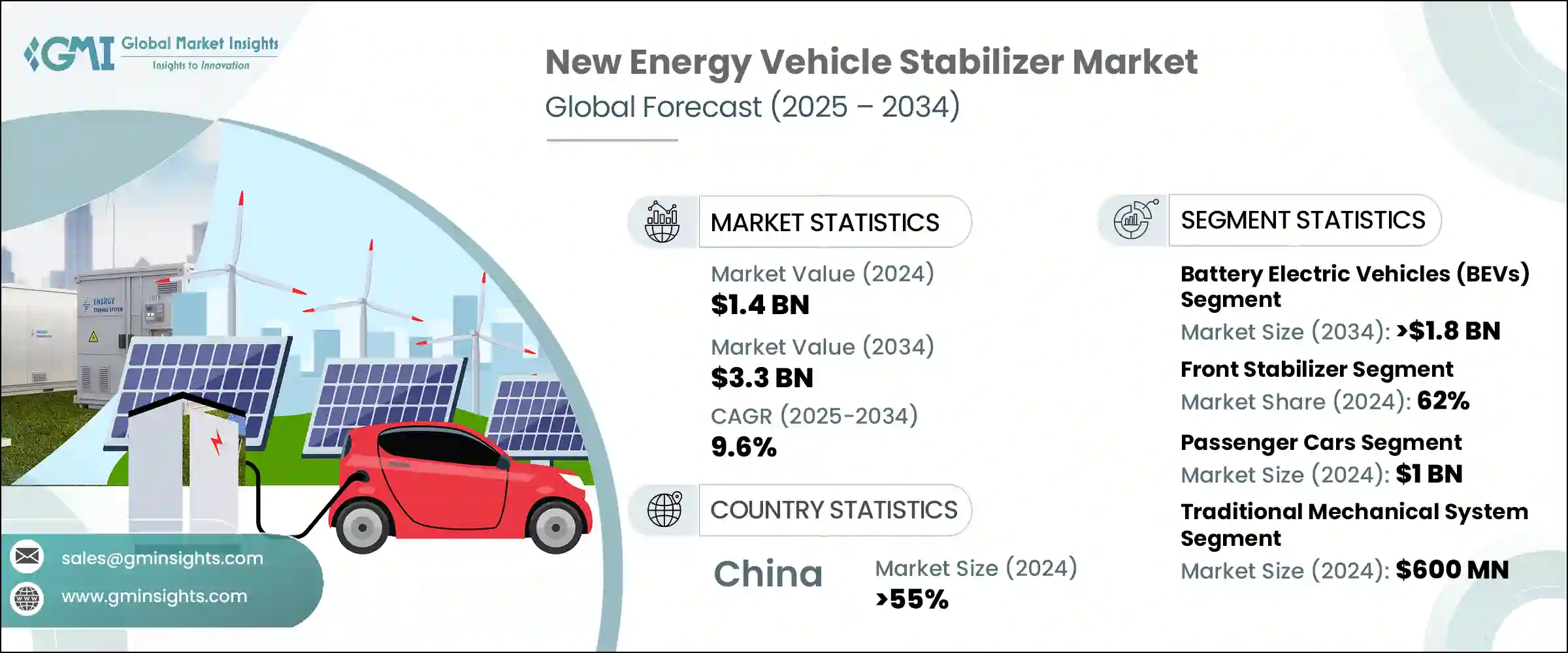

세계의 신에너지차 스태빌라이저 시장은 2024년에는 14억 달러로 평가되었고 CAGR 9.6%로 성장하여 2034년까지는 33억 달러에 이를 것으로 추정되고 있습니다. 주요 시장에서 전기자동차, 하이브리드 자동차, 수소 자동차의 채용이 증가하고 있는 것이 큰 성장요인이 되고 있습니다. 차량 역학과 전반적인 승차품질 향상을 위한 노력이 첨단 스태빌라이저 기술 수요를 직접 뒷받침하고 있습니다. 전자기계식 및 액티브 스태빌라이저는 운전자에게 부드러운 핸들링을 제공하는 능력으로 널리 채택되고 있습니다.

스태빌라이저(주로 스태빌라이저 바 또는 안티롤 바로 불림)는 특히 배터리의 탑재에 의해 중량 배분이 변화하는 NEV의 서스펜션 시스템을 지원하는데 중요한 역할을 합니다. NEV는 배터리팩을 차량 플로어에 탑재하는 경향이 있기 때문에 무게 중심이 이동하며 따라서 스태빌라이저 시스템의 재검토가 필요합니다.

시장 범위

시작연도

2024년

예측연도

2025-2034년

시작금액

14억 달러

예측금액

33억 달러

CAGR

9.6%

배터리 전기자동차(BEV)는 2024년에 46%의 점유율을 차지했으며, 2034년까지는 18억 달러 시장 규모에 이를 것으로 예측되고 있습니다. 이러한 성장은 우호적인 정책 환경, 충전 인프라 확대, 그리고 현대, Volkswagen, Tesla, BYD와 같은 세계적인 OEM의 엄청난 투자로 인한 것입니다.

2024년에는 전면 스태빌라이저 바 부문이 세계의 신에너지차 스태빌라이저 시장을 선도하며 62%의 점유율을 차지하였고, 2034년까지의 CAGR은 8.2%로 예측되고 있습니다. 전기자동차는 전륜구동 방식을 채용하는 경우가 많고, 배터리의 질량이 전차축에 집중하기 때문에 전면 스태빌라이저는 실시간 운전 상황에서 정확한 핸들링을 제공하여 차체의 움직임을 억제하기 위해 필수적인 요소가 되고 있습니다.

아시아태평양의 신에너지차 스태빌라이저 시장은 2024년에는 55%의 점유율을 차지했으며 3억 달러를 창출했습니다. NEV 제조의 급속한 가속으로 인한 지속적인 규제 지원과 국내 수요 증가는 이러한 성장의 주요 촉진요인입니다. 중국은 세계 최대의 NEV 시장으로서의 지위를 확립하고 있으며, 그 지위는 적극적인 국가 전략과 투자에 의해 강화되고 있습니다. NIO, XPeng, BYD, Geely 등의 현지 브랜드와 Tesla, Volkswagen 등의 세계 자동차 업체들은 급증하는 수요에 대응하기 위해 이 지역에서 생산거점을 계속 확대하고 있습니다.

신에너지차 스태빌라이저 시장에서 사업을 전개하고 있는 주요 기업으로는 Sogefi Group, Thyssenkrupp, DAEWON, ZF, Dongfeng, NHK International, SwayTec, Hendrickson, Kongsberg Automotive, Mubea 등이 있습니다. NEV용 스태빌라이저 부문에 속한 기업은 차세대 EV 플랫폼의 혁신과 통합을 적극적으로 추구하고 있습니다. 이들 중 많은 부분이 진화하는 전동 드라이브트레인의 역학에 맞는 가볍고 강도 높은 스태빌라이저 부품을 개발하기 위한 연구개발에 투자하고 있습니다. EV 제조업체와 협력하여 초기 단계부터 설계에 관여함으로써 맞춤형 서스펜션 시스템을 실현할 수 있습니다. 기업은 또한 온보드 센서 및 제어유닛과 연동하여 실시간으로 성능을 발휘하는 적응기술 및 전기기계기술을 도입하고 있습니다. 지역에 뿌리를 둔 생산거점과 OEM과의 장기적인 공급업체 계약을 통해 세계 시장에 전개함으로써, 이러한 기업은 시장 진입을 강화하고 있습니다.

목차

제1장 조사방법과 범위

제2장 주요 요약

제3장 업계 인사이트

업계 생태계 분석

공급자의 상황

원재료 공급자

부품 제조업체

기술공급자

애프터마켓 공급업체

시스템 통합자

비용구조

이익률

각 단계에서의 부가가치

공급망에 영향을 미치는 요인

파괴자

영향요인

성장 촉진요인

전기차와 하이브리드차에 대한 정부의 의무와 소비자 수요 증가

NEV에서의 승차감 제어와 핸들링 성능의 향상에 대한 수요

기계식 스태빌라이저에서 인텔리전트 센서 통합형 스태빌라이저로의 전환

적응형 및 단절형 스태빌라이저 시스템의 필요성 증가

업계의 잠재적 리스크 및 과제

전기기계 및 능동시스템

공간적 제약에 의한 포장 과제

시장 기회

전동 오프로드 차량의 퍼포먼스 파트와 커스터마이즈의 성장

무선(OTA) 스태빌라이저의 튜닝 및 제어 솔루션 시장 개척

성장 가능성 분석

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현재의 기술

신흥기술

특허 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

생산통계

생산거점

소비거점

수출과 수입

코스트 내역 분석

지속 가능성 분석

지속 가능한 관행

폐기물 감축 전략

생산에서의 에너지 효율

환경친화적인 노력

탄소발자국의 고려

제4장 경쟁구도

소개

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병과 인수

파트너십 및 협업

신제품 발매

확장계획과 자금조달

제5장 시장 추계 및 예측 : 차량별(2021-2034년)

주요 동향

배터리 전기자동차(BEV)

플러그인 하이브리드 전기자동차(PHEV)

하이브리드 전기자동차(HEV)

연료전지 전기자동차(FCEV)

제6장 시장 추계 및 예측 : 스태빌라이저(2021-2034년)

주요 동향

전면 스태빌라이저

후면 스태빌라이저

제7장 시장 추계 및 예측 : 기술별(2021-2034년)

주요 동향

유압 스태빌라이저 시스템

전기기계식 스태빌라이저 시스템

전자제어 스태빌라이저 바

전통적인 기계 시스템

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

승용차

세단

해치백

SUV

MUV

상용차

소형상용차

중형상용차

대형상용차

제9장 시장 추계 및 예측 : 판매채널별(2021-2034년)

주요 동향

OEM

애프터마켓

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

우크라이나

러시아

노르딕

아시아태평양

중국

인도

일본

호주

한국

동남아시아

라틴아메리카

브라질

멕시코

아르헨티나

칠레

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제11장 기업 프로파일

AAM

ADDCO

Chuo Spring

DAEWON

Dongfeng

JAMNA AUTO INDUSTRIES LIMITED

Sogefi Group

Kongsberg Automotive

Mubea

NHK International

Hendrickson

Sogefi

SwayTec

Tata

Thyssenkrupp

Tinsley Bridge

TMT(CSR)

Tower

Wanxiang

Yangzhou Dongsheng

ZF

CSM

영문 목차

영문목차

The Global New Energy Vehicle Stabilizer Market was valued at USD 1.4 billion in 2024 and is estimated to grow at a CAGR of 9.6% to reach USD 3.3 billion by 2034. This growth is largely fueled by the increasing adoption of electric, hybrid, and hydrogen-powered vehicles across major global markets. As manufacturers shift to alternative drivetrains, there is a rising emphasis on vehicle dynamics and overall ride quality, which directly boosts the demand for advanced stabilizer technologies. Electromechanical and active stabilizers are becoming more widely adopted due to their ability to enhance suspension performance, reduce body roll, and provide smoother handling for both passengers and drivers. This reflects a broader trend in the EV sector to deliver high levels of safety and comfort.

Stabilizers-often called sway or anti-roll bars-play a crucial role in supporting the suspension systems of NEVs, especially given the altered weight distribution brought on by battery placement. Unlike conventional internal combustion engine (ICE) vehicles, NEVs tend to house battery packs on the vehicle floor, shifting the center of gravity and requiring reimagined stabilizer systems. These systems are designed to ensure optimal performance and cornering stability, particularly during high-speed maneuvers or rapid direction changes.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$1.4 Billion

Forecast Value

$3.3 Billion

CAGR

9.6%

Battery Electric Vehicles (BEVs) commanded a 46% share in 2024, and the segment is anticipated to generate USD 1.8 billion by 2034. The strong foothold of BEVs in the stabilizer market is backed by surging production and consumer demand for all-electric platforms. This increase is due to supportive policy environments, expanded charging infrastructure, and significant investment from global OEMs like Hyundai, Volkswagen, Tesla, and BYD. Heavier battery weights in BEVs necessitate specially engineered suspension systems, increasing the reliance on advanced stabilizer components.

In 2024, the front stabilizer bars segment led the global new energy vehicle stabilizer market, accounting for 62% share, and is forecasted to grow at a CAGR of 8.2% through 2034. This dominance stems from their critical role in managing front-axle stability and maintaining vehicle balance. As electric vehicles frequently adopt front-wheel drive configurations and concentrate battery mass on the front axle, front stabilizers have become indispensable in ensuring precise handling and reduced body movement in real-time driving conditions.

Asia Pacific New Energy Vehicle Stabilizer Market held a 55% share and generated USD 300 million in 2024. The rapid acceleration of NEV manufacturing sustained regulatory support, and increasing domestic demand are key drivers of this growth. China has established itself as the largest NEV market worldwide, a position reinforced by aggressive national strategies and investment. Local brands like NIO, XPeng, BYD, and Geely, as well as global automakers such as Tesla and Volkswagen, have continued to expand their production footprints in the region to meet this surging demand.

Leading players operating in the New Energy Vehicle Stabilizer Market include Sogefi Group, Thyssenkrupp, DAEWON, ZF, Dongfeng, NHK International, SwayTec, Hendrickson, Kongsberg Automotive, and Mubea. Companies in the NEV stabilizer segment are aggressively pursuing innovation and integration with next-gen EV platforms. Most are investing in R&D to develop lighter, high-strength stabilizer components that match the evolving dynamics of electric drivetrains. Collaborations with EV manufacturers for early-stage design involvement allow for customized suspension systems. Firms are also incorporating adaptive and electromechanical technologies that work with onboard sensors and control units for real-time performance. Global expansion through localized production hubs and long-term supplier agreements with OEMs helps these players strengthen their market reach.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Research design

1.1.1 Research approach

1.1.2 Data collection methods

1.2 Base estimates & calculations

1.2.1 Base year calculation

1.2.2 Key trends for market estimation

1.3 Forecast model

1.4 Primary research and validation

1.4.1 Primary sources

1.4.2 Data mining sources

1.5 Market scope & definition

Chapter 2 Executive Summary

2.1 Industry synopsis, 2021 – 2034

2.2 Key market trends

2.2.1 Regional

2.2.2 Vehicle

2.2.3 Stabilizer

2.2.4 Technology

2.2.5 Application

2.2.6 Sales Channel

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Key decision points for industry executives

2.4.2 Critical success factors for market players

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.1.1 Raw material suppliers

3.1.1.2 Component manufacturers

3.1.1.3 Technology providers

3.1.1.4 Aftermarket suppliers

3.1.1.5 System integrators

3.1.2 Cost structure

3.1.3 Profit margin

3.1.4 Value addition at each stage

3.1.5 Factors impacting the supply chain

3.1.6 Disruptors

3.2 Impact on forces

3.2.1 Growth drivers

3.2.1.1 Increasing government mandates and consumer demand for electric and hybrid vehicles

3.2.1.2 Demand for enhanced ride control and handling performance in NEVs

3.2.1.3 Shift from mechanical to intelligent, sensor-integrated stabilizers

3.2.1.4 Increased need for adaptive and disconnecting stabilizer systems

3.2.2 Industry pitfalls & challenges

3.2.2.1 Especially electromechanical and active systems

3.2.2.2 Packaging challenges due to space constraints

3.2.3 Market Opportunities

3.2.3.1 Growth in performance parts and customization in electric off-road vehicles

3.2.3.2 Opens door for over-the-air (OTA) stabilizer tuning and control solutions