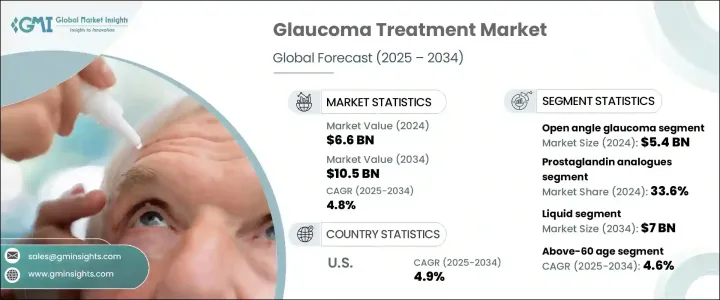

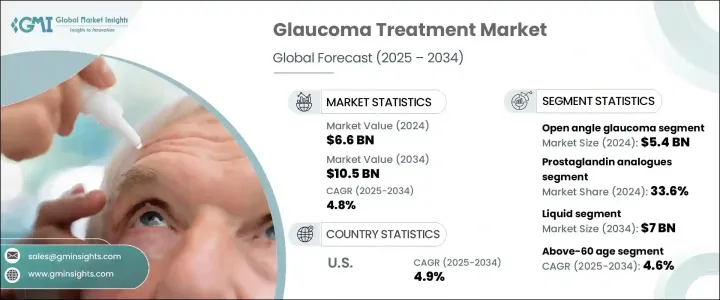

세계의 녹내장 치료 시장은 2024년에 66억 달러로 평가되었으며 CAGR 4.8%를 나타내 2034년에는 105억 달러에 이를 것으로 추정됩니다.

세계의 인구의 고령화가 진행됨에 따라 노화와 관련된 안구 질환의 증례가 더 빈번하고 심각해지고 있으며 조기 진단과 장기 치료의 필요성이 높아지고 있습니다. 중대한 위험 인자인 당뇨병이나 고혈압 등의 만성 질환도 증가 경향에 있어, 다양한 층에서 효과적이고 장기적인 치료 옵션에 대한 수요가 높아지는 원인이 되고 있습니다.

정부와 보건 기관은 조기 검진이나 정기적인 안과 검진을 추진하는 계발 캠페인에 힘을 넣기 시작하고 있어, 녹내장의 조기 발견에 도움이 되고 있습니다. 이것에 의해 치료 개시가 현저하게 증가하고 있습니다. 용도도 치료 옵션을 넓혀 환자의 결과를 개선하고 있습니다. 또한, 의료 인프라의 개선과 가처분 소득 증가(특히 신흥 시장)에 의해 안과 의료가 보다 친숙해지게 되어, 보다 폭넓은 층의 사람들이 시기 적절하고 고도의 녹내장 관리를 받게 되어 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 66억 달러 |

| 예측 금액 | 105억 달러 |

| CAGR | 4.8% |

개방각 녹내장은 여전히 가장 많이 진단되는 질환이며, 세계 전체의 증례의 70% 이상을 차지하며, 2024년 시장 규모는 54억 달러였습니다. 안압을 낮추는 약물에 초점을 맞추었습니다. 개방 구석 각 녹내장은 천천히 개발되어 많은 경우, 중대한 시력 저하가 일어날 때까지 명백한 증상은 없습니다.

체액 배출을 촉진하여 안압을 낮추는 프로스타글란딘 아날로그는 2024년 치료 시장에서 33.6%의 가장 높은 점유율을 차지했으며 2034년에는 37억 달러에 달할 것으로 예측되고 있습니다. 부작용 프로파일은 개방 각도 녹내장 관리에 널리 처방되고 있습니다. 고령화가 진행되는 동안, 특히 방부제 프리로 사용하기 편리한 점안제를 선택하는 환자가 늘어남에 따라, 이러한 약제 수요는 더욱 높아질 것으로 예측됩니다.

2024년 미국의 녹내장 치료 시장 규모는 22억 4,000만 달러에 달했고 2034년까지 연평균 복합 성장률(CAGR) 4.9%를 나타낼 것으로 예측됩니다. 치료에 대한 광범위한 접근을 지원하는 한편, 임상시험과 FDA 승인에 대한 지속적인 투자는 이용가능한 의약품 파이프라인을 급속히 확대하고 있습니다.

Novartis, Pfizer, Santen Pharmaceutical, Sun Pharmaceutical, Thea, Alcon, Cipla, AbbVie, Bausch & Lomb, Inotek Pharmaceuticals, Eyepoint Pharmaceuticals, Teva Pharmaceutical, Merck, Grevis Pharmaceuticals 등의 기업이 이 분야에서 적극적으로 경쟁하고 있습니다. 네트워크를 통해 고성장 신흥 시장에 진출하는 것도 중요한 전략입니다. 또한, 조기 개입과 지속적인 케어를 지원하기 위해, 기업은 디지털 관여 툴이나 원격 환자 모니터링 기술을 강화하고 있습니다.

The Global Glaucoma Treatment Market was valued at USD 6.6 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 10.5 billion by 2034, attributed to the rising incidence of glaucoma worldwide, especially among older adults. As the global population continues to age, cases of age-related ocular disorders are becoming more frequent and severe, prompting a greater need for early diagnosis and long-term care. Chronic illnesses such as diabetes and hypertension-both significant risk factors for developing glaucoma-are also on the rise, which further contributes to increasing demand for effective and long-lasting treatment options across various demographics.

Governments and health agencies have started focusing on awareness campaigns to promote early screening and routine eye examinations, which is helping detect glaucoma at earlier stages. This has led to a notable rise in treatment initiations. The market is also benefiting from the adoption of novel drug classes, including Rho kinase inhibitors and fixed-dose combination therapies, which are expanding treatment alternatives and improving patient outcomes. Additionally, improving healthcare infrastructure and growing disposable incomes-especially in emerging markets-are making ophthalmic care more accessible, enabling a broader segment of the population to pursue timely and advanced glaucoma management.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.6 Billion |

| Forecast Value | $10.5 Billion |

| CAGR | 4.8% |

Open-angle glaucoma remains the most diagnosed form of the disease, accounting for more than 70% of global cases and valued at USD 5.4 billion in 2024. Treating glaucoma revolves around managing intraocular pressure (IOP) to prevent irreversible optic nerve damage. Most therapies focus on medications that help reduce IOP, including beta-blockers, alpha agonists, carbonic anhydrase inhibitors, and prostaglandin analogs. Open angle glaucoma condition develops slowly and often without obvious symptoms until significant vision loss occurs. Its chronic nature means patients require continuous and long-term care, creating sustained demand for pharmaceutical solutions and regular monitoring services.

Prostaglandin analogs, which help lower eye pressure by enhancing fluid drainage, commanded the highest share of the treatment market in 2024, making up 33.6% share and is projected to reach USD 3.7 billion by 2034. Their effectiveness and relatively mild side effect profile make them widely prescribed for managing open-angle glaucoma. With aging populations increasing, the demand for these medications is expected to climb further, particularly as more patients opt for preservative-free and user-friendly eye drop formulations.

U.S. Glaucoma Treatment Market generated USD 2.24 billion in 2024 and is set to grow at a 4.9% CAGR through 2034. The country's aging population and high awareness levels, coupled with the strong presence of pharmaceutical innovators, continue to fuel demand for advanced treatment options. A well-established healthcare infrastructure supports early diagnosis and widespread access to prescription therapies, while ongoing investments in clinical trials and FDA approvals are rapidly expanding the available drug pipeline. Increased insurance coverage and favorable reimbursement policies are further supporting treatment adoption among the elderly and high-risk groups.

Companies like Novartis, Pfizer, Santen Pharmaceutical, Sun Pharmaceutical, Thea, Alcon, Cipla, AbbVie, Bausch & Lomb, Inotek Pharmaceuticals, Eyepoint Pharmaceuticals, Teva Pharmaceutical, Merck, and Grevis Pharmaceuticals are actively competing in this space. To secure a competitive edge in the glaucoma treatment market, leading companies are investing heavily in R&D to develop next-generation therapies with improved efficacy and safety. They are focusing on fixed-dose combinations to simplify treatment regimens and improve patient adherence. Expanding into high-growth emerging markets through partnerships and distribution networks is another key strategy. Additionally, firms are enhancing digital engagement tools and remote patient monitoring technologies to support early intervention and ongoing care. Strategic collaborations, pipeline diversification, and product lifecycle management remain central to strengthening market positioning across global regions.