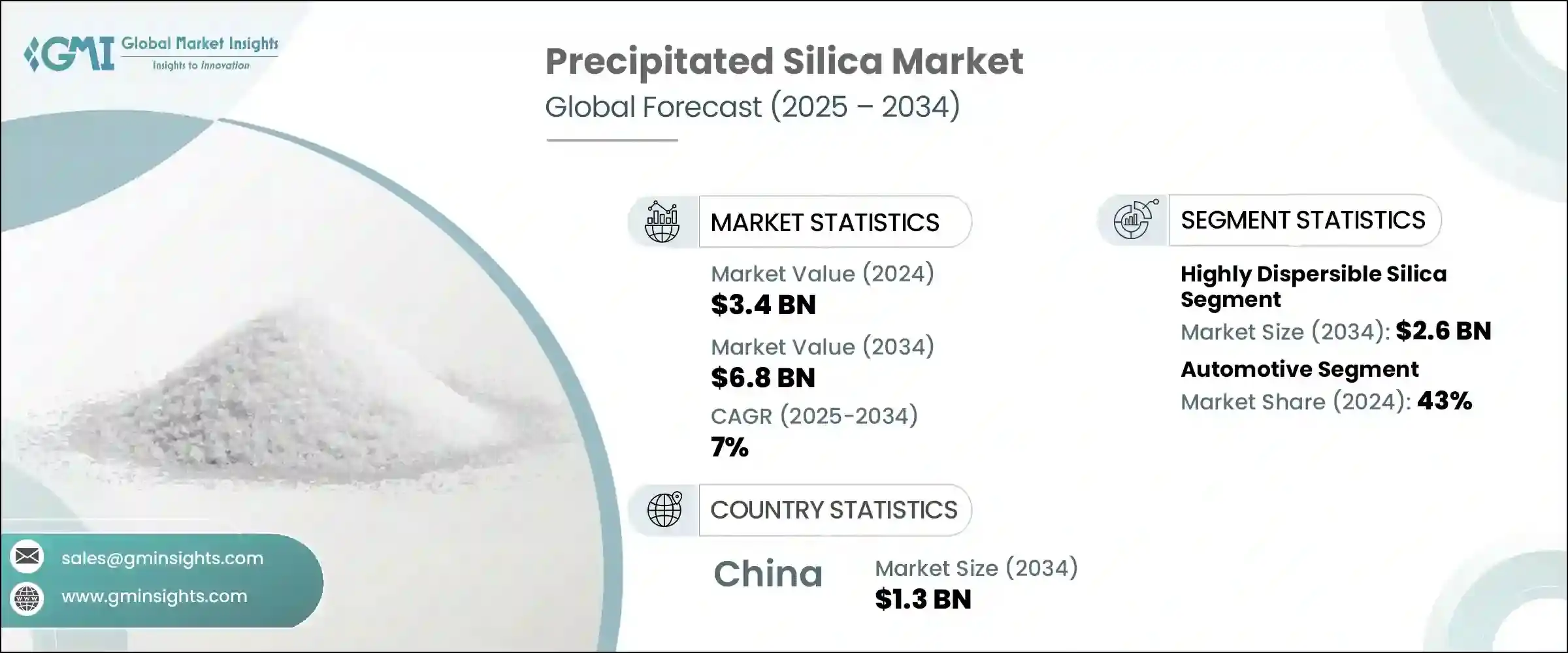

세계의 침전 실리카 시장은 2024년에는 34억 달러로 평가되며, CAGR 7%로 성장하며, 2034년에는 68억 달러에 달할 것으로 추정되고 있습니다.

이러한 시장 성장의 원동력은 침전 실리카의 독특한 물리적, 화학적 특성으로 인해 다양한 산업에서 다용도한 성분으로 활용되고 있습니다. 지난 10년간 침전 실리카 수요는 꾸준히 증가하고 있으며, 특히 고무, 구강 관리 제품, 코팅제의 성능 향상 첨가제로서 주목받고 있습니다. 급속한 도시화, 자동차 생산량 증가, 친환경 기술 중시 등의 지속적인 추세는 시장을 계속 발전시키고 있습니다.

침전 실리카는 지속가능성 목표에 부합하면서 제품 성능을 향상시킬 수 있으므로 지속적인 채택이 예상됩니다. 아시아태평양의 신흥 경제 국가들은 산업 개발의 가속화, 자동차 부문의 확대, 소비재 시장의 호황으로 인해 이러한 성장의 대부분을 주도하고 있습니다. 중국과 인도와 같은 국가들은 대규모 소비국일 뿐만 아니라 주요 생산 기지로 발전하고 있으며, 이 분야에서 이 지역의 우위를 더욱 공고히 하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025-2034년 |

| 시작 금액 | 34억 달러 |

| 예측 금액 | 68억 달러 |

| CAGR | 7% |

타이어 및 고무 산업은 여전히 침전 실리카 응용의 핵심입니다. 침전 실리카는 견인력 강화, 구름 저항 감소, 연비 향상에 중요한 역할을 하므로 특히 전기자동차 및 고성능 자동차를 위한 최신 타이어 배합에 없어서는 안 될 필수 요소입니다. 타이어뿐만 아니라 침전 실리카의 용도는 의약품, 식품 가공, 퍼스널케어 제품, 고결 방지제, 증점제, 세정제 등 다양한 분야로 확대되고 있습니다.

고분산성 실리카(HDS)는 2024년 13억 달러를 차지하며, 2034년에는 26억 달러에 달할 것으로 예상되며, 연평균 7.1%의 성장률을 보일 것으로 예측됩니다. HDS는 우수한 보강 능력과 타이어 고무 컴파운드와의 호환성을 바탕으로, 특히 하이브리드 및 전기자동차를 위한 친환경 고성능 타이어 제조에 필수적인데, HDS는 구름 저항, 습식 트랙션 및 연비를 크게 향상시키기 때문에 특히 하이브리드 및 전기자동차를 위한 친환경 타이어 제조에 필수적입니다. 이는 전 세계에서 강화되는 환경 규제와 OEM(주문자 상표 부착 생산)의 저연비 제품 수요에 부합합니다. 저공해 차량과 친환경 타이어 솔루션으로의 전환은 HDS의 채택을 촉진하고 미래 타이어 기술의 핵심 소재로서 HDS의 입지를 강화하고 있습니다.

2024년에는 자동차 분야가 43%의 점유율을 차지합니다. 실리카는 회전 저항을 감소시켜 타이어의 접지력, 내마모성, 연비 효율을 향상시킵니다. 전 세계에서 에너지 효율이 높고 저공해 자동차가 부상함에 따라 제조업체들은 규제 기준과 고객 선호도를 충족시키기 위해 실리카 강화 타이어의 채택을 늘리고 있습니다. 전기자동차와 하이브리드차의 생산량이 급증하면서 견인력 강화와 주행거리 연장을 위해 침전 실리카에 크게 의존하는 고성능 타이어에 대한 수요가 증가하고 있습니다. 자동차 제조업체들이 지속가능한 고품질 타이어 소재를 우선시하고 있으므로 이러한 추세는 앞으로도 지속될 것으로 예측됩니다.

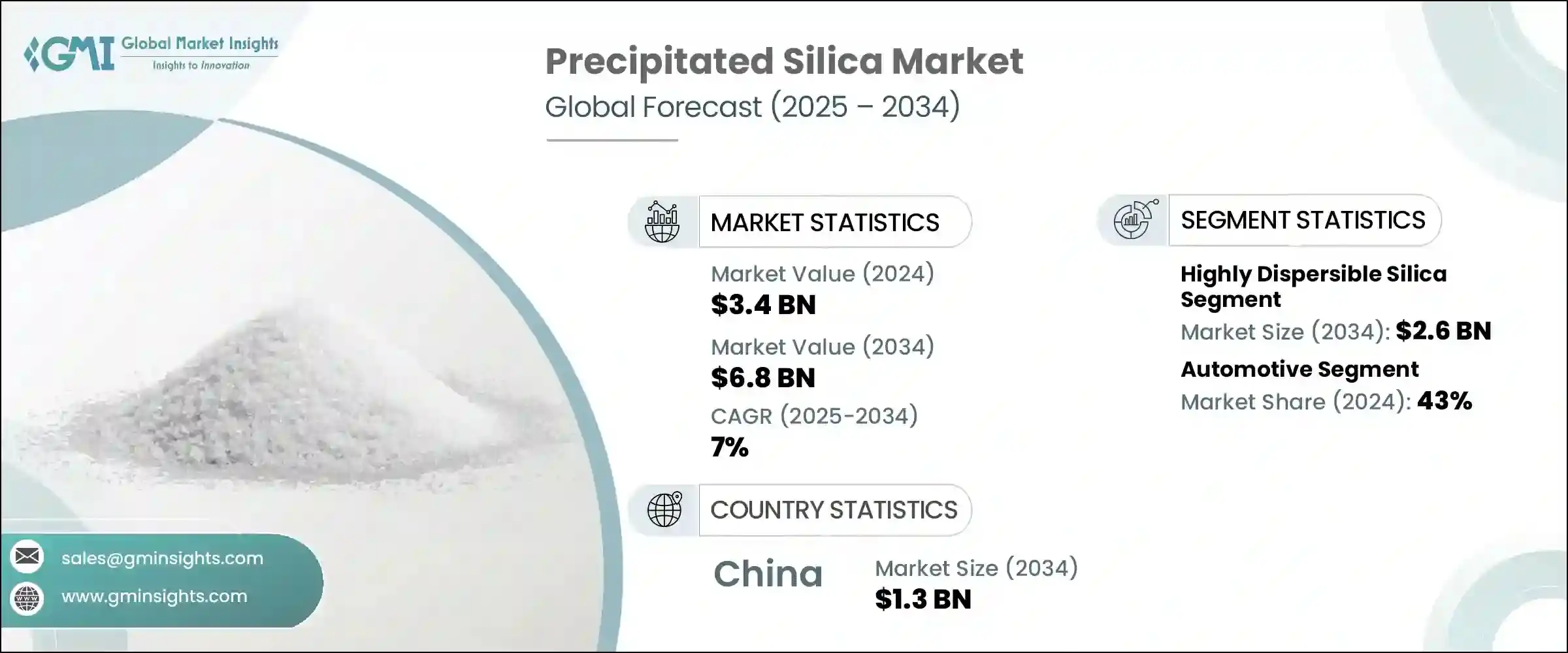

미국의 침전 실리카 시장은 2034년까지 연평균 복합 성장률(CAGR) 6.7%로 성장할 것입니다. 이러한 성장의 주요 요인은 타이어 및 고무 용도, 특히 전기자동차용 타이어의 판매 증가에 기인합니다. 또한 퍼스널케어, 의약품, 코팅제, 접착제 등으로 용도가 다양화되면서 시장 저변 확대에 기여하고 있습니다. 환경 문제에 대한 관심 증가와 친환경 소재에 대한 규제 강화로 인해 제조업체들은 지속가능한 실리카 생산 기술을 채택하고 있습니다. 주요 기업은 친환경 소재와 공정 혁신을 위해 생산 능력 확대와 연구개발에 많은 투자를 하고 있으며, 이는 미국 시장에서의 지속가능성과 장기적인 기술 혁신에 대한 업계의 명확한 초점을 강조하고 있습니다.

침전 실리카 업계의 주요 기업에는 PPG Industries, Evonik Industries, Oriental Silicas Corporation, W.R. Grace &Co., Solvay S.A. 등이 있습니다. 침전 실리카 시장에서 입지를 굳히기 위해 주요 기업은 다양한 산업의 요구에 맞는 특수하고 지속가능한 실리카 등급을 개발하고 제품 포트폴리오를 확장하는 데 주력하고 있습니다. R&D에 대한 집중적인 투자로 친환경 생산 방식과 재료 성능 향상에 대한 기술 혁신을 통해 친환경적이고 효율적인 솔루션에 대한 수요 증가에 부응하고 있습니다. 전략적 파트너십과 협력 관계는 새로운 지역적 시장에 접근하고 유통망을 확장하기 위해 형성되고 있습니다. 또한 각 회사는 기술 지원 서비스 및 맞춤형 솔루션을 통해 고객과의 관계를 강화하여 고객과의 관계를 더욱 공고히 하고 있습니다.

The Global Precipitated Silica Market was valued at USD 3.4 billion in 2024 and is estimated to grow at a CAGR of 7% to reach USD 6.8 billion by 2034. This market growth is driven by precipitated silica's unique physical and chemical properties, which make it a versatile ingredient across various industries. Over the past decade, its demand has steadily increased, particularly as a performance-enhancing additive in rubber, oral care products, and coatings. The ongoing trends of rapid urbanization, growing automotive production, and the increasing emphasis on environmentally friendly technologies continue to propel the market forward.

Precipitated silica's ability to improve product performance while aligning with sustainability goals positions it well for continued adoption. Emerging economies in the Asia Pacific region are fueling much of this growth, thanks to accelerated industrial development, expanding automotive sectors, and booming consumer goods markets. Countries such as China and India are not only large consumers but are also evolving as major production hubs, further solidifying the region's dominance in this sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.4 Billion |

| Forecast Value | $6.8 Billion |

| CAGR | 7% |

The tire and rubber industry remains the cornerstone of precipitated silica applications. Its vital role in enhancing traction, lowering rolling resistance, and boosting fuel efficiency has made it indispensable in modern tire formulations, especially for electric and high-performance vehicles. Beyond tires, precipitated silica's uses are broadening into pharmaceuticals, food processing, and personal care products, where it acts as an anti-caking agent, thickener, and detergent.

Highly dispersible silica (HDS) accounted for USD 1.3 billion in 2024 and is expected to reach USD 2.6 billion by 2034, growing at a CAGR of 7.1%. This variant is favored for its superior reinforcement capabilities and compatibility with tire rubber compounds. HDS significantly enhances rolling resistance, wet traction, and fuel economy, making it essential in the manufacture of green and high-performance tires, particularly for hybrid and electric vehicles. This aligns well with increasing global environmental regulations and original equipment manufacturers' (OEMs) demand for fuel-efficient products. The shift toward low-emission vehicles and eco-friendly tire solutions is boosting HDS adoption, reinforcing its position as a key material in future tire technologies.

In 2024, the automotive segment held a 43% share. This leadership is attributed to its widespread use in tire production, where silica improves tire grip, wear resistance, and fuel efficiency through reduced rolling resistance. With the global rise of energy-efficient, low-emission vehicles, manufacturers are increasingly incorporating silica-reinforced tires to meet regulatory standards and customer preferences. The surge in electric and hybrid vehicle production is driving demand for high-performance tires that depend heavily on precipitated silica to deliver enhanced traction and extended driving range. This trend is expected to continue as automotive manufacturers prioritize sustainable and high-quality tire materials.

U.S. Precipitated Silica Market will grow at a CAGR of 6.7% through 2034. This growth is primarily fueled by tire and rubber applications, especially with the rising sales of tires tailored for electric vehicles. Additionally, the diversification of applications into personal care, pharmaceuticals, coatings, and adhesives is helping broaden the market base. Increasing environmental concerns and regulations promoting eco-friendly materials are encouraging manufacturers to adopt sustainable silica production techniques. Leading companies are investing heavily in capacity expansion and research & development to innovate greener materials and processes, highlighting a clear industry focus on sustainability and long-term innovation in the U.S. market.

Key players in the Precipitated Silica Industry include PPG Industries, Evonik Industries, Oriental Silicas Corporation, W.R. Grace & Co., and Solvay S.A. To strengthen their foothold in the precipitated silica market, leading companies are focusing on expanding their product portfolios by developing specialized and sustainable silica grades tailored to diverse industry needs. Heavy investment in R&D is enabling innovation around eco-friendly production methods and enhanced material performance, which meets the growing demand for green and efficient solutions. Strategic partnerships and collaborations are being formed to access new geographic markets and broaden distribution networks. Companies are also enhancing customer engagement through technical support services and customized solutions, fostering stronger client relationships.