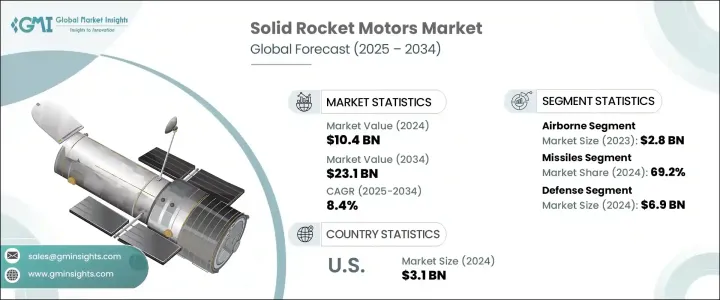

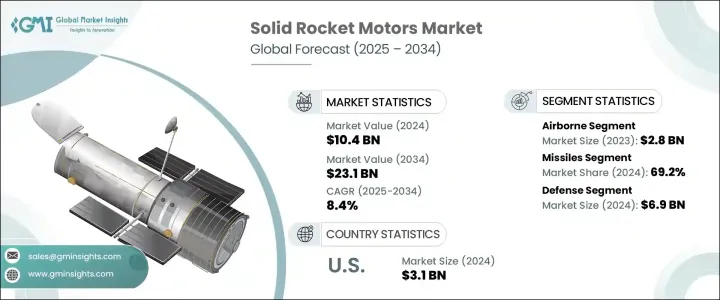

세계의 고체 로켓 모터 시장 규모는 2024년에는 104억 달러로 세계 방위 예산 증가와 최신 미사일 로켓 시스템의 필요성으로 인해 2034년에는 231억 달러에 달할 것으로 예측되며, CAGR 8.4%로 성장할 전망입니다.

전 세계 고체 로켓 모터 시장은 2024년에 104억 달러로 평가되었으며, 전 세계 국방 예산의 증가와 현대적인 미사일 및 발사체 시스템에 대한 수요에 힘입어 2034년에는 연평균 8.4%의 성장률을 보이며 231억 달러에 달할 것으로 예상됩니다. 고체 로켓 모터는 단순성, 높은 추력 출력, 빠른 점화 및 긴 저장 수명으로 인해 주목을 받고 있으며, 군용 및 항공우주 용도에 이상적입니다. 경제 및 정치 발전은 공급망에 영향을 미치고 부품 비용을 증가시켜 시장 트렌드에 더욱 영향을 미치고 있습니다. 이러한 도전에도 불구하고, 각국은 국가 안보 이니셔티브 및 미사일 기술에 계속해서 막대한 투자를 하고 있으며, 신뢰할 수 있고 확장 가능한 추진 시스템에 대한 수요를 강화하고 있습니다.

고체 로켓 모터는 방위 프로그램 전반에 걸쳐 필수적인 부품으로, 지대공, 전술 탄도 및 요격 미사일 시스템에 적합한 소형 폼 팩터로 고성능을 제공합니다. 모듈식이며 적응력이 뛰어난 추진 기술은 특정 임무 요구 사항을 지원하면서 비용을 최적화하기 때문에 필수적인 요소가 되고 있습니다. 이 시장은 기동성, 사거리 및 발사 정밀도를 향상시키기 위한 지속적인 혁신의 혜택을 받고 있습니다. 각국이 억지력과 우주 능력에 대한 관심을 강화함에 따라 고체 모터는 전 세계 방위 및 항공우주 인프라에 없어서는 안 될 부분으로 남아 있습니다.

| 시장 범위 | |

|---|---|

| 시장 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 104억 달러 |

| 예측 금액 | 231억 달러 |

| CAGR | 8.4% |

위성 발사체 부문은 비용 효율적이고 신뢰성이 높은 발사 솔루션에 대한 수요가 증가함에 따라 2024년에 30.8%의 점유율을 차지했습니다. 고체 추진 시스템은 유지보수가 최소화되고 배포가 용이하기 때문에 중소형 발사 플랫폼에서 널리 선호되고 있습니다. 위성 배치에 대한 공공 및 민간 이니셔티브가 증가함에 따라, 신속하고 신뢰할 수 있는 궤도 발사의 요구를 충족하기 위해 고체 로켓 모터가 점점 더 많이 사용되고 있습니다.

2024년에는 방위 부문이 69억 달러를 창출하여 고체 로켓 모터 시장에서 지배적인 최종 사용 부문으로 자리매김했습니다. 첨단 전술 무기 시스템 및 미사일 업그레이드에 대한 지속적인 수요는 전 세계 군이 신속한 대응 능력과 기술 우위를 우선시하기 때문에 직접적으로 발생한 결과입니다. 높은 추력 대 중량 비, 최소한의 유지보수 요구 사항 및 안정적인 보관으로 잘 알려진 고체 로켓 모터는 이러한 목표에 부합합니다. 여러 지역에서 진행 중인 군의 현대화와 전략적 국방 이니셔티브는 고체 추진 시스템의 채택을 더욱 확대했습니다.

미국의 고체 로켓 모터 2024년 시장 규모는 31억 달러로 미국은 고체 추진 기술의 세계 리더로서의 역할을 강화하고 있습니다. 국방 및 항공우주 프로그램에 대한 강력한 예산 배정은 이러한 모멘텀을 계속 촉진하고 있습니다. 초음속 시스템, 차세대 미사일 플랫폼 및 재사용 가능한 발사체에 대한 투자는 고체 모터 기술의 국내 생산 및 혁신을 촉진하고 있습니다. 미국 군대의 고급 미사일 시스템 배치에 대한 공격적인 일정과 NASA의 심우주 탐사 재강조는 소형화되고 고효율적인 추진 솔루션에 대한 수요를 촉진하고 있습니다.

Aerojet Rocketdyne, L3 Harris Technologies, Northrop Grumman, RAFAEL Advanced Defense Systems Ltd.와 같은 선도 기업들은 정부 및 상업용 응용 분야를 지원하는 다양한 플랫폼에 적용 가능한 고체 로켓 모터 시스템을 혁신하고 있습니다. 시장 지위를 공고히 하기 위해 주요 기업들은 다양한 발사 및 방위 시스템에 걸쳐 향상된 유연성과 확장성을 제공하는 모듈형 모터 기술에 투자하고 있습니다. 기업들은 제조 효율성 개선, 생산 비용 절감, 차세대 복합 재료 연구 개발 확대에 집중하고 있습니다. 우주 및 방위 기관과의 협력을 통해 진화하는 임무 프로필에 맞는 고체 추진 솔루션을 맞춤형으로 개발하며, 전략적 계약 및 인수합병을 통해 시장 침투를 강화하고 있습니다.

The Global Solid Rocket Motors Market was valued at USD 10.4 billion in 2024 and is estimated to grow at a CAGR of 8.4% to reach USD 23.1 billion by 2034, driven by rising global defense budgets and the need for modern missile and launch vehicle systems. Solid rocket motors are gaining traction due to their simplicity, high-thrust output, fast ignition, and long shelf life, making them ideal for military and aerospace use. Economic and political developments have affected supply chains and increased component costs, further influencing market trends. Despite these challenges, countries continue to invest heavily in national security initiatives and missile technologies, reinforcing the demand for reliable and scalable propulsion systems.

Solid rocket motors are vital components across defense programs, offering high performance in a compact form factor suitable for surface-to-air, tactical ballistic, and interceptor missile systems. Modular and adaptable propulsion technologies are becoming essential as they support specific mission requirements while optimizing cost. The market benefits from ongoing innovations to enhance maneuverability, range, and launch precision. As nations intensify their focus on deterrence and space capabilities, solid motors remain an indispensable part of defense and aerospace infrastructure worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.4 Billion |

| Forecast Value | $23.1 Billion |

| CAGR | 8.4% |

The satellite launch vehicle segment is projected to hold a 30.8% share in 2024, driven by the growing need for cost-efficient, high-reliability launch solutions. Solid propulsion systems are widely favored in small to medium-sized launch platforms due to their minimal maintenance and ease of deployment. As both public and private initiatives in satellite deployment grow, solid rocket motors are increasingly used to meet the needs of rapid and dependable orbital launches.

In 2024, the defense segment generated USD 6.9 billion, establishing itself as the dominant end-use category in the solid rocket motors market. The consistent demand for advanced tactical weapon systems and missile upgrades is a direct result of global military forces prioritizing rapid response capabilities and technological superiority. Solid rocket motors, known for their high thrust-to-weight ratio, minimal maintenance requirements, and dependable storage, align well with these objectives. Ongoing modernization of armed forces across several regions, coupled with strategic defense initiatives, has further amplified the adoption of solid propulsion systems.

United States Solid Rocket Motors Market generated USD 3.1 billion in 2024, reinforcing the country's role as a global leader in solid propulsion technologies. A robust budget allocation toward national defense and aerospace programs continues to drive this momentum. Investments in hypersonic systems, next-generation missile platforms, and reusable launch vehicles are helping fuel domestic production and innovation in solid motor technologies. The U.S. military's aggressive timeline for deploying advanced missile systems and NASA's renewed emphasis on deep space exploration are pushing demand for compact, high-efficiency propulsion solutions.

Leading firms such as Aerojet Rocketdyne, L3Harris Technologies, Inc., Northrop Grumman, and RAFAEL Advanced Defense Systems Ltd. are innovating solid motor systems that support government and commercial applications across various platforms. To solidify their market position, key companies are investing in modular motor technologies that provide enhanced flexibility and scalability across different launch and defense systems. Firms focus on improving manufacturing efficiencies, reducing production costs, and expanding R&D in next-gen composite materials. Collaborations with space and defense agencies help tailor solid propulsion solutions to evolving mission profiles, while strategic contracts and acquisitions enable deeper market penetration.