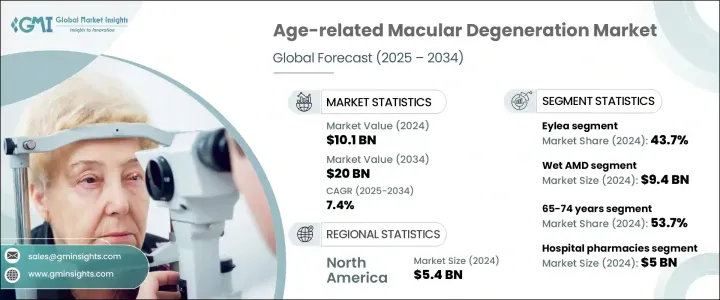

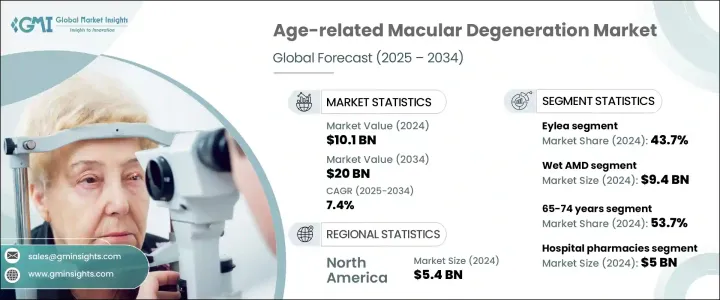

세계의 노인황반변성(AMD) 시장 규모는 2024년에 101억 달러를 달성하였고 CAGR 7.4%로 성장하여 2034년에는 200억 달러에 이를 것으로 추정됩니다.

시장 성장의 원동력은 AMD의 유병률 상승, 세계 인구의 고령화, 인지도의 향상과 조기 진단, 치료 옵션의 지속적인 혁신입니다. AMD는 주로 50세 이상의 사람들이 앓고 있는 진행성 안질환이며, 돌이킬 수 없는 중심 시력의 저하를 초래하고, 독서, 운전, 얼굴 인식 등의 일상생활을 현저하게 손상시키며 결국 생활의 질 전체에 영향을 미칩니다.

질병이 진행되면 망막의 황반부(샤프한 중심 시력을 잡는 부분)가 침범되어 시야가 흐리거나 어두워지거나 합니다. AMD의 부담 증가는 세계 고령화의 동향과 밀접하게 관련되어 있으며, 그 유병률은 65세 이상의 인구에서 급격히 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 101억 달러 |

| 예측 금액 | 200억 달러 |

| CAGR | 7.4% |

질병 유형별로는 습성 AMD가 2024년에 94억 달러 시장 규모를 차지하였고, 그 원동력이 된 것은 질병의 진행을 멈추고, 망막액 저류를 최소한으로 억제하여, 시기능을 유지하는 효과가 입증된 항VEGF 요법의 광범위한 채용이었습니다. 한편, 건성 AMD는 지금까지 승인된 약리학적 개입이 없었지만, 현재 임상적으로 다시 주목받고 있습니다. 최초의 FDA 승인 치료제인 Syfovre의 출시는 보체 경로 억제제 및 유전자 치료제의 유망한 파이프라인과 함께 이 분야의 치료에서 변화의 징후를 시사합니다.

Eylea, Lucentis, Vabysmo 등의 항VEGF 요법은 AMD 치료의 핵심이 되고 있습니다. Eylea HD는 투여 스케줄을 연장하여 환자의 순응도를 향상시키고 치료 부담을 경감함으로써 많은 인기를 모으고 있습니다. Vabysmo와 같은 신규 참가 기업은 이중 경로 저해(VEGF-A+Ang-2) 기술로 급속하게 시장 점유율을 확대하면서 혈관의 불안정성에 대처하여 임상 결과를 향상시키고 있습니다.

북미 노인황반변성 시장의 2025-2034년간 CAGR은 7%로 예상되며 견고한 헬스케어 인프라, 혁신적인 치료법의 조기 도입, 지지적인 규제 프레임워크가 시장을 견인하고 있습니다. 건식 AMD에 대한 광바이오모듈레이션 등 새로운 비침습적 치료법이 최근 FDA의 승인을 받은 사실은 환자의 기호에 맞추어 장기적인 순응도를 향상시키는 보다 부담이 적은 치료법으로의 지역적인 전환을 뒷받침하는 것입니다.

노인황반변성 시장 내 지위를 강화하기 위해 Xbrane Biopharma AB, Pfizer Inc., Formycon AG, Celltrion, Inc., Novartis AG, Amgen Inc., Sandoz Group AG, Apellis Pharmaceuticals, Inc., STADA Arzneimittel AG, F. Hoffmann-La Roche Ltd., Biocon Biologics Limited, Regeneron Pharmaceuticals Inc., Bayer AG, Biogen, Inc.와 같은 기업은 R&D 투자, 바이오시밀러 개발, 장시간 작용 제형 등의 전략적 이니셔티브를 채택하고 있습니다. Regeneron의 Eylea HD 출시와 Roche에 의한 Vabysmo의 도입은 혁신 주도의 경쟁을 실증하고 있습니다. 시장 리더는 포트폴리오를 다각화하기 위해 유전자 치료제, 이중 경로 억제제, 보체 표적 약물에 주력하고 있습니다.

The Global Age-related Macular Degeneration Market was valued at USD 10.1 billion in 2024 and is estimated to grow at a CAGR of 7.4% to reach USD 20 billion by 2034. The market growth is driven by a rising prevalence of AMD, an aging global population, increased awareness and early diagnosis, and ongoing innovations in treatment options. AMD is a progressive eye condition affecting individuals aged 50 and above, leading to central vision loss and significantly impacting quality of life. AMD is a progressive eye condition that primarily affects individuals aged 50 and above, leading to irreversible central vision loss and significantly impairing daily activities such as reading, driving, and recognizing faces, ultimately impacting the overall quality of life.

As the disease advances, it compromises the macula-the part of the retina responsible for sharp, central vision-resulting in blurred or dark spots in the visual field that cannot be corrected with glasses or contact lenses. This loss of independence often contributes to psychological effects such as anxiety, depression, and social isolation, especially among older adults. The growing burden of AMD is closely tied to the global aging trend, with its prevalence sharply increasing in populations over 65. The disease is also associated with other risk factors such as smoking, hypertension, obesity, genetic predisposition, and poor dietary habits-factors that are becoming more prevalent globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.1 Billion |

| Forecast Value | $20 Billion |

| CAGR | 7.4% |

By disease type, wet AMD dominated the market with USD 9.4 billion in 2024, driven by the widespread adoption of anti-VEGF therapies, which have proven effective in halting disease progression, minimizing retinal fluid accumulation, and preserving visual function. The success of agents like Eylea, Lucentis, and Beovu has positioned wet AMD as the most actively treated form of the disease. Meanwhile, dry AMD, historically lacking approved pharmacologic interventions, is now seeing renewed clinical focus. The launch of Syfovre, the first FDA-approved treatment for geographic atrophy (a severe form of dry AMD), along with a promising pipeline of complement pathway inhibitors and gene therapies, signals a transformative shift in managing this segment.

Anti-VEGF therapies such as Eylea, Lucentis, and Vabysmo have become the cornerstone of AMD treatment. Among these, the Eylea segment held 43.7% share owing to its efficacy in extending injection intervals and maintaining visual acuity. The drug's updated formulation, Eylea HD, is gaining further traction by offering extended dosing schedules that improve patient adherence and reduce treatment burden. New entrants like Vabysmo are rapidly gaining market share through dual-pathway inhibition (VEGF-A + Ang-2), addressing vascular instability and offering enhanced clinical outcomes.

North America Age-related Macular Degeneration Market will grow at a CAGR of 7% during 2025-2034, driven by robust healthcare infrastructure, early adoption of innovative therapies, and supportive regulatory frameworks. High diagnosis rates are further supported by widespread access to advanced imaging technologies such as OCT and an increasing focus on preventative eye care. Recent FDA approvals of novel, non-invasive therapies such as photobiomodulation for dry AMD underscore a regional shift toward less burdensome treatment modalities, aligning with patient preferences and improving long-term adherence.

To strengthen their position in the Age-related Macular Degeneration Market, companies like Xbrane Biopharma AB, Pfizer Inc., Formycon AG, Celltrion, Inc., Novartis AG, Amgen Inc., Sandoz Group AG, Apellis Pharmaceuticals, Inc., STADA Arzneimittel AG, F. Hoffmann-La Roche Ltd., Biocon Biologics Limited, Regeneron Pharmaceuticals Inc., Bayer AG, Biogen, Inc. are adopting strategic initiatives including R&D investments, biosimilar development, and long-acting formulations. Regeneron's launch of Eylea HD and Roche's introduction of Vabysmo demonstrate innovation-driven competition. Companies are also expanding through partnerships with CROs for clinical trials and leveraging digital tools for real-world data collection. Global market leaders focus on gene therapies, dual-pathway inhibitors, and complement-targeting drugs to diversify their portfolios. Additionally, pricing strategies, strategic licensing, and regulatory collaborations enable faster market access.