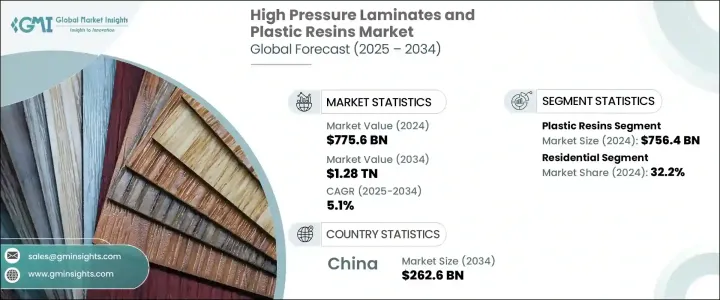

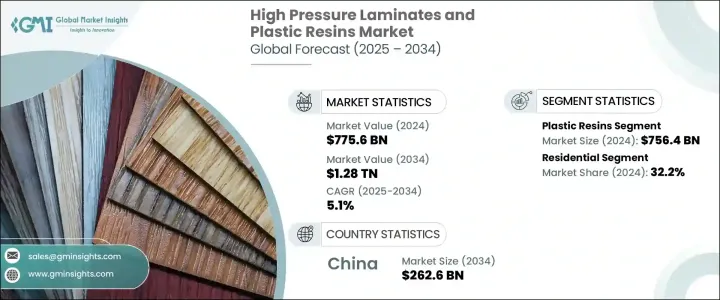

고압 라미네이트 및 플라스틱 수지 세계 시장 규모는 2024년에 7,756억 달러로 평가되었고, CAGR 5.1%로 성장하여 2034년에는 1조 2,800억 달러에 달할 것으로 예측됩니다.

시장의 기세는 특히 건설용 액세서리, 소비자용 패키징, 공업 제품, 모빌리티 솔루션 등 여러 부문에 걸친 광범위한 용도에 의해 견인되고 있습니다. 가볍고 비용 효율적이며 고강도 소재에 대한 수요가 증가함에 따라 고압 라미네이트(HPL)와 플라스틱 수지 모두에서 성장세를 이어가고 있으며, 시장 점유율에서는 수지가 리드하고 있습니다. 플라스틱 수지는 그 가공성, 내구성, 범용성으로부터, 광범위한 상품에 있어서 불가결한 원재료가 계속되고 있기 때문에 당분간 세계 마켓플레이스에서의 우위성을 유지할 것으로 예측됩니다.

HPL은 시장 점유율이 작은 것, 인테리어 디자인 및 건축 용도에서의 채택이 증가하고 있기 때문에 견인력을 늘리고 있습니다. 디자인 트렌드는 시각적 매력뿐만 아니라 최소한의 유지보수가 필요한 표면으로 변화하고 있어 라미네이트에 대한 관심이 높아지고 있습니다. 기능과 미관을 겸비한 소재에 대한 수요가 높아짐에 따라, HPL은 보다 강력한 부문이 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 7,756억 달러 |

| 예측 금액 | 1조 2,800억 달러 |

| CAGR | 5.1% |

신흥 경제 국가와 선진 경제 국가를 불문하고 도시 개발과 인프라의 근대화가 진행되고 시장의 성장이 더욱 가속화되고 있습니다. 라미네이트와 플라스틱 수지 모두가 가져다주는 특성을 갖춘 설계 제품으로 꾸준히 이행하고 있습니다.

제품 유형별로 볼 때 시장은 고압 라미네이트(HPL), 연속압 라미네이트(CPL), 플라스틱 수지로 구분됩니다. 이 부문은 예측 기간 동안 CAGR 5.1%로 성장할 것으로 예상됩니다. 플라스틱 수지의 주요 이점은 경제적인 생산 가치, 가공의 용이성, 폭넓은 재료의 다양성을 제공하며, 여러 산업에서 기초 부품으로서 기능하는 능력에 있습니다.

재료의 혁신이 이 시장의 미래를 형성하고 있습니다. 첨단 수지 화학과 재활용 가능한 폴리머를 통해 환경 성능을 향상시키려는 노력은 제조업체 각사의 사업 방식을 바꾸고 있습니다. 환경 친화적인 재료를 제조하는 방향으로의 변화가 현저해지고 있습니다. 재활용 가능한 플라스틱과 바이오베이스 플라스틱의 채택은 점차 증가하고 있으며, 환경 컴플라이언스 및 각 분야의 녹색 이니셔티브와 보조를 맞추고 있습니다.

최종 이용 산업별로 분석하면 시장은 주택, 상업, 헬스케어, 운송, 공업 등으로 분류됩니다. 2024년 주거 부문은 전체 시장의 약 32.2%를 차지했습니다.

중국은 이 시장의 세계 궤도를 형성하는데 있어 매우 중요한 역할을 하고 있습니다. CAGR 5.3%로 성장할 것으로 예상됩니다. 중국의 광범위한 제조 거점은 최종 사용자 산업에서의 국내 소비 증가와 함께 세계 생산과 수요의 최전선에 위치하고 있습니다.

고압 라미네이트 및 플라스틱 수지 시장 경쟁 구도는 상위 5개 기업이 세계 점유율의 30% 이상을 차지하고 있으며, 완만하게 통합되어 있습니다. 이를 통해 경쟁력을 유지하고 있습니다. 라미네이트 분야에서는 강력한 브랜드 아이덴티티, 폭넓은 제품 변형, 광범위한 판매망을 가진 기업이 계속해서 높은 실적을 올리고 있습니다. 지속가능성, 혁신성, 효율적인 가격설정은 각 사가 소비자의 신뢰를 구축하고 각 지역에서 진화하는 법규제의 요구에 부응하려고 노력하는 가운데 여전히 중심적인 전략이 되고 있습니다.

The Global High Pressure Laminates and Plastic Resins Market was valued at USD 775.6 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 1.28 trillion by 2034. Market momentum is being driven by widespread application across multiple sectors, especially in construction accessories, consumer packaging, industrial goods, and mobility solutions. The growing demand for lightweight, cost-efficient, and high-strength materials continues to fuel growth in both high-pressure laminates (HPL) and plastic resins, with resins leading the way in terms of market share. As plastic resins remain essential raw materials for a wide spectrum of goods due to their processability, durability, and versatility, they are expected to maintain their dominance in the global marketplace for the foreseeable future.

HPL, although smaller in market share, is gaining traction due to its increasing adoption in interior design and architectural applications. Known for their resilience and design flexibility, HPL materials are frequently preferred in residential and commercial installations. Trends in design are shifting towards surfaces that offer not only visual appeal but also require minimal upkeep, boosting interest in laminates. As demand grows for materials that combine function with aesthetics, HPL is becoming a stronger segment. Meanwhile, plastic resins remain in high-volume circulation due to their cost-efficient nature and adaptability in mass manufacturing.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $775.6 Billion |

| Forecast Value | $1.28 Trillion |

| CAGR | 5.1% |

Increased urban development and modernization of infrastructure across emerging and developed economies alike are further accelerating market growth. Industries seek advanced materials that deliver not just structural value but also sustainability. Design preferences are steadily moving toward engineered products that offer low maintenance, weather resistance, and lightweight performance-all attributes that both laminates and plastic resins bring to the table. This consistent demand for materials that fulfill evolving design and utility requirements ensures continued relevance for both segments, although at different scales.

By product type, the market is segmented into high pressure laminates (HPL), continuous-pressure laminates (CPL), and plastic resins. Among these, plastic resins accounted for a significant market share, with a recorded revenue of USD 756.4 billion in 2024. This segment is expected to expand at a CAGR of 5.1% throughout the forecast period. The key advantage of plastic resins lies in their ability to serve as foundational components across multiple industries, offering economic production value, ease of fabrication, and broad material diversity. Their performance in structural and non-structural applications-ranging from packaging to electronics-reinforces their leadership position.

Material innovation is shaping the future of this market. Efforts to improve environmental performance through advanced resin chemistry and recyclable polymers are reshaping how manufacturers operate. There is a noticeable shift toward producing high-performance, eco-conscious materials that support long-term sustainability goals. The adoption of recyclable and bio-based plastics is gradually rising, aligning with environmental compliance and green initiatives across sectors.

When analyzed by end-use industry, the market is classified into residential, commercial, healthcare, transportation, industrial, and others. The commercial segment currently commands the highest market share, largely due to the consistent use of both plastic resins and HPLs in public infrastructure, corporate offices, retail chains, and other high-traffic commercial environments. In 2024, the residential sector accounted for approximately 32.2% of the overall market. Increasing design consciousness and the need for durable, easy-to-clean surfaces in modern homes continue to stimulate HPL usage in residential applications. Plastic resins, on the other hand, dominate a wide array of uses across interiors, decor, and safety applications in both residential and commercial properties.

China plays a pivotal role in shaping the global trajectory of this market. In 2024, the Chinese market generated revenue of USD 156.4 billion and is on track to reach USD 262.6 billion by 2034, growing at a CAGR of 5.3%. China's extensive manufacturing base, combined with rising domestic consumption in end-user industries, places it at the forefront of global production and demand. The surge in urban development, infrastructure expansion, and consumer upgrades contributes to increased usage of both laminates and resins within the country.

The competitive landscape of the high-pressure laminates and plastic resins market is moderately consolidated, with the top five companies controlling over 30% of the global share. The plastic resins space is highly influenced by producers focused on volume scalability, global logistics capabilities, and multipurpose product lines. These players maintain their competitive edge through innovations in sustainable materials, aggressive R&D programs, and responsive production models. On the laminates side, companies with a strong brand identity, wide product variety, and expansive distribution continue to outperform. Sustainability, innovation, and efficient pricing remain core strategies as companies work to build consumer trust and meet evolving regulatory demands across regions.

3.11.1 Major importing countries