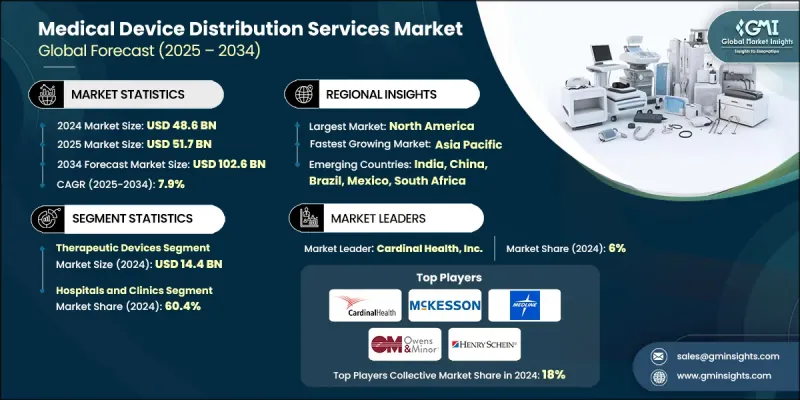

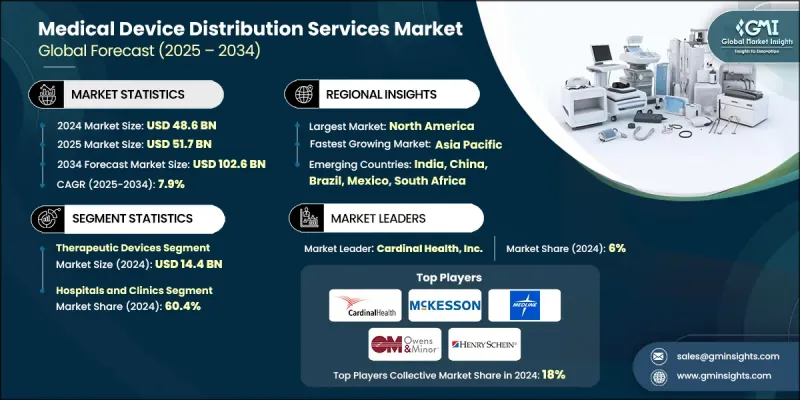

세계의 의료기기 유통 서비스 시장은 2024년에 486억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 7.9%로 성장하여 1,026억 달러에 이를 것으로 예측됩니다.

이러한 확대는 만성질환의 유병률 증가, 재택의료 및 원격 모니터링 솔루션의 급속한 보급, 디지털 공급망 역량에 대한 대규모 투자에 의해 촉진되고 있습니다. 유통업체는 의료시스템의 전략적 파트너로서 물류뿐만 아니라 설치, 교정, 교육, 콜드체인 관리, UDI 추적성 등 부가가치 서비스를 제공합니다. 이는 상품 운송에서 통합 임상 공급 솔루션으로의 전환을 가속화하고 있습니다. 동시에 병원의 대량 조달 및 그룹 구매 조직(GPO)의 추세에 따라 재고 부족을 줄이고 리드 타임을 단축하며 여러 관할 구역의 규제 준수를 보장하는 고급 유통 서비스에 대한 수요가 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 개시 연도 시장 규모 | 486억 달러 |

| 예측 금액 | 1,026억 달러 |

| CAGR | 7.9% |

제품 유형별로는 치료 장비 부문이 2024년 144억 달러로 시장을 주도할 것으로 예상되며, 이는 주입 펌프, 호흡기, 심혈관 스텐트, 인공 임플란트, 투석 시스템, 기타 치료 필수 기술에 대한 높은 수요를 반영합니다. 치료용 기기는 일반적으로 전문적인 취급, 콜드체인 또는 환경 조건에 민감한 물류, 애프터 서비스(설치, 유지 보수, 직원 교육)가 필요하기 때문에 유통업체의 마진을 확대하고 병원 및 클리닉과의 장기적인 파트너십을 강화합니다.

최종 용도별로는 병원 및 클리닉 부문이 2024년 60.4%의 점유율을 차지했습니다. 이는 광범위한 의료기기에 대한 수요, 중앙 집중식 조달 프로세스, 응급 및 수술 치료를 위한 높은 수준의 병원 내 재고 유지 필요성에 기인합니다. 병원이 물류, 설치, 애프터 서비스를 결합한 종합적인 서비스 제공을 선호하는 추세는 추적성, 신속한 수리 대응, 컴플라이언스 보고를 보장할 수 있는 유통 파트너의 전략적 중요성을 높이고 있습니다.

북미 의료기기 유통 서비스 시장은 2024년 39.2%의 점유율을 차지했습니다. 이는 이 지역의 성숙한 의료 인프라, 높은 시술 건수, 디지털 물류 기술(IoT, AI, 추적성을 위한 블록체인)의 조기 도입을 반영합니다. 대규모 병원 네트워크, 중앙집중식 GPO 계약, 강력한 재택치료 상환 제도를 포함한 미국 시장 시장 역학은 유통업체의 수익률 향상과 첨단 콜드체인 및 자동 보충 시스템에 대한 투자를 뒷받침하고 있습니다. 또한, 공급망 탄력성 강화, 유통 센터의 기술 현대화, UDI(의료기기 식별자)와 같은 규제 프레임워크(추적 가능하고 품질이 보장된 유통 모델 촉진)에 대한 공공 및 민간 자금의 대폭적인 투입으로 북미의 선도적 입지는 더욱 강화되고 있습니다.

The Global Medical Device Distribution Services Market was valued at USD 48.6 billion in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 102.6 billion by 2034.

The expansion is driven by rising chronic disease prevalence, rapid adoption of home-healthcare and remote monitoring solutions, and significant investments in digital supply-chain capabilities. Distributors are increasingly positioned as strategic partners to healthcare systems, providing not just logistics but value-added services such as installation, calibration, training, cold-chain management, and UDI traceability, which is accelerating the shift from commodity shipping to integrated clinical supply solutions. Simultaneously, hospitals' large procurement volumes and Group Purchasing Organization (GPO) dynamics are increasing demand for sophisticated distribution services that reduce stockouts, shorten lead times, and ensure regulatory compliance across multiple jurisdictions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $48.6 Billion |

| Forecast Value | $102.6 Billion |

| CAGR | 7.9% |

By product type, the therapeutic devices segment led the market in 2024 with USD 14.4 billion, reflecting strong demand for infusion pumps, respiratory devices, cardiovascular stents, prosthetic implants, dialysis systems, and other treatment-critical technologies. Therapeutic devices typically require specialized handling, cold-chain or condition-sensitive logistics, and after-sales support (installation, servicing, staff training), which amplifies distributor margins and cements long-term partnerships with hospitals and clinics.

On an end-use basis, the hospitals and clinics segment held 60.4% share in 2024, owing to their broad device requirements, centralized procurement processes, and need to maintain high in-house inventories for emergency and surgical care. Hospitals' preference for bundled service offerings combining logistics, installation, and post-sale support heightens the strategic importance of distribution partners who can guarantee traceability, rapid response repair, and compliance reporting.

North America Medical Device Distribution Services Market held 39.2% share in 2024, reflecting the region's mature healthcare infrastructure, high procedural volumes, and early adoption of digital logistics technologies (IoT, AI, blockchain for traceability). The U.S. market dynamics, including large hospital networks, centralized GPO contracting, and strong home-healthcare reimbursement systems, support higher distributor margins and investment in advanced cold-chain and automated replenishment systems. North America's leadership is further reinforced by substantial private and public funding for supply-chain resilience, technology modernization in distribution centers, and regulatory frameworks such as UDI that incentivize traceable, quality-assured distribution models.

Key players shaping the Global Medical Device Distribution Services Market include Cardinal Health, Inc.; McKesson Corporation; Medline Inc.; Owens & Minor, Inc.; Henry Schein, Inc.; Patterson Companies, Inc.; Bunzl plc; Avantor, Inc.; Alfresa Holdings Corporation; CAN-med Healthcare; KEBOMED Europe AG; Meditek Systems Pvt. Ltd.; Soquelec Ltd.; Southmedic Inc.; and The Stevens Company Limited. These companies are competing on breadth of coverage, cold-chain and compliance capabilities, digital ordering platforms, and value-added clinical services. Market leaders are investing in smart warehouses, temperature-validated storage, last-mile home care delivery capabilities, and partnerships with OEMs and telehealth providers to capture higher margin service revenues and lock in long-term procurement agreements. Companies in the medical device distribution services market are strengthening footprints through vertical integration, digital platform investments, and strategic partnerships with hospitals, GPOs, and device OEMs.