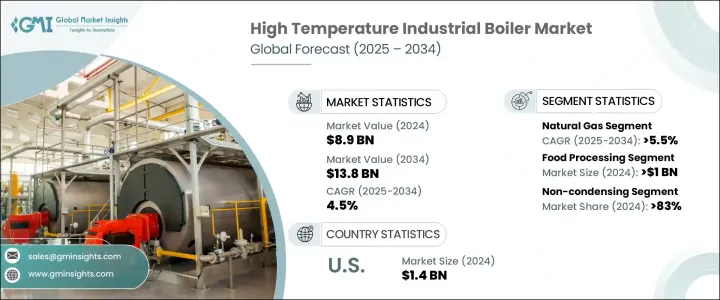

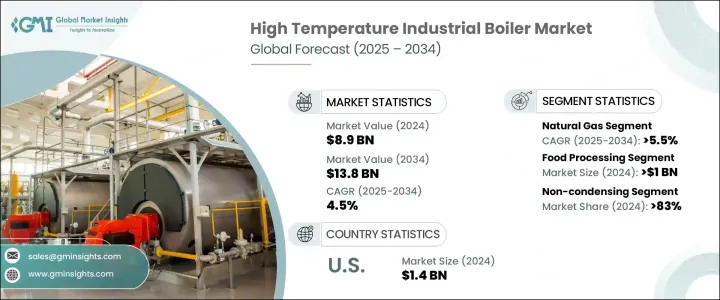

세계의 고온 산업용 보일러 시장 규모는 2024년에 89억 달러로 평가되었고, 신흥국 시장의 급속한 도시 확대에 의한 공업 생산의 급증을 배경으로, CAGR 4.5%로 성장할 전망이며, 2034년에는 138억 달러에 이를 것으로 예측되고 있습니다.

각국이 에너지 효율을 높이기 위해 보다 엄격한 규제를 실시하는 중, 고도의 보일러 기술에 대한 수요는 대폭 늘어날 것으로 예측됩니다. 인구 수준의 상승은 특히 상업 및 공업 공간의 난방 솔루션 소비 패턴에 영향을 미칩니다. 인프라 개발이 탄력을 받고 신재생 에너지의 통합이 보급됨에 따라 산업계는 보다 환경 친화적인 저배출 기술의 채택을 강요받고 있습니다. 이러한 동향은 지속 가능한 고온 보일러 시스템의 수요를 촉진할 것으로 예상됩니다.

이 산업은 현대적인 제조 공정에 대한 투자를 확대하고 세계 수준의 환경 의식이 높은 정책에 의해 형성되고 있습니다. 배기가스 규제가 우선 과제가 되는 가운데, 기후변화 목표에 따른 에너지 효율이 높은 솔루션이 선호되고 있습니다. 고온 산업용 보일러 시장은, 운용 비용과 에너지 소비량의 삭감을 목표로 하는 부문 전체에서 통합 시스템의 이용이 증가하고 있는 것으로부터, 새로운 혜택을 받고 있습니다. 에너지 안보 및 천연가스 인프라의 이용 가능성 확대가 가스식 고온 보일러의 채택을 계속 뒷받침하고 있습니다. 신뢰성이 높은 고온 스팀 솔루션이, 특히 열을 대량으로 소비하는 환경에서 산업계로부터 요구되고 있어 사업의 전망은 계속 견조합니다. 무역 정책과 경쟁 요인은 국제 경쟁력을 형성하는 추가 요인입니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 89억 달러 |

| 예측 금액 | 138억 달러 |

| CAGR | 4.5% |

천연가스 연소 고온 보일러는 산업계가 보다 청정한 에너지원으로의 이행을 지속하고 있기 때문에 2034년까지 CAGR 5.5%로 성장할 것으로 예측됩니다. 대기질에 관한 우려 고조, 천연가스의 이용 가능성 상승, 지원 인프라의 확대에 의해, 이러한 시스템은 보다 실행 가능하고 비용대비 효과가 높습니다. 많은 정부와 민간단체가 온실가스를 많이 배출하는 석탄 및 석유 의존을 줄이기 위해 가스 난방 기술에 적극적으로 투자하고 있습니다. 천연가스 보일러는 저배출가스 레벨을 유지하면서 안정적인 고온 출력을 제공할 수 있기 때문에 제조, 가공, 화학 등의 에너지 집약형 분야에서 바람직한 선택지가 되고 있습니다.

비응축식 고온 보일러 부문은 2024년에 83%의 점유율을 차지했습니다. 이러한 보일러는 간단한 설계, 내구성, 가혹한 환경에서도 성능을 발휘하는 능력으로 지지받고 있습니다. 연속적인 가열이 필요한 산업에서는 높은 보온성과 신속한 응답 시간으로 인해 비응축 시스템에 크게 의존하고 있습니다. 환경 규제의 고조에도 불구하고 인프라나 비용에 대한 배려로 응축형이나 하이브리드형으로 이행할 수 없는 경우, 이러한 보일러는 여전히 인기가 있습니다. 그러나 효율 기준의 변화에 대응하기 위해 제조사들은 보다 뛰어난 제어 시스템 및 고도의 연소 기술로 비응축형 모델을 강화하고 있습니다.

미국의 고온 산업용 보일러의 왕성한 국내 수요를 반영하여 2024년 시장은 14억 달러에 이르렀습니다. 이 성장의 대부분은 오래된 산업 시설의 노후화 및 비효율적인 보일러 시스템의 대체에 의한 것입니다. 에너지 소비와 배출에 관한 새로운 규제가 엄격해짐에 따라 산업계는 조업을 현대화하고 있습니다. 연방 및 주 차원의 인센티브는 보다 깨끗하고 고효율의 기기 채택을 지원함으로써 이러한 시프트를 촉진하고 있습니다. 지속가능성에 대한 관심의 고조는 에너지 인프라에 대한 경제적 투자와 맞물려 장래 대응 가능한 에너지 정책에 따른 기술적으로 고도의 보일러에 대한 요구를 뒷받침하고 있습니다.

시장 상황에 기여하는 주요 기업은 Siemens, Thermax, Mitsubishi Heavy Industries, Hurst Boiler and Welding, Babcock and Wilcox Enterprises, Sofinter, Forbes Marshall, GE Vernova, Victory Energy Operations, Cleaver-Brooks, Viessmann, Clayton Industries, Cochran, Doosan Heavy Industries & Construction, FONDITAL, Bharat Heavy Electricals, FERROLI, Hoval, John Wood Group, Groupe Atlantic, IHI Corporation, Walchandnagar Industries, John Cockerill, Miura America, The Fulton Companies, Robert Bosch, Fonderie Sime 및 Rentech Boilers 등입니다. 이 시장에서의 지위를 강화하기 위해 대기업은 기술 혁신, 지속가능성 및 전략적 제휴에 주력하고 있습니다. 각 회사는 연구 개발에 투자하여 엄격한 배출 기준을 충족하는 콤팩트하고 에너지 효율이 높은 보일러를 개발하고 있습니다. 정부 및 다른 산업 기업과의 제휴는 업무 범위를 확대하고 공급망을 합리화하는 데 도움이 되고 있습니다. 많은 기업들은 보일러의 성능을 최적화하고 다운타임을 최소화하기 위해 디지털 제어 시스템을 강화하는 한편 장기적인 고객 관계를 구축하기 위해 애프터마켓 서비스를 확대하고 있습니다.

The Global High Temperature Industrial Boiler Market was valued at USD 8.9 billion in 2024 and is estimated to grow at a CAGR of 4.5% to reach USD 13.8 billion by 2034, driven by the surge in industrial production with rapid urban expansion across developing nations. As countries implement stricter regulations to boost energy efficiency, demand for advanced boiler technologies is expected to grow significantly. Rising population levels influence consumption patterns, particularly for heating solutions in commercial and industrial spaces. With infrastructure development gaining momentum and renewable energy integration becoming more widespread, industries are under increased pressure to adopt greener, low-emission technologies. These trends are expected to fuel demand for sustainable high-temperature boiler systems.

The industry is also being shaped by growing investments in modern manufacturing processes and eco-conscious policies at the global level. With emissions control becoming a priority, there's a growing preference for energy-efficient solutions that align with climate goals. The high temperature industrial boiler market is further benefiting from the increased use of integrated systems across sectors seeking to reduce operational costs and energy consumption. Energy security and the expanding availability of natural gas infrastructure continue to support the adoption of gas-powered high-temperature boilers. With industries demanding reliable high-temperature steam solutions, especially in heat-intensive environments, the business outlook remains strong. Trade policies and component pricing are additional factors shaping global competitiveness.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.9 Billion |

| Forecast Value | $13.8 Billion |

| CAGR | 4.5% |

Natural gas-fired high temperature boilers are projected to grow at a CAGR of 5.5% through 2034, as industries continue shifting toward cleaner energy sources. Increasing concerns around air quality, rising natural gas availability, and expanding supportive infrastructure make these systems more viable and cost-effective. Many governments and private entities are actively investing in gas-powered heating technologies to reduce dependence on coal and oil, which emit higher levels of greenhouse gases. The ability of natural gas boilers to deliver consistent high-temperature output while maintaining lower emission levels positions them as a preferred option across energy-intensive sectors such as manufacturing, processing, and chemicals.

Non-condensing high temperature boilers segment held an 83% share in 2024. These boilers are favored for their simple design, durability, and ability to perform in demanding environments. Industries with continuous heating needs rely heavily on non-condensing systems due to their high heat retention and quick response time. Despite growing environmental regulations, these boilers remain popular where infrastructure or cost considerations prevent a shift to condensing or hybrid models. However, to meet changing efficiency standards, manufacturers are enhancing non-condensing models with better control systems and advanced combustion technologies.

United States High Temperature Industrial Boiler Market reached USD 1.4 billion in 2024, reflecting strong domestic demand. A major portion of this growth is attributed to replacing aging and inefficient boiler systems in older industrial facilities. As new regulations on energy consumption and emissions become more stringent, industries modernize their operations. Federal and state-level incentives are encouraging this shift by offering support for the adoption of cleaner, high-efficiency equipment. The increased focus on sustainability, coupled with economic investments in energy infrastructure, is driving the need for technologically advanced boilers that align with future-ready energy policies.

Leading companies contributing to the market landscape include Siemens, Thermax, Mitsubishi Heavy Industries, Hurst Boiler and Welding, Babcock and Wilcox Enterprises, Sofinter, Forbes Marshall, GE Vernova, Victory Energy Operations, Cleaver-Brooks, Viessmann, Clayton Industries, Cochran, Doosan Heavy Industries & Construction, FONDITAL, Bharat Heavy Electricals, FERROLI, Hoval, John Wood Group, Groupe Atlantic, IHI Corporation, Walchandnagar Industries, John Cockerill, Miura America, The Fulton Companies, Robert Bosch, Fonderie Sime, and Rentech Boilers. To reinforce their position in the market, major players are focusing on innovation, sustainability, and strategic alliances. Companies invest in R&D to develop compact, energy-efficient boilers that meet stringent emissions standards. Partnerships with governments and other industrial firms help expand operational reach and streamline supply chains. Many enhance digital control systems to optimize boiler performance and minimize downtime, while expanding aftermarket services to build long-term client relationships.