Contrast Media Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1750572

리서치사:Global Market Insights Inc.

발행일:2025년 05월

페이지 정보:영문 141 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

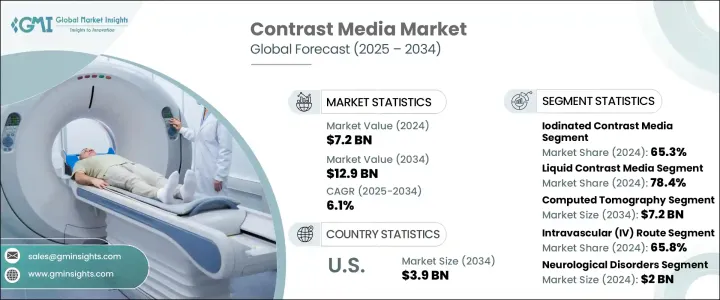

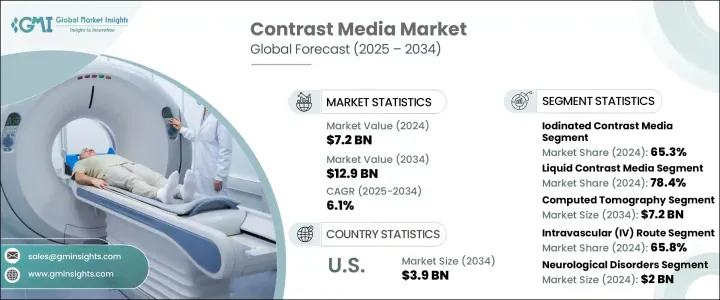

세계의 조영제 주입기 시장은 2024년에 72억 달러로 평가되었으며, 광범위한 만성 건강 상태를 진단 및 관리하기 위한 의료 영상 진단 수요가 증가함에 따라 CAGR 6.1%를 나타내 2034년에는 129억 달러에 달할 것으로 예측되고 있습니다.

정확하고 조기 진단의 필요성이 높아짐에 따라, MRI, CT, X선, 초음파 등의 화상 진단 기술도 증가해, 이러한 기술은 선명함과 세부를 개선하기 위해 조영제에 크게 의존하고 있습니다.

조영 이미지는 조직, 혈관, 장기의 미묘한 이상을 식별하는 데 유용합니다. 이것은 조기 발견이 보다 효과적인 치료 계획으로 이어지는데 특히 중요합니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

72억 달러

예측 금액

129억 달러

CAGR

6.1%

2024년 요오드 조영제가 65.3%의 점유율로 시장을 견인했습니다. 요오드 조영제는 CT나 X선 검사에 널리 사용되고 있습니다.에서 정확한 영상 진단에 필수적입니다. 시인성이 향상됨으로써 진단 및 치료 계획이 보다 확실해집니다.

액체 조영제 부문은 2024년에 78.4%의 점유율을 차지했습니다. 액체 약제가 널리 사용되는 주된 이유는 간단한 투여 방법, 신속한 흡수, 내부 구조의 효과적인 시각화 등 실용적인 이점에 있습니다. 다양한 영상 진단 시스템에 적합하고 혈류를 신속하게 순환시킬 수 있기 때문에 신속하고 정확한 진단 데이터를 필요로 하는 임상의는 최적의 선택이 되고 있습니다.

미국의 조영제 주입기 시장은 2024년에 23억 달러에 이르렀고, 2034년에는 39억 달러에 이를 것으로 예측되고 있습니다. 스크리닝과 모니터링 모두에서 MRI와 CT 기술의 사용이 증가하고 있다는 것은 조영제에 대한 안정적인 수요를 뒷받침하고 있습니다.

이 시장의 유력 기업은 TAEJOON Pharmaceutical, GE HealthCare Technologies, Livealth Biopharma, Bracco, Unijules Life Sciences, Guerbet, Trivitron Healthcare, nanoPET Pharma, Senochemia Pharmazeutika, Bayer, Jodas Expoim, JB &Pharmaceuticals, Fresenius, Lantheus, iMAX Diagnostic Imaging 등이 있습니다. 시장에서의 존재감을 높이기 위해, 주요 기업은 안전성을 향상시킨 차세대 조영제의 연구 개발에 투자하고 있습니다. 정밀촬영을 지원하고 조영제 복용량을 줄이기 위한 AI 통합 플랫폼을 모색하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

업계에 미치는 영향요인

성장 촉진요인

조영제의 규제 승인 증가

방사선 검사 증가

만성질환의 발생률 급증

저침습 수술 증가

업계의 잠재적 리스크 및 과제

엄격한 규제와 빈번한 제품 리콜의 존재

조영제와 관련된 알레르기 반응과 부작용

성장 가능성 분석

규제 상황

트럼프 정권에 의한 관세에 대한 영향

무역에 미치는 영향

무역량의 혼란

국가별 대응

업계에 미치는 영향

공급측의 영향(제조 비용)

주요 원재료의 가격 변동

공급망 재구성

생산 비용에 미치는 영향

수요측의 영향(소비자에 대한 비용)

최종 시장에의 가격 전달

시장 점유율 동향

소비자의 반응 패턴

영향을 받는 주요 기업

전략적인 업계 대응

공급망 재구성

가격 설정 및 제품 전략

정책관여

전망과 향후 검토 사항

기술적 상황

향후 시장 동향

갭 분석

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략 대시보드

제5장 시장 추계·예측 : 유형별(2021-2034년)

주요 동향

요오드화 조영제

가돌리늄 조영제

마이크로 버블 조영제

바륨 조영제

제6장 시장 추계·예측 : 형태별(2021-2034년)

주요 동향

액체

분말

기타

제7장 시장 추계·예측 : 모달리티별(2021-2034년)

주요 동향

X선

컴퓨터 단층 촬영(CT)

자기 공명 영상법(MRI)

초음파

제8장 시장 추계·예측 : 투여 경로별(2021-2034년)

주요 동향

혈관

경구

직장

기타

제9장 시장 추계·예측 : 적응증별(2021-2034년)

주요 동향

신경학적 장애

암

심혈관 질환

위장 장애

근골격계 질환

신장 질환

제10장 시장 추계·예측 : 용도별(2021-2034년)

주요 동향

방사선학

중재적 방사선학

중재적 심장학

제11장 시장 추계·예측 : 최종 용도별(2021-2034년)

주요 동향

병원, 진료소, ASC

진단 영상 센터

제12장 시장 추계·예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

네덜란드

아시아태평양

중국

인도

일본

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

제13장 기업 프로파일

Bayer

Bracco

GE HealthCare Technologies

Guerbet

Fresenius

iMAX Diagnostic Imaging

JB Chemicals &Pharmaceuticals

Jodas Expoim

Lantheus

Livealth Biopharma

nanoPET Pharma

Senochemia Pharmazeutika

TAEJOON Pharmaceutical

Trivitron Healthcare

Unijules Life Sciences

KTH

영문 목차

영문목차

The Global Contrast Media Market was valued at USD 7.2 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 12.9 billion by 2034, driven by the increased reliance on medical imaging to diagnose and manage a wide range of chronic health conditions. As the need for accurate and early diagnosis continues to rise, so do imaging techniques such as MRI, CT, X-ray, and ultrasound-all of which depend heavily on contrast agents to improve clarity and detail. Hospitals and diagnostic centers are performing more radiological procedures than ever, with inpatient and outpatient volumes increasing due to a growing population and the higher incidence of chronic illness.

Contrast-enhanced imaging is useful in identifying subtle abnormalities in tissues, blood vessels, and organs. This is especially critical in early detection leads to more effective treatment plans. The development of advanced imaging platforms and the integration of artificial intelligence are also shaping the landscape. Modern AI-driven radiology platforms enable precise dosage management and optimized workflow, supporting better diagnostic outcomes while maintaining patient safety.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$7.2 Billion

Forecast Value

$12.9 Billion

CAGR

6.1%

In 2024, iodinated contrast agents led the market with a 65.3% share. Their strong uptake is supported by widespread application in CT and X-ray procedures. Their versatility allows use across several diagnostic methods, including angiography and urography. The density of iodine enhances contrast and definition, crucial for clear and precise imaging results. This improved visibility allows for more confident diagnosis and treatment planning. The properties of iodine-based agents align well with the energy levels used in standard diagnostic imaging, making them the preferred choice across clinical settings.

The liquid contrast media segment held 78.4% share in 2024. Their widespread use is largely attributed to the practical advantages they offer-simple administration methods, rapid absorption, and effective visualization of internal structures. These agents are routinely used in high-demand diagnostic procedures like CT scans, where speed, precision, and image clarity are paramount. Their compatibility with various imaging systems and ability to quickly circulate through the bloodstream make them a go-to option for clinicians needing immediate and accurate diagnostic data. In both emergency and outpatient settings, the reliability and efficiency of liquid contrast media have solidified their position as the preferred medium in modern diagnostic workflows.

United States Contrast Media Market reached USD 2.3 billion in 2024 and is forecasted to reach USD 3.9 billion by 2034. This upward trajectory is propelled by a rise in chronic disease incidence, particularly within the aging population, where conditions like cancer, cardiovascular disease, and neurodegenerative disorders demand regular, high-precision imaging. Increasing use of MRI and CT technologies for both screening and monitoring drives steady demand for contrast-enhanced imaging agents. Additionally, innovation in imaging technologies, including AI-driven imaging platforms, makes contrast agents more effective, ensuring optimal dosing and better image acquisition.

Prominent companies in the market include TAEJOON Pharmaceutical, GE HealthCare Technologies, Livealth Biopharma, Bracco, Unijules Life Sciences, Guerbet, Trivitron Healthcare, nanoPET Pharma, Senochemia Pharmazeutika, Bayer, Jodas Expoim, J.B. Chemicals & Pharmaceuticals, Fresenius, Lantheus, and iMAX Diagnostic Imaging. To strengthen their market presence, key players are investing in R&D for next-gen contrast agents with improved safety profiles. They are also forming strategic alliances with imaging equipment manufacturers and expanding their global distribution networks. Several companies are exploring AI-integrated platforms to support precision imaging and reduce contrast dosage. Moreover, targeted marketing, regulatory approvals, and expansion in emerging markets help them secure a competitive advantage and boost revenue growth across geographies.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definitions

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Base estimates and calculations

1.3.1 Base year calculation

1.3.2 Key trends for market estimation

1.4 Forecast model

1.5 Primary research and validation

1.5.1 Primary sources

1.5.2 Data mining sources

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Growing regulatory approvals of contrast media

3.2.1.2 Growth in radiological examinations

3.2.1.3 Surging incidence of chronic diseases

3.2.1.4 Increase in minimally invasive procedures

3.2.2 Industry pitfalls and challenges

3.2.2.1 Presence of stringent regulations and frequent product recalls

3.2.2.2 Allergic reactions and side-effects associated with contrast media

3.3 Growth potential analysis

3.4 Regulatory landscape

3.5 Trump administration tariffs

3.5.1 Impact on trade

3.5.1.1 Trade volume disruptions

3.5.1.2 Country-wise response

3.5.2 Impact on the Industry

3.5.2.1 Supply-side impact (cost of manufacturing)

3.5.2.1.1.1 Price volatility in key materials

3.5.2.1.1.2 Supply chain restructuring

3.5.2.1.1.3 Production cost implications

3.5.2.2 Demand-side impact (cost to consumers)

3.5.2.2.1.1 Price transmission to end markets

3.5.2.2.1.2 Market share dynamics

3.5.2.2.1.3 Consumer response patterns

3.5.3 Key companies impacted

3.5.4 Strategic industry responses

3.5.4.1 Supply chain reconfiguration

3.5.4.2 Pricing and product strategies

3.5.4.3 Policy engagement

3.5.5 Outlook and future considerations

3.6 Technological landscape

3.7 Future market trends

3.8 Gap analysis

3.9 Porter's analysis

3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

5.1 Key trends

5.2 Iodinated contrast media

5.3 Gadolinium-based contrast media

5.4 Microbubble contrast media

5.5 Barium-based contrast media

Chapter 6 Market Estimates and Forecast, By Form, 2021 – 2034 ($ Mn)

6.1 Key trends

6.2 Liquid

6.3 Powder

6.4 Other forms

Chapter 7 Market Estimates and Forecast, By Modality, 2021 – 2034 ($ Mn)

7.1 Key trends

7.2 X-ray

7.3 Computed tomography (CT)

7.4 Magnetic resonance imaging (MRI)

7.5 Ultrasound

Chapter 8 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

8.1 Key trends

8.2 Intravascular route

8.3 Oral route

8.4 Rectal route

8.5 Other routes of administration

Chapter 9 Market Estimates and Forecast, By Indication, 2021 – 2034 ($ Mn)

9.1 Key trends

9.2 Neurological disorders

9.3 Cancer

9.4 Cardiovascular disease

9.5 Gastrointestinal disorders

9.6 Musculoskeletal disorders

9.7 Nephrological disorders

Chapter 10 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

10.1 Key trends

10.2 Radiology

10.3 Interventional radiology

10.4 Interventional cardiology

Chapter 11 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

11.1 Key trends

11.2 Hospitals, clinics, and ASCs

11.3 Diagnostic imaging centers

Chapter 12 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)