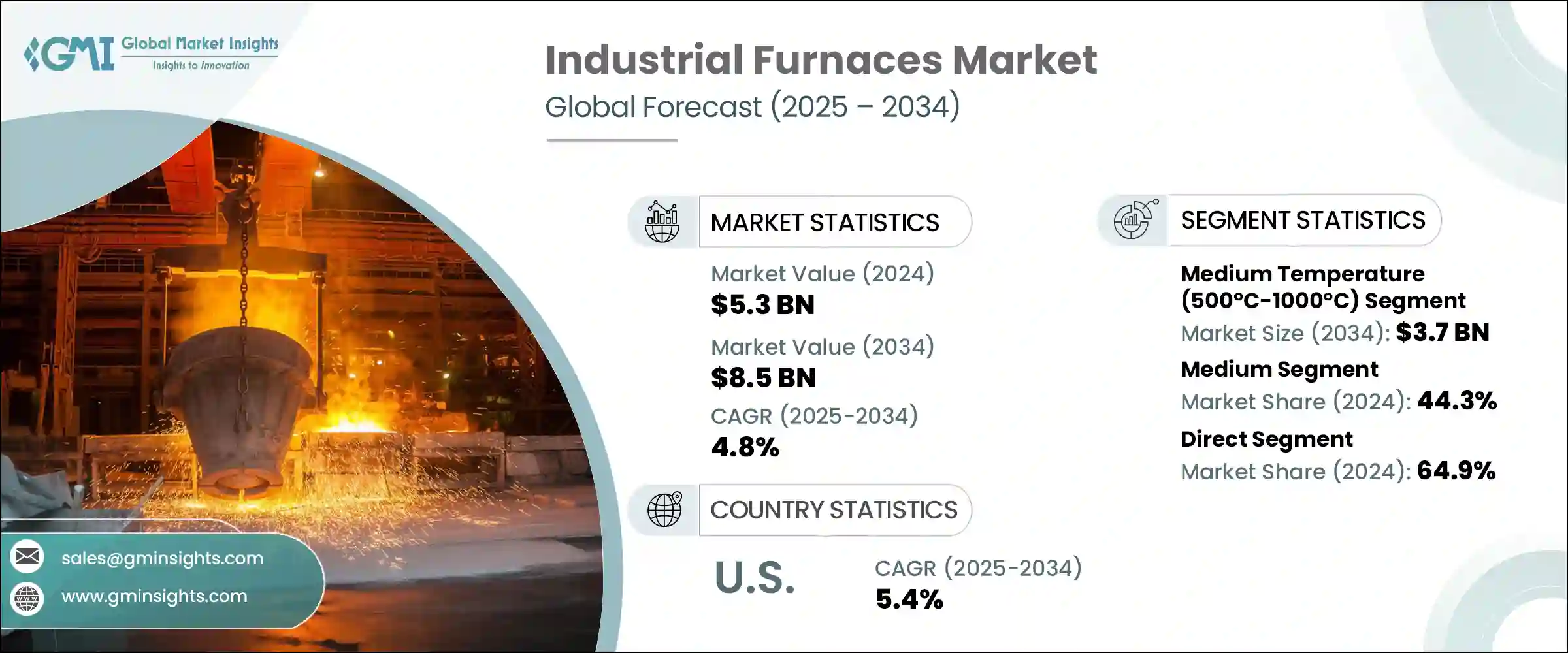

세계의 산업용 용광로 시장 규모는 2024년에 53억 달러를 달성하였고, CAGR 4.8%로 성장하여 2034년까지는 85억 달러에 이를 것으로 예측되고 있습니다. 산업용 용광로는 용융, 어닐링, 템퍼링 등의 고온 공정에 필수적이기 때문에 금속 및 철강 산업이 시장 성장에 크게 공헌하고 있습니다. 특히 중국, 인도, 미국 등의 지역에서 기존에 비해 배출량이 적고 에너지 효율이 높은 전기아크로(EAF)의 채용이 증가하고 있는 것도 중요한 동향입니다.

탈탄소화에 대한 관심 증가와 더불어 산업계는 이산화탄소 배출량을 줄이기 위해 수소화염 및 전기아크와 같은 대체 가열기술에 대한 관심을 높여 왔습니다. 예를 들어 수소화염은 수증기만을 배출하는 깨끗한 연소 방법이며, 고온 공정에서의 배출량 감축에 매력적인 선택입니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024 |

| 예측연도 | 2025-2034년 |

| 시작금액 | 53억 달러 |

| 예측금액 | 85억 달러 |

| CAGR | 4.8% |

산업용 용광로 시장의 중온 부문은 2024년에 22억 달러를 창출하였고 2034년까지는 37억 달러에 이를 것으로 예측됩니다. 500°C에서 1000°C 사이에서 작동하는 중온로는 다용도성과 다양한 열처리 공정에 대한 대응 능력으로 인해 세계 시장에서 지배적인 부문이 되고 있습니다. 이 용광로는 금속과 합금을 처리하는 능력으로 자동차 및 항공우주에서 전자장비 제조에 이르기까지 모든 산업에서 널리 사용됩니다.

중용량로 부문은 2024년에 44.3%의 점유율을 차지하였고 2034년까지 연평균 복합 성장률(CAGR) 4.4%를 보일 것으로 예측됩니다. 이러한 용광로는 빈번한 온도 사이클과 중간 정도의 처리 능력을 필요로 하는 중규모 산업 분야에서 특히 선호됩니다. 기계제조, 자동차부품 제조, 주조 등의 산업은 일관된 품질관리 및 생산 요구사항을 충족하기 위해 중온로에 의존합니다.

미국의 산업용 용광로 시장은 2024년에 7억 달러로 평가되었으며, 2034년까지의 CAGR은 5.4%로 강력한 성장이 예측되고 있습니다. 미국은 첨단 제조능력과 에너지 효율이 높은 용광로 기술의 채용 증가로 북미 산업용 용광로 시장을 선도하고 있습니다. 금속 가공공장, 항공우주공장, 자동차산업은 배출가스 절감과 생산성 향상을 위해 노력하고 있으며, 새로운 고효율 산업용 용광로 수요를 견인하고 있습니다. 북미에서도 특히 미국, 캐나다, 멕시코는 이 지역의 성숙한 제조거점과 지속 가능한 생산 방식에 대한 주력으로 세계 시장에서 큰 점유율을 차지하고 있습니다.

산업용 용광로 시장의 주요 기업은 Harper International, SECO/WARWICK SA, Tenova SpA, Despatch Industries, Carbolite Gero, Lindberg/MPH, Gasbarre Thermal Processing Systems, Nabertherm GmbH, Inductotherm Group, Surface Combustion, Inc., ABB, Ipsen International GmbH Bickley, ANDRITZ AG 등이 있습니다. 산업용 용광로 시장의 기업은 그 지위를 강화하기 위해 몇 가지 중요한 전략을 채택하고 있습니다.

각 회사는 전기아크로(EAF)의 성능을 향상시키고 탈탄소 목표를 달성하기 위해 수소화염과 같은 대체 수단을 모색하는 연구개발에 많은 투자를 실시했습니다. 또한 협력을 통해 세계적인 풋프린트를 확대하기 위해 노력하고 있습니다. 또 다른 전략은 다양한 업계의 특정 요구를 충족시키기 위해 맞춤형 솔루션을 제공함으로써 시장 매력을 높이고 장기적인 고객 관계를 확보하는 것입니다.

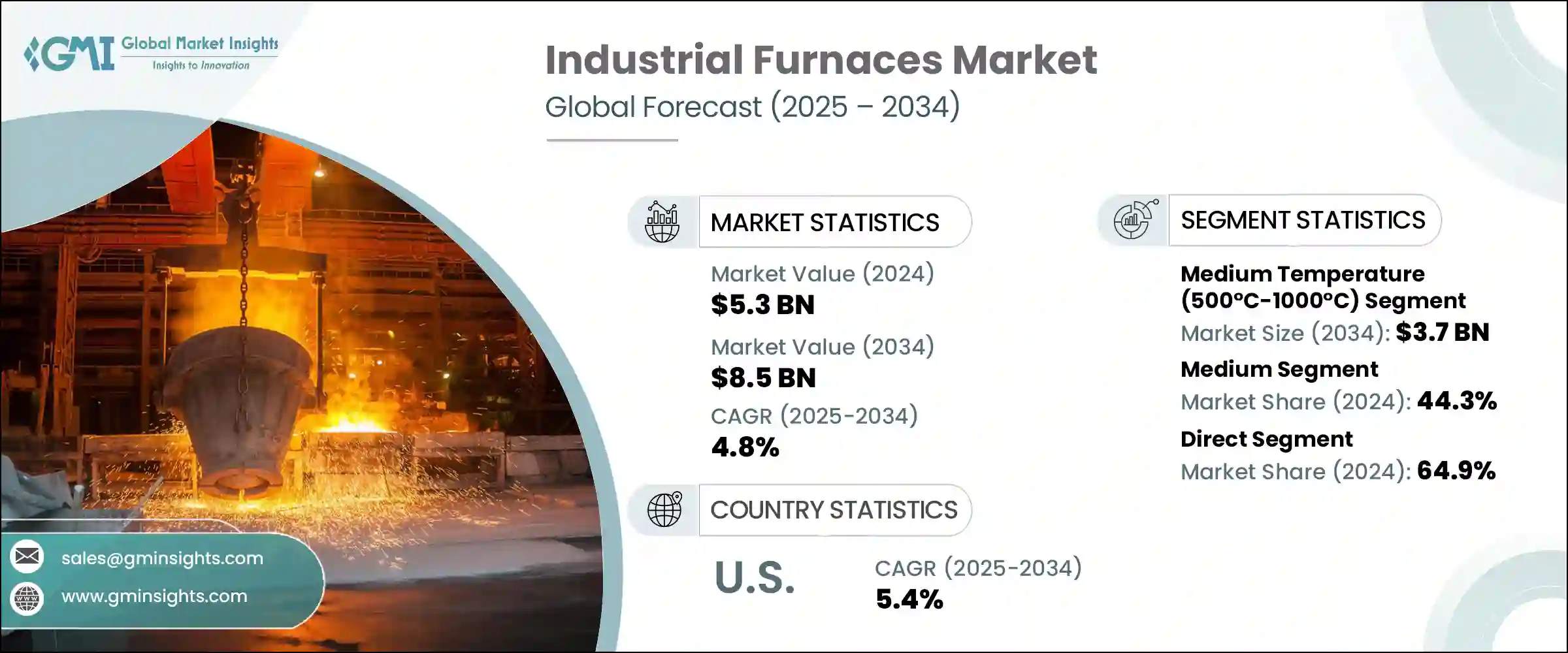

The Global Industrial Furnaces Market was valued at USD 5.3 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 8.5 billion by 2034. The metal and steel industries are key contributors to this growth, as industrial furnaces are essential for high-temperature processes such as melting, annealing, and tempering, which are required for shaping and treating metals. Rising demand for infrastructure, automotive production, and industrial development, particularly in regions like China, India, and the U.S., is driving the need for more efficient and durable furnaces. The increasing adoption of electric arc furnaces (EAFs), which offer lower emissions and higher energy efficiency compared to traditional blast furnaces, is another important trend. EAFs now account for approximately 30% of global steel production, further increasing the demand for advanced furnace technologies worldwide.

In addition to the rising focus on decarbonization, industries are increasingly turning to alternative heating technologies like hydrogen flames and electric arcs to reduce their carbon footprint. These alternatives are seen as key solutions in the transition to more sustainable manufacturing processes. Hydrogen flames, for example, offer a clean burning option that emits only water vapor, making them an attractive choice for reducing emissions in high-temperature processes. Electric arc furnaces (EAFs), already popular in steel production, are also being explored for their ability to reduce carbon emissions compared to traditional furnace technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.3 Billion |

| Forecast Value | $8.5 Billion |

| CAGR | 4.8% |

The medium-temperature segment of the industrial furnaces market generated USD 2.2 billion in 2024 and is expected to reach USD 3.7 billion by 2034. Medium-temperature furnaces, which operate between 500°C and 1000°C, remain a dominant segment in the global market due to their versatility and ability to handle various heat-treatment processes. These furnaces are widely used across industries, from automotive and aerospace to electronics manufacturing, due to their ability to process metals and alloys.

The medium-capacity segment accounted for a 44.3% share in 2024 and is expected to grow at a CAGR of 4.4% through 2034. These furnaces are particularly favored for mid-sized industrial applications that require frequent temperature cycling and moderate throughput. Industries such as machinery manufacturing, auto parts production, and foundries rely on medium-temperature furnaces for consistent quality control and fulfilling production requirements.

United States Industrial Furnaces Market was valued at USD 700 million in 2024, with projections showing strong growth at a CAGR of 5.4% through 2034. The U.S. continues to lead the North American industrial furnaces market due to its advanced manufacturing capabilities and the increasing adoption of energy-efficient furnace technologies. Metal processing plants, aerospace workshops, and the automotive industry are driving demand for new, high-efficiency industrial furnaces, as these sectors work to reduce emissions and improve productivity. North America, particularly the U.S., Canada, and Mexico, holds a significant share of the global market due to the region's mature manufacturing base and focus on sustainable production practices.

Key players in the Industrial Furnaces Market include Harper International, SECO/WARWICK S.A., Tenova S.p.A., Despatch Industries, Carbolite Gero, Lindberg/MPH, Gasbarre Thermal Processing Systems, Nabertherm GmbH, Inductotherm Group, Surface Combustion, Inc., ABB, Ipsen International GmbH, Wisconsin Oven Corporation, Nutec Bickley, and ANDRITZ AG. Companies in the industrial furnaces market are adopting several key strategies to strengthen their position. One of the main approaches is focusing on technological innovation, such as the development of more energy-efficient and sustainable furnaces.

Companies are investing heavily in research and development to improve the performance of electric arc furnaces (EAFs) and explore alternatives like hydrogen flames to meet decarbonization targets. Additionally, these companies are working on expanding their global footprint through strategic partnerships and collaborations with manufacturers in key industries, such as automotive, aerospace, and metal processing. Another strategy is offering customized solutions to meet the specific needs of various industries, enhancing their market appeal and ensuring long-term customer relationships.