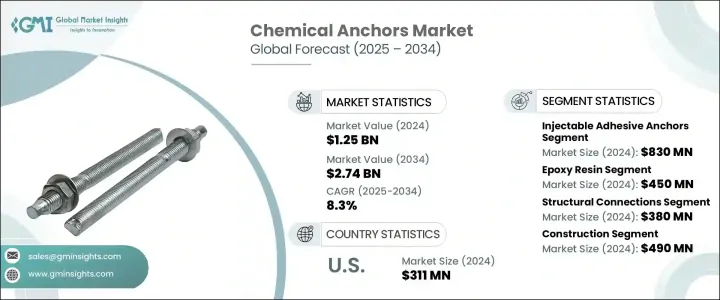

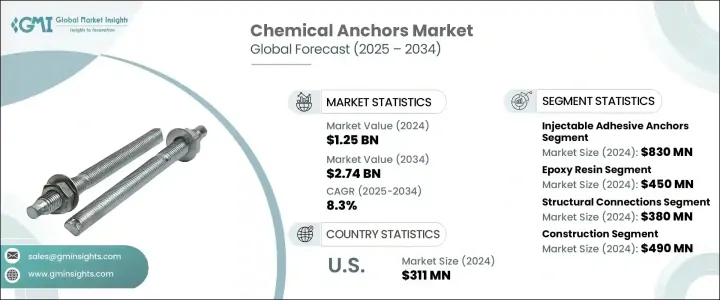

세계의 화학 앵커 시장 규모는 2024년에 12억 5,000만 달러로 평가되었고, 2034년에는 27억 4,000만 달러에 이를 것으로 예측되며, CAGR 8.3%로 성장할 전망입니다.

이러한 성장은 전 세계적으로 증가하는 건설 활동에 크게 촉진되고 있습니다. 도시 인구가 증가하고 도시화가 가속화되면서 고급 건설 기술과 현대적 인프라에 대한 수요가 지속적으로 증가하고 있습니다. 이에 대응해 화학 앵커는 다양한 복잡성과 규모의 건물에서 구조적 요소를 고정하는 필수적인 구성 요소로 자리 잡고 있습니다. 이러한 앵커링 솔루션은 구조적 응용 분야에서 강하고 오래 지속되는 결합력을 제공하며, 주거용, 상업용, 산업용 분야를 걸쳐 확산되고 있습니다.

도시화가 심화됨에 따라 까다로운 환경에서 성능과 안전을 모두 보장하는 앵커링 시스템에 대한 필요성이 증가하고 있습니다. 구조가 점점 더 복잡해지고 지속 가능성에 대한 관심이 높아짐에 따라 엔지니어와 계약업체들은 신뢰할 수 있는 고정력을 갖춘 화학 앵커로 눈을 돌리고 있습니다. 화학 앵커는 콘크리트 및 보강철근에 높은 접착력을 발휘하기 때문에 전 세계적으로 인프라 개발 및 리모델링 프로젝트에 점점 더 많이 채택되고 있습니다. 동적 및 정적 하중을 처리할 수 있는 능력으로 인해 현대의 건설 요구 사항에 특히 적합합니다. 기업들은 이제 엄격한 안전 기준을 충족하는 고성능 고정 솔루션을 제조하는 데 집중하고 있으며, 다양한 응용 분야에서 채택을 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 12억 5,000만 달러 |

| 예측 금액 | 27억 4,000만 달러 |

| CAGR | 8.3% |

제품 유형에 따라 시장은 주입형 접착 앵커, 캡슐 접착 앵커 및 화학 앵커 고정 장치로 구분됩니다. 주입형 접착 앵커 부문은 2024년에 8억 3,000만 달러의 가치로 시장을 주도했으며, 2034년까지 연평균 8.9%의 성장률을 보일 것으로 예상됩니다. 이 부문의 우위는 사용 편의성, 다양한 건설 응용 분야에서의 다용성, 엄격한 조건에서도 우수한 성능에 기인합니다. 이러한 앵커는 정밀한 하중 지지 성능과 빠른 설치 시간이 요구되는 지역에서도 강한 일관된 접착력을 제공할 수 있어 선호됩니다. 수지 배합 기술의 발전도 더 빠른 경화 시간과 향상된 신뢰성을 가능하게 함으로써 그 인기를 높이는 데 기여했습니다.

수지 유형에 따라 시장은 비닐 에스테르 수지, 에폭시 아크릴레이트, 에폭시 수지, 폴리에스터 수지 및 하이브리드 시스템으로 분류됩니다. 에폭시 수지 부문은 2024년에 4억 5,000만 달러로 평가되었으며, 예측 기간 동안 연평균 9%의 성장률을 보일 것으로 예상됩니다. 에폭시 기반 화학 앵커는 높은 기계적 강도, 우수한 화학 저항성, 고하중 환경에서의 신뢰성 있는 접착력으로 인해 중공업 건설 환경에서 널리 선호됩니다. 이 레진은 빠른 경화 능력과 극한 환경 조건에서도 우수한 성능을 발휘해 구조적 안정성이 중요한 프로젝트에서 필수적인 선택지로 자리매김했습니다.

이 시장은 구조물 연결, 철근 연결, 중장비 장착, 외관 설치, 난간 및 안전 장벽, 내진 보강 등 다양한 분야를 포함합니다. 구조물 연결 부문은 2024년에 3억 8,000만 달러의 가치를 기록했으며, 2025년부터 2034년까지 연평균 8.8%의 성장률을 보일 것으로 예상됩니다. 이 부문은 다양한 건축 형식에서 안정성과 안전을 보장하는 중요한 역할을 수행하기 때문에 상당한 점유율을 차지하고 있습니다. 고층 건물과 현대적인 인프라 시스템이 발전함에 따라 구조용 조인트에 대한 강력한 앵커링 솔루션에 대한 수요가 꾸준히 증가하고 있습니다. 이러한 용도에 화학 앵커를 사용하면 하중을 안전하게 전달하고 주변 자재에 대한 손상을 최소화할 수 있습니다.

건설 부문은 2024년에 4억 9,000만 달러의 규모로 가장 큰 최종 사용 산업으로 부상했으며, 7.8%의 CAGR로 성장하여 39.5%의 시장 점유율을 차지할 것으로 예상됩니다. 급속한 도시 개발, 상업용 부동산의 확장, 안전하고 지속 가능한 건축 관행에 대한 관심의 증가와 같은 동향은 모두 이 부문의 중요성을 높이는 요인이 되었습니다. 건축업자와 개발업자는 현대 건축 요구 사항에 대한 적응성, 강도 및 호환성을 위해 화학 앵커에 점점 더 의존하고 있습니다. 설계의 복잡성과 구조물의 높이가 계속 증가함에 따라 신뢰할 수 있는 앵커링 솔루션에 대한 필요성은 계속 높을 것입니다.

지역별로 미국의 화학 앵커 시장은 2024년 3억 1,100만 달러로 평가되었으며, 2034년까지 연평균 성장률(CAGR) 8%로 성장할 것으로 예상됩니다. 인프라 업그레이드 증가와 지진 보강 기준의 확산이 수요를 촉진하고 있습니다. 또한 건설 규정 개정과 주거 및 상업용 리모델링 투자 증가도 시장 성장을 지원하고 있습니다. 주요 제조업체들의 기술 혁신과 신제품 개발은 화학 앵커의 적용 범위를 확장하며 시장 침투 기회를 제공하고 있습니다.

선도적인 업계 기업들은 지속적인 혁신, 브랜드 개발, 광범위한 국제 유통망을 통해 경쟁 우위를 유지하고 있습니다. 이들 기업은 다양한 환경 조건에서 우수한 하중 지지 능력, 빠른 경화 시간, 신뢰성 있는 성능을 제공하는 고급 포뮬레이션 생산에 집중하고 있습니다. 지속 가능성과 전 세계 안전 표준 준수를 중시하는 주요 제조업체들은 진화하는 규제 요건에 따라 제품 라인을 조정하고 있습니다. 또한, 파트너십, 합병 및 전략적 인수를 통한 확장 노력으로 신흥 시장과 성숙한 시장에서 입지를 강화하고 있습니다. 이 산업은 또한 다양한 건설 요구에 맞는 전문적인 기술 지원, 고급 교육 프로그램 및 통합 솔루션에 의해 형성되고 있습니다.

(참고 : 무역 통계는 주요 국가에서만 제공됩니다)

The Global Chemical Anchors Market was valued at USD 1.25 billion in 2024 and is estimated to grow at a CAGR of 8.3% to reach USD 2.74 billion by 2034. This growth is largely driven by the increasing volume of construction activity worldwide. As urban populations expand and cities develop rapidly, the demand for advanced construction techniques and modern infrastructure continues to rise. In response, chemical anchors are becoming essential components for securing various structural elements in buildings of varying complexity and size. These anchoring solutions provide strong, long-lasting bonds in structural applications and are gaining traction across residential, commercial, and industrial sectors.

As urbanization intensifies, there is a growing need for anchoring systems that ensure both performance and safety in demanding environments. With more complex structures being built and an increased focus on sustainability, engineers and contractors are turning to chemical anchors for reliable fastening. They are particularly effective in delivering high-strength adhesion to concrete and reinforcement bars, which is why they are being increasingly adopted in infrastructure development and renovation projects globally. Their ability to handle dynamic and static loads makes them especially suitable for modern-day construction requirements. Companies are now concentrating on manufacturing high-performance anchoring solutions that meet stringent safety standards, driving adoption across diverse applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.25 billion |

| Forecast Value | $2.74 billion |

| CAGR | 8.3% |

In terms of product types, the market is segmented into injectable adhesive anchors, capsule adhesive anchors, and chemical anchor fixings. The injectable adhesive anchors segment led the market in 2024 with a valuation of USD 830 million and is expected to grow at a CAGR of 8.9% through 2034. Its dominance is attributed to its ease of use, versatility across multiple construction applications, and superior performance in demanding scenarios. These anchors are favored for their ability to provide strong, consistent bonding, even in areas that require precise load-bearing performance and fast installation times. Technological advancements in resin formulations have also contributed to their rising popularity by enabling faster curing and improved reliability.

Based on resin types, the market is categorized into vinyl ester resin, epoxy acrylate, epoxy resin, polyester resin, and hybrid systems. The epoxy resin segment was valued at USD 450 million in 2024 and is anticipated to expand at a CAGR of 9% during the forecast period. Epoxy-based chemical anchors are widely preferred in heavy construction environments due to their high mechanical strength, excellent resistance to chemicals, and dependable bonding in high-load settings. These resins also offer rapid curing capabilities and perform well under extreme environmental conditions, making them the go-to option in projects where structural integrity is critical.

When analyzed by application, the market includes structural connections, rebar connections, heavy equipment mounting, facade installations, handrails and safety barriers, seismic retrofitting, and others. The structural connections segment recorded a value of USD 380 million in 2024 and is projected to grow at a CAGR of 8.8% from 2025 to 2034. This segment holds a significant share as it fulfills a crucial role in ensuring stability and safety across a broad range of construction formats. With the evolution of high-rise buildings and modern infrastructure systems, the demand for strong anchoring solutions in structural joints is growing steadily. The use of chemical anchors in these applications allows for secure load transfer and minimal disruption to surrounding materials.

The construction segment emerged as the largest end-use industry in 2024, valued at USD 490 million, and is forecasted to grow at a CAGR of 7.8%, capturing a market share of 39.5%. The growing trend of rapid urban development, expansion in commercial real estate, and increased focus on safe and sustainable construction practices have all contributed to the segment's prominence. Builders and developers increasingly rely on chemical anchors for their adaptability, strength, and compatibility with modern construction requirements. As design complexity and structural heights continue to rise, the need for reliable anchoring solutions will remain high.

In terms of regional performance, the United States chemical anchors market was valued at USD 311 million in 2024 and is anticipated to grow at a CAGR of 8% through 2034. The rise in infrastructure upgrades, coupled with the increasing adoption of seismic retrofitting standards, is fueling demand. Additionally, market growth is supported by updates in construction regulations and rising investments in residential and commercial renovations. Technological enhancements and innovations from top manufacturers are also expanding the application scope of chemical anchors, offering new opportunities for market penetration.

Leading industry players maintain a competitive edge through continuous innovation, brand development, and broad international distribution channels. These companies focus on producing advanced formulations that offer superior load-bearing capabilities, faster curing times, and reliable performance under varying environmental conditions. With an emphasis on sustainability and compliance with global safety standards, major manufacturers are aligning their product lines with evolving regulatory requirements. Moreover, expansion efforts through partnerships, mergers, and strategic acquisitions are enabling them to strengthen their presence across emerging and mature markets. The industry is also shaped by specialized technical support, advanced training programs, and integrated solutions tailored to diverse construction needs.

( Note: the trade statistics will be provided for key countries only)