세계의 자동차용 회생 쇼크 업소버 시장은 2024년 13억 달러에 달했고, CAGR 8.2%로 성장해 2034년까지 28억 달러에 이를 것으로 예측되고 있습니다.

에너지 효율이 높은 차량 시스템과 연료 성능의 향상에 대한 수요 증가가 회생 쇼크 업소버의 채용을 뒷받침하고 있습니다. 차량 서스펜션 기술의 진보는 상용차와 승용차의 양쪽 모두에 적용 범위를 넓혀, 회생 솔루션을 보다 현실적인 것으로 만들고 있습니다.

자동차 부문은 에너지 회수 솔루션으로 전환하고 있으며, 회생 쇼크 업소버는 운전 효율을 달성하기 위한 중요한 구성 요소로 부상하고 있습니다. 배출가스와 연비 향상을 요구하는 세계의 규제 강화로 OEM은 컴플라이언스 전략의 일환으로 에너지 변환 서스펜션 기술의 채용을 강요받고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 13억 달러 |

| 예측 금액 | 28억 달러 |

| CAGR | 8.2% |

2024년에는 승용차가 66.5%의 점유율로 시장을 선도했고 2034년까지 연평균 복합 성장률(CAGR) 8.5%를 보일 것으로 예측됩니다. 승용차의 생산과 판매가 세계적으로 확산되고 있는 것이 이 동향의 큰 힘이 되고 있습니다. 소비자는 점점 더 부드러운 승차감, 우수한 핸들링, 우수한 연비 효율을 제공하는 자동차를 선호하고 있습니다. 그 결과, 회생 쇼크 업소버는 보통 승용차에도 고급 승용차에도 탑재되게 되어 있습니다. 자동차 제조업체가 항속거리의 향상과 환경 부하의 저감에 노력하고 있기 때문에 전기자동차나 하이브리드 승용차의 급속한 보급이 이 경향을 한층 더 가속시키고 있습니다. 지속가능성 목표를 달성하려는 상대방 상표 제품 제조업체의 노력은 전자기 댐퍼와 기계식 댐퍼의 통합을 촉진합니다. 지속적인 R&D 비용과 지원 정부의 이니셔티브는 기술 혁신을 가속화하고 이 부문에서 회생 서스펜션 시스템의 채택을 강화하고 있습니다.

전자식 회생 쇼크 업소버는 2024년 44%로 최대 시장 점유율을 차지했고, 2025-2034년에는 CAGR 8.3%를 보일 것으로 예측됩니다. 이 시스템은 전자기 유도를 이용하여 노면의 유도 운동으로부터 에너지를 이용하여 기계 저항을 최소화하면서 발전합니다. 고효율, 응답성이 뛰어난 설계로 기존의 유압식 및 기계식 시스템보다 우수합니다. OEM 각사는 프리미엄 모델이나 전동 모델에 전자 서스펜션을 채용하여 에너지 절약 효과를 얻으면서 성능을 극대화하고 있습니다. 세계의 선호도가 지능적이고 효율적인 모빌리티 솔루션으로 옮겨가면서 이 부문에 대한 관심이 높아지고 급속히 확대되고 있습니다.

중국의 자동차용 회생 쇼크 업소버 2024년 시장 규모는 3억 6,270만 달러로, 점유율은 69%였습니다. 전기자동차의 급속한 보급은 현지에서의 서스펜션 제조의 진보와 함께, 중국을 중요한 성장 허브에 자리잡고 있는 중국의 견고한 자동차 제조 에코시스템은 국내 기술 혁신과 연구개발에 많은 투자와 함께 회생 서스펜션 시스템의 채용을 뒷받침하고 있습니다.

자동차용 회생 쇼크 업소버 세계 시장을 형성하는 주요 기업으로는 ZF Friedrichshafen, SACHS, Trelleborg, Hitachi Astemo, KYB, Mando, Fox Factory, Endurance Technologies, ThyssenKrupp Bilstein, BWI Group 등이 있습니다. 자동차용 회생 쇼크 업소버 시장에서의 지위를 굳히기 위해, 주요 기업은 기술 혁신, 지속가능성, 전략적 제휴에 주력하고 있습니다. 을 강화하기 위해 R&D 투자를 강화하고 있습니다. 제조업체는 OEM과 제휴하여 이러한 기술을 차세대 전기자동차와 하이브리드 자동차에 통합하려고 합니다.

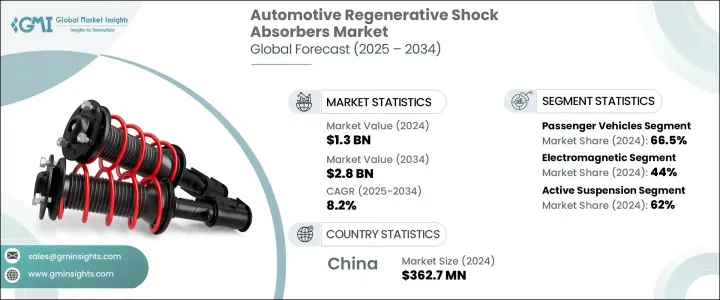

The Global Automotive Regenerative Shock Absorbers Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 8.2% to reach USD 2.8 billion by 2034. Increasing demand for energy-efficient vehicle systems and enhanced fuel performance continues to drive the adoption of regenerative shock absorbers. These systems convert kinetic energy, produced by suspension movement and road vibrations, into usable electricity, contributing to overall vehicle efficiency. As electrification trends accelerate and environmental regulations tighten worldwide, automakers are integrating these systems more broadly into electric, hybrid, and conventional vehicles. Advances in vehicle suspension technologies are expanding the application scope across both commercial and passenger vehicles, making regenerative solutions more viable. Manufacturers are turning to energy-harvesting technologies to support fuel economy and meet emissions standards while improving ride quality and system responsiveness.

The automotive sector is shifting toward energy recovery solutions, and regenerative shock absorbers are emerging as key components in achieving operational efficiency. These systems repurpose road energy into electrical output, lowering traditional energy dependency. Stricter global mandates for lower emissions and improved fuel economy are pushing OEMs to embrace energy-converting suspension technologies as part of their compliance strategies. In this evolving landscape, regenerative damping systems are gaining prominence across various vehicle classes and use cases.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.8 Billion |

| CAGR | 8.2% |

In 2024, passenger vehicles led the market with a 66.5% share and are forecast to grow at 8.5% CAGR through 2034. The widespread production and sales of passenger cars worldwide are a major force behind this trend. Consumers are increasingly favoring vehicles that offer smoother rides, superior handling, and better fuel efficiency. As a result, regenerative shock absorbers are being incorporated into both standard and high-end passenger vehicles. The rapid growth of electric and hybrid passenger models is further accelerating this trend, as automakers strive to enhance range and reduce environmental impact. Efforts by original equipment manufacturers to meet sustainability goals are encouraging the integration of electromagnetic and mechanical dampers. Continued R&D spending and supportive government initiatives are accelerating innovation and bolstering the adoption of regenerative suspension systems in this segment.

Electromagnetic regenerative shock absorbers held the largest market share in 2024, accounting for 44%, and are projected to grow at a CAGR of 8.3% during 2025-2034. These systems harness energy from road-induced motion using electromagnetic induction, generating electricity while minimizing mechanical drag. Their high efficiency and responsive design give them an edge over traditional hydraulic or mechanical systems. OEMs are adopting electromagnetic suspension for premium and electric models to maximize performance while achieving energy-saving benefits. As global preferences shift toward intelligent and efficient mobility solutions, this segment is seeing heightened interest and rapid expansion.

China Automotive Regenerative Shock Absorbers Market generated USD 362.7 million in 2024 and held a 69% share. The rapid uptake of electric vehicles, coupled with advancements in local suspension manufacturing, has positioned China as a key growth hub. Heavier EV battery designs are driving the need for advanced shock absorption solutions that improve handling and ride quality. China's robust automotive manufacturing ecosystem, along with substantial investments in domestic innovation and R&D, is bolstering the adoption of regenerative suspension systems. Government backing for electric mobility and industry transformation is further encouraging the development of lightweight and adaptive technologies. The country's strategic focus on performance and fuel economy is making it a significant contributor to global market expansion.

Key players shaping the Global Automotive Regenerative Shock Absorbers Market include ZF Friedrichshafen, SACHS, Trelleborg, Hitachi Astemo, KYB, Mando, Fox Factory, Endurance Technologies, ThyssenKrupp Bilstein, and BWI Group. To solidify their position in the automotive regenerative shock absorbers market, leading companies are focusing on innovation, sustainability, and strategic collaborations. Many are ramping up R&D investments to enhance electromagnetic and mechanical energy recovery systems that align with the shift to electrified mobility. Manufacturers are partnering with OEMs to integrate these technologies into next-generation electric and hybrid vehicles. Another major strategy includes geographic expansion into emerging EV markets through localized production units.