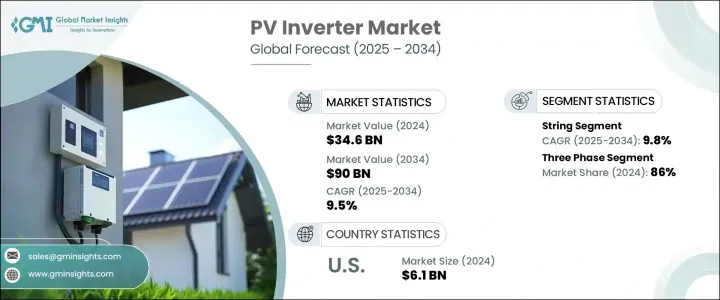

세계의 PV 인버터 시장은 2024년에는 346억 달러로 평가되었고, CAGR 9.5%로 성장할 전망이며, 2034년에는 900억 달러에 이를 것으로 예측됩니다.

세계의 에너지 정세는 신재생 전원을 중시하는 경향이 강해지는 등 현저한 변화를 이루고 있습니다. 이러한 변화는 효율적인 태양광 발전 시스템의 채택을 가속화시키고 있으며 인버터는 이제 최신 태양광 발전 설비의 중심적 존재가 되고 있습니다. 각국이 화석 연료에 대한 의존도를 줄이려 하고 있기 때문에 태양광 발전 인버터는 에너지 인프라로의 통합이 가속화되고 있습니다. 인버터는 직류 전력을 교류 전력으로 변환할 뿐만 아니라 시스템의 신뢰성과 에너지 수확량을 향상시키기 때문에 다양한 용도로 필수적인 기기가 되고 있습니다.

지속가능성에 대한 관심 증가는 유리한 에너지 정책과 관민 지원 투자와 함께 PV 인버터의 전개에 도움이 되는 환경을 만들어 내고 있습니다. 이산화탄소 배출량을 줄이고 에너지 소비를 최적화하기 위한 규제는 첨단 태양광 솔루션으로의 전환을 강화하고 있습니다. 게다가 규모의 경제와 제조 기술의 꾸준한 향상으로 태양광 발전 기술의 비용이 계속 줄어들어 태양광 발전 시스템의 채산성이 높아지고 있습니다. 이러한 합리적인 가격은 태양광 자원이 풍부하면서도 기존의 전력 인프라에 액세스하는 데 어려움을 겪었던 지역에 기회를 제공합니다. 분산형 에너지 발전의 확대는 계통 연계 및 오프 그리드 모두에서 원활하게 작동하는 인버터 수요를 더욱 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 346억 달러 |

| 예측 금액 | 900억 달러 |

| CAGR | 9.5% |

전력망의 근대화에 대한 노력도 첨단 인버터의 역할을 증대시키고 있습니다. 인텔리전트 에너지 네트워크의 진화에 따라 기본적인 전력 변환 이상의 기능을 가진 인버터에 대한 요구가 높아지고 있습니다. 원격 진단, 실시간 모니터링, 전압 조정, 주파수 지원 등의 기능은 차세대 디바이스의 표준이 되고 있습니다. 이러한 기능은 스마트 그리드의 틀에 통합을 가능하게 하고, 변동하는 신재생 전력 입력 중 전력회사가 그리드의 안정성을 유지하는 데 도움이 됩니다. 에너지 분야 전체에서 디지털화가 진행되는 가운데, 데이터 분석 및 AI 주도의 에너지 관리 기능을 갖춘 PV 인버터는, 효율적인 배전과 성능 최적화에 불가결한 존재가 되고 있습니다.

제품 유형별로, 스트링 인버터 수요가 높아지고 있으며, 2034년까지 CAGR 9.8%로 성장이 예상되고 있습니다. 그 인기의 이유는 확장성, 저렴한 가격, 유지보수의 용이성에 있습니다. 이러한 시스템은 모듈러 아키텍처가 신속한 고장 식별과 간소화된 시스템 업그레이드를 용이하게 하기 위해 주택과 상업 분야에서 널리 채택되고 있습니다. 게다가 스트링 인버터와 에너지 저장 유닛과의 호환성이 높아지고 있기 때문에 하이브리드 설비 전체에 걸쳐 그 매력이 퍼지고 있습니다. 효율적인 열 관리와 컴팩트한 설계는, 특히 스페이스에 제약이 있는 프로젝트에서의 시장 점유율 확대에 한층 더 공헌하고 있습니다.

시장 세분화는 단상과 3상으로 구분됩니다. 2024년에는 3상 인버터가 시장 전체의 86%를 차지했습니다. 이러한 우위성은 신흥 경제국의 급속한 공업화 및 도시 개발의 속도가 보다 대용량이고 범용성이 높은 에너지 시스템을 요구하고 있는 것에 기인하고 있습니다. 3상 인버터는 운전 효율이 높고, 전력 수요가 크고 안정된 상업용이나 공익 사업용의 대규모 전개에 적합합니다.

2024년 북미는 세계 PV 인버터 시장의 18.1%를 차지했습니다. 이 지역에서는 미국이 계속해서 주요 기여국으로, 시장 규모는 2022년 48억 달러에서 2024년 61억 달러로 증가했습니다. 이 나라에서는, 연방 및 주 레벨의 강력한 인센티브에 지탱되는 분산형 에너지 발전이 중시되고 있어 주택과 상업 시설 양쪽에서 옥상 태양광 발전의 성장을 조장하는 환경이 조성되고 있습니다. 동시에, 전국적인 송전망의 인프라 정비가 진행되어 스마트 인버터의 도입이 진행되고 있습니다. 특히 에너지의 회복력을 중시하는 주에서는 미터기 축전 솔루션이 대두되고 있어 PV 인버터의 도입은 더욱 확대될 것으로 보입니다.

각 제조업체는 연구 개발에 다액의 투자를 실시해, 주택용, 상업용, 공공시설용 등, 각 수요가의 요구에 맞춘 인버터의 폭넓은 라인업을 개발하고 있습니다. 하이브리드 모델로부터 산업용으로 설계된 대용량 인버터까지, 각사는 성능을 향상시켜, 에너지 수율을 높이고, 세계의 지속 가능성 목표에 따른 혁신을 전개하고 있습니다. 또, 디지털 인터페이스, 클라우드 접속, 예지 보전 기능 등, 인텔리전트 기술을 제품에 포함시키는 동향도 현저합니다. 이러한 진보는 사용자 경험을 향상시킬 뿐만 아니라 에너지 사용량과 시스템 건전성에 대한 보다 깊은 인사이트를 오퍼레이터에게 제공합니다.

세계적인 사업 전개를 강화하기 위해, 시장 진출 기업은 다양한 전략을 구사하고 있습니다. 이것은 태양광 발전 가능성이 높은 새로운 지역에의 진입, 서비스 제공을 강화하기 위한 제휴, 신기술을 활용하기 위한 합병 등을 포함합니다. 디지털 인프라 및 AI 기반 모니터링 툴의 연관성이 높아짐에 따라 이해관계자들은 기본적인 에너지 변환 이상의 가치를 부가하는 스마트 기능을 접목하게 됩니다. 세계 태양광 발전의 정세가 성숙함에 따라 이러한 포괄적인 전략은 소비자, 기업, 공익 사업자의 진화하는 에너지 수요에 대응하면서 기업이 경쟁력을 유지하는 데 도움이 될 것으로 생각됩니다.

The Global PV Inverter Market was valued at USD 34.6 billion in 2024 and is estimated to grow at a CAGR of 9.5% to reach USD 90 billion by 2034. The global energy landscape is undergoing a notable transformation, with increasing emphasis on renewable power sources. This shift is accelerating the adoption of efficient photovoltaic systems, and inverters are now central to modern solar installations. As countries seek to reduce their dependence on fossil fuels, PV inverters are being integrated into energy infrastructure at a faster pace. These devices not only convert DC to AC power but also enhance system reliability and energy yield, making them indispensable across various applications.

The growing focus on sustainability, combined with favorable energy policies and supportive investment from the public and private sectors, is creating a conducive environment for PV inverter deployment. Regulations aimed at cutting carbon emissions and optimizing energy consumption are reinforcing the shift toward advanced solar solutions. Moreover, ongoing declines in solar technology costs-driven by economies of scale and steady improvements in manufacturing-are making PV systems more financially viable. This affordability is opening up opportunities in regions that are rich in solar resources but have historically faced challenges in accessing conventional power infrastructure. The expansion of distributed energy generation further supports the demand for inverters capable of operating seamlessly across grid-connected and off-grid setups.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $34.6 Billion |

| Forecast Value | $90 Billion |

| CAGR | 9.5% |

Modernization efforts within power grids are also amplifying the role of advanced inverters. With the evolution of intelligent energy networks, there is an increased need for inverters that can perform beyond basic power conversion. Features such as remote diagnostics, real-time monitoring, voltage regulation, and frequency support are becoming standard in next-generation devices. These functionalities enable better integration into smart grid frameworks and help utilities maintain grid stability amid fluctuating renewable power inputs. As digitalization gains traction across the energy sector, PV inverters equipped with data analytics and AI-driven energy management capabilities are proving vital for efficient power distribution and performance optimization.

Among the different product types, string inverters are experiencing heightened demand, with expectations of growing at a CAGR of 9.8% through 2034. Their popularity stems from their scalability, affordability, and ease of maintenance. These systems are widely adopted in both residential and commercial sectors, as their modular architecture facilitates quick fault identification and simplified system upgrades. Additionally, the increasing compatibility of string inverters with energy storage units has broadened their appeal across hybrid installations. Their efficient thermal management and compact designs further contribute to their rising market share, especially in space-constrained projects.

The PV inverter market is segmented by phase into single-phase and three-phase systems. In 2024, three-phase inverters accounted for 86% of the overall market. This dominance can be attributed to the rapid pace of industrialization and urban development in emerging economies, which demand higher-capacity and more versatile energy systems. Three-phase inverters offer operational efficiency and are better suited for large-scale deployments in commercial and utility-scale applications, where power requirements are substantial and consistent.

North America, as of 2024, represented 18.1% of the global PV inverter market. Within this region, the United States continues to be a key contributor, with market values rising from USD 4.8 billion in 2022 to USD 6.1 billion in 2024. The country's emphasis on decentralized energy generation, supported by robust federal and state-level incentives, has fostered an environment conducive to rooftop solar growth in both residential and commercial settings. At the same time, ongoing upgrades to the national grid infrastructure are driving the integration of smart inverters. With the rise of behind-the-meter storage solutions, particularly in states focused on energy resilience, the deployment of PV inverters is set to grow further.

Manufacturers are investing heavily in R&D to develop a broad portfolio of inverters tailored to specific customer needs across residential, commercial, and utility-scale sectors. From hybrid models to high-capacity inverters designed for industrial use, companies are rolling out innovations that improve performance, enhance energy yield, and align with global sustainability goals. There is also a noticeable trend toward embedding intelligent technologies into products, including digital interfaces, cloud connectivity, and predictive maintenance capabilities. These advancements not only improve user experience but also offer operators deeper insights into energy usage and system health.

To strengthen their global footprint, market participants are leveraging a combination of strategies. These include entering new geographic regions with high solar potential, forming alliances to enhance service offerings, and pursuing mergers to tap into emerging technologies. The increasing relevance of digital infrastructure and AI-based monitoring tools is leading stakeholders to incorporate smart features that add value beyond basic energy conversion. As the global solar landscape matures, these comprehensive strategies will help companies remain competitive while addressing the evolving energy demands of consumers, businesses, and utilities.