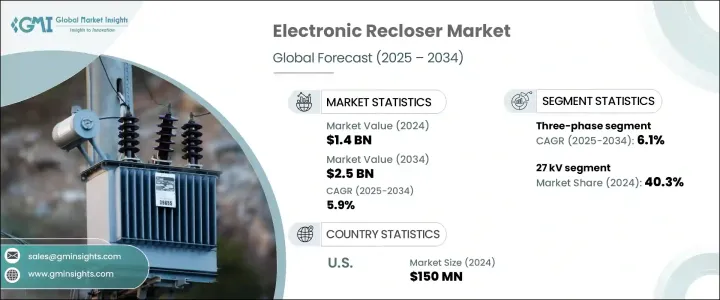

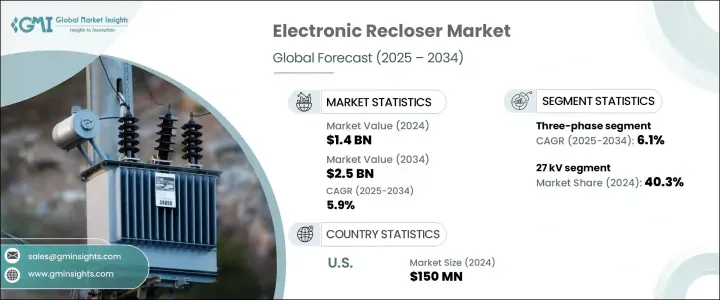

세계의 전자 리클로저 시장 규모는 2024년에 14억 달러로 평가되었고, CAGR 5.9%로 성장할 전망이며, 2034년에는 25억 달러에 이를 것으로 예측됩니다.

이러한 성장의 배경은 노후화된 송전망 인프라의 현대화, 배전 효율의 향상, 재생에너지원 통합 등의 요구가 있습니다. 전자 리클로져는 자동 고장 검출 및 복구를 가능하게 함으로써 다운타임을 줄이고 시스템의 신뢰성을 향상시키는 스마트 그리드에서 중요한 역할을 하고 있습니다. 기술의 진보로 센서, 통신 기능, 사물인터넷(IoT) 플랫폼과의 통합이 강화된 리클로져가 개발되어 채택이 더욱 가속화되고 있습니다.

게다가 신뢰성이 높고 지능적인 그리드 시스템에 대한 수요가 높아지고, 유리한 정부 인센티브, 전기 인프라 근대화에 대한 대규모 투자 등이 전자 리클로저 시장의 성장을 계속 추진하고 있습니다. 유틸리티 기업 및 그리드 운영자가 자동화 및 보다 스마트한 에너지 관리로 전환하는 가운데, 전자 리클로져는 신속한 고장 검출을 지원하고 전력 중단을 최소화하며 시스템 전체의 회복력을 높이기 위해 통합되고 있습니다. 분산형 에너지 자원의 도입과 신재생 에너지의 통합이 진행되어 안정성 및 서비스의 계속성을 유지하기 위해서 실시간 그리드 응답성이 불가결하게 되는 가운데, 그 역할은 더욱 중요해지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 14억 달러 |

| 예측 금액 | 25억 달러 |

| CAGR | 5.9% |

3상 부문은 고부하의 미션 크리티컬 배전 네트워크 설치를 반영하며 2034년까지 연평균 복합 성장률(CAGR) 6.1%로 성장할 것으로 예측됩니다. 이 리클로저는 전력의 3상 전반에 걸쳐 종합적인 보호를 제공하기 때문에 대규모 상업시설 및 산업 시설에서 헤비 듀티 용도에 적합합니다. 고장을 분리하고 수동 개입 없이 자동으로 전력을 복구시키는 그 능력은 다운타임을 최소화해야 하는 대용량 송전망에 필수적입니다.

2024년에는 15kV 부문의 시장 평가 금액이 5억 3,550만 달러에 이르렀습니다. 이 전압 클래스는 중전압 시스템에 널리 도입되어 있으며, 도시 지역과 농촌 지역 양쪽 배전망의 표준 사양입니다. 이 전압 등급의 인기는 주택지, 경공업단지, 전력회사의 변전소에서 비용 효율 및 신뢰성 높은 고장 관리를 실현하고 전력회사가 다양한 운전조건 하에서 중단없는 서비스를 유지할 수 있는 것에 기인하고 있습니다.

미국의 전자 리클로저 2024년 시장 규모는 1억 5,000만 달러로 지난 몇 년간의 일관된 성장을 반영하고 있습니다. 이러한 증가 경향은 노후화된 전력 인프라의 갱신과 고도의 그리드 기술 도입에 국가가 주력하고 있는 것이 큰 요인이 되고 있습니다. 노후화된 시스템 업그레이드는 현재의 에너지 수요에 대응하고 송전망의 안정성을 확보하며 미래의 지속가능성 목표를 달성하기 위해 필수적입니다. 게다가 규제기관이 정하는 엄격한 성능 및 신뢰성 기준에 준거하는 것으로, 고도의 진단, 원격 조작 기능, 심리스한 그리드 통합을 제공하는 차세대 리클로져의 채용이 증가하고 있습니다.

세계 전자 리클로저 시장에서 사업을 전개하는 주요 기업으로는 ABB, Arteche, Eaton, Ensto, Entec Electric & Electronic, G&W Electric, Hubbell, Hughes Power System, NOJA Power Switchgear Pty Ltd, Rockwell, S&C Electric Company, Schneider Electric, Siemens, Tavrida Electric 등이 있습니다. 이러한 기업은 경쟁 구도에서의 지위를 강화하기 위해 제품 혁신, 전략적 파트너십, 시장 존재를 주도하고 있습니다. 시장에서의 위상을 강화하기 위해 전자 리클로자 업계의 기업은 몇 가지 중요한 전략을 채택하고 있습니다. 연구 개발에 투자하고, 제품 제공의 혁신과 개선을 도모해, 최신의 배전 시스템의 진화하는 요구에 확실히 응하고 있습니다.

The Global Electronic Recloser Market was valued at USD 1.4 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 2.5 billion by 2034. This growth is driven by the need to modernize aging grid infrastructure, enhance power distribution efficiency, and integrate renewable energy sources. Electronic reclosers play a crucial role in smart grids by enabling automated fault detection and restoration, thereby reducing downtime and improving system reliability. Technological advancements have led to the development of reclosers with enhanced sensors, communication capabilities, and integration with Internet of Things (IoT) platforms, further boosting their adoption.

Additionally, the rising demand for dependable and intelligent grid systems, alongside favorable government incentives and large-scale investments in electrical infrastructure modernization, continues to fuel growth in the electronic recloser market. As utilities and grid operators shift toward automation and smarter energy management, electronic reclosers are being integrated to support rapid fault detection, minimize power interruptions, and enhance overall system resilience. Their role becomes even more critical with the growing deployment of distributed energy resources and renewable energy integration, where real-time grid responsiveness is essential for maintaining stability and service continuity.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.5 Billion |

| CAGR | 5.9% |

The three-phase segment is anticipated to grow at a CAGR of 6.1% through 2034, reflecting installations in high-load and mission-critical distribution networks. These reclosers provide comprehensive protection across all three phases of power, making them well-suited for heavy-duty applications in large-scale commercial and industrial facilities. Their ability to isolate faults and automatically restore power without manual intervention makes them indispensable in high-capacity grids where downtime must be minimized.

In 2024, the 15kV segment reached a market valuation of USD 535.5 million. This voltage class is widely deployed in medium-voltage systems and serves as a standard specification for both urban and rural distribution networks. Its popularity stems from its ability to deliver cost-effective and reliable fault management in residential zones, light industrial parks, and utility substations, enabling utilities to maintain uninterrupted service in diverse operating conditions.

United States Electronic Recloser Market was valued at USD 150 million in 2024, reflecting consistent growth over the previous years. This upward trend is largely driven by the nation's focus on replacing aging power infrastructure and deploying advanced grid technologies. Upgrades to outdated systems are essential for addressing current energy demands, ensuring grid stability, and achieving future sustainability goals. Additionally, compliance with strict performance and reliability standards set by regulatory bodies has increased the adoption of next-generation reclosers, which offer advanced diagnostics, remote operation capabilities, and seamless grid integration.

Key players operating in the Global Electronic Recloser Market include ABB, Arteche, Eaton, Ensto, Entec Electric & Electronic, G&W Electric, Hubbell, Hughes Power System, NOJA Power Switchgear Pty Ltd, Rockwell, S&C Electric Company, Schneider Electric, Shinsung Industrial Electric, Siemens, and Tavrida Electric. These companies are focusing on product innovation, strategic partnerships, and expanding their market presence to strengthen their positions in the competitive landscape. To strengthen their market presence, companies in the electronic recloser industry are adopting several key strategies. They are investing in research and development to innovate and improve product offerings, ensuring they meet the evolving needs of modern power distribution systems.